Get Complete Analysis Of The Report - Download Updated Free Sample PDF

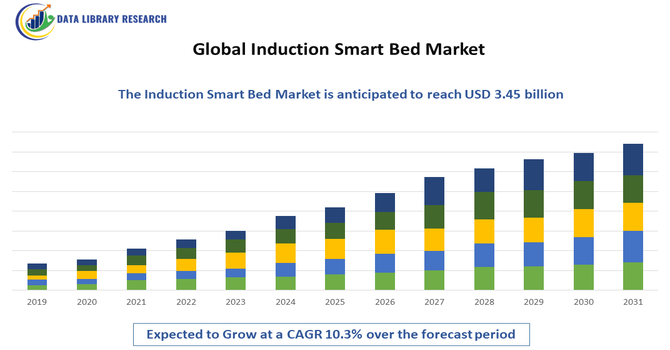

The Global Induction Smart Bed Market refers to the industry focused on advanced beds that use induction technology to provide personalized comfort, health monitoring, and therapeutic features. These beds can adjust firmness, temperature, and support automatically, often integrating sensors to track sleep patterns and vital signs. Rising awareness of sleep health, technological innovations, and increasing adoption in hospitals, wellness centers, and homes are driving demand and shaping the market worldwide.

The growth of the Global Induction Smart Bed Market has been driven by increasing awareness of sleep health and wellness, rising prevalence of sleep disorders, and the growing adoption of smart home technologies. Innovations such as adjustable firmness, temperature control, biometric monitoring, and integration with mobile apps have enhanced user convenience and personalized comfort. Additionally, expanding applications in hospitals, elderly care, and luxury hospitality, along with rising disposable incomes, have fueled market demand and encouraged continuous technological development.

The Global Induction Smart Bed Market is witnessing trends driven by technology integration and personalization. Smart beds with features like sleep tracking, temperature adjustment, automatic firmness control, and health monitoring are becoming increasingly popular. Connectivity with smartphones and smart home ecosystems allows users to customize settings and receive real-time insights into sleep patterns. Additionally, rising interest in wellness, preventive healthcare, and home automation is pushing manufacturers to innovate. AI-driven analytics and cloud-based sleep data management are emerging trends. Hospitals and luxury hotels are adopting these beds to enhance patient and guest experiences, further accelerating market growth.

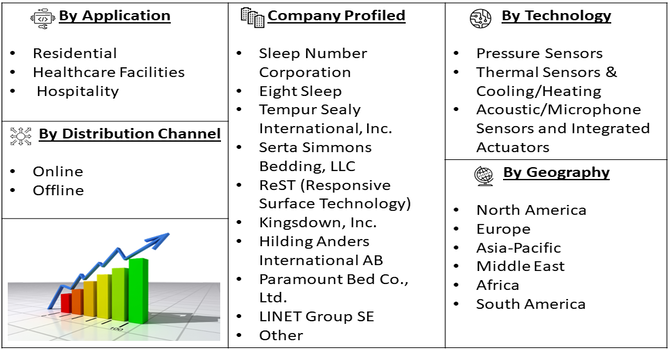

Segmentation: The Global Induction Smart Bed Market is Segmented by Technology (Pressure Sensors, Thermal Sensors & Cooling/Heating, Acoustic/Microphone Sensors and Integrated Actuators), Application (Residential, Healthcare Facilities, and Hospitality), Distribution Channel (Online and Offline), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Global concern for sleep quality and its impact on long-term health was a major driver of the induction smart bed market. As sleep disorders like insomnia and sleep apnea grew, more people sought non-pharmaceutical solutions. For instance, in February 2025, ResMed released its fifth annual Global Sleep Survey, revealing that poor sleep affected health, work, and relationships worldwide. Among 30,026 respondents across 13 markets, 70% of employed individuals reported missing work due to inadequate sleep, while 18% of couples slept separately due to snoring and restlessness. Thus, the global induction smart bed market benefited from increased adoption of AI-enabled, adaptive sleep solutions targeting restorative sleep and wellness-focused consumers.

Smart beds with biometric sensors and sleep tracking capabilities helped users and healthcare providers monitor vital signs and sleep patterns, promoting better sleep hygiene. This health-oriented demand was amplified by preventive care trends, where consumers increasingly saw sleep optimization as part of overall wellness, making intelligent beds a valuable investment in personal health.

Technological advancements, particularly in the Internet of Things (IoT), powered substantial growth in the induction smart bed market. Smart beds began to include embedded sensors, connectivity, actuators, and automated firmness or temperature adjustments, allowing seamless integration with smartphones and home automation systems. Users could control and customize their sleep environment remotely, receiving personalized insights via apps. This connectivity, combined with AI-driven analytics, made smart beds more appealing to tech-savvy consumers and wellness-focused buyers, driving adoption within modern smart homes.

Market Restraints:

A key restraint for the global induction smart bed market was the high upfront cost, which limited adoption among price-sensitive consumers. Advanced smart beds with embedded sensors, connectivity modules, and actuators often carried a significant premium over traditional mattresses. In addition, data privacy concerns emerged as another barrier: sleep data, biometric measurements, and other personal health metrics collected by smart beds raised worries over unauthorized access and misuse. Fear of data breaches and insufficient transparency about how data was stored or shared discouraged widespread consumer adoption, slowing market growth.

Induction smart beds are positively impacting society and economies by improving health, productivity, and quality of life. Better sleep contributes to reduced medical expenses, enhanced mental health, and higher workplace efficiency. The adoption of smart beds in hospitals and elderly care facilities supports patient monitoring and preventive care, reducing strain on healthcare systems. The market is also creating jobs in R&D, manufacturing, and tech support. Rising consumer spending on health and wellness products demonstrates socioeconomic shifts toward preventive care and technology-driven lifestyles. As awareness of sleep’s importance grows, these beds are fostering broader societal benefits and contributing to economic activity.

Segmental Analysis:

The Thermal Sensors & Cooling/Heating segment of the Global Induction Smart Bed Market is expected to witness the highest growth over the forecast period. Rising consumer demand for personalized sleep experiences, including automatic temperature regulation and climate control, is driving adoption. These beds monitor body heat and adjust cooling or heating systems in real time, enhancing comfort and sleep quality. Technological advancements in energy-efficient thermal systems, combined with integration into smart home ecosystems, further support market expansion. Healthcare applications, such as improving patient sleep and recovery, also contribute. The segment’s growth reflects the increasing focus on smart, adaptive, and high-precision sleep solutions.

The Residential segment is projected to witness the highest growth over the forecast period, driven by increasing awareness of sleep wellness and growing smart home adoption. Consumers are investing in smart beds to improve comfort, monitor health, and enhance sleep quality. Rising disposable incomes, urbanization, and changing lifestyles have fueled demand for technologically advanced mattresses that offer personalized experiences. Additionally, integration with mobile apps, IoT devices, and voice assistants makes residential smart beds more attractive. The trend toward home-based healthcare solutions and preventive wellness further supports growth, positioning residential applications as a key driver in the global induction smart bed market.

The Offline segment is expected to witness the highest growth over the forecast period due to consumer preference for physically inspecting smart beds before purchase. Retail stores and specialized mattress showrooms allow customers to experience features like firmness adjustment, temperature control, and sleep tracking firsthand, building trust and confidence in technology. Offline sales channels also offer personalized consultations, demonstrations, and installation services, enhancing the buying experience. While e-commerce is growing, the tactile and experiential nature of smart beds makes offline channels critical. Manufacturers and retailers are expanding physical presence and showrooms, ensuring consumers have hands-on experience, thereby boosting adoption in the offline segment.

North America is expected to witness the highest growth in the Global Induction Smart Bed Market over the forecast period. High consumer awareness about sleep health, widespread smart home adoption, and advanced technological infrastructure are driving market expansion.

The region has a strong presence of key market players, significant R&D investment, and early adoption of innovative smart bed features like biometric tracking, temperature control, and AI-driven analytics. For instance, in April 2023, Sleep Number Corporation launched its next-generation Sleep Number® smart beds and Lifestyle Furniture, building on the award-winning 360® series. Leveraging over 19 billion hours of proprietary sleep data, the beds used AI and embedded sensors to learn individual biometrics, automatically adjusting firmness and support for varying life stages, from pregnancy to aging. This innovation strengthened the U.S. induction smart bed market by driving consumer demand for highly personalized, adaptive sleep solutions, encouraging competitors to integrate AI and data-driven features, and accelerating adoption of smart beds across residential and healthcare segments.

Rising disposable income and a growing focus on preventive healthcare and wellness solutions further support demand. For instance, in August 2025, U.S. personal income rose by USD 95.7 billion (0.4%), with disposable personal income increasing USD 86.1 billion, while personal consumption expenditures grew USD 129.2 billion. Personal savings totaled USD 1.06 trillion, representing a 4.6% saving rate. The rise in disposable income boosted consumer spending capacity, positively impacting the U.S. induction smart bed market by enabling more households to invest in advanced sleep solutions, driving demand for AI-enabled, adaptive, and wellness-focused smart beds, and supporting growth across residential and premium segments. Thus, together, such factors are driving factors of this market in this region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the induction smart bed market is characterized by innovation-driven rivalry among established mattress manufacturers and emerging tech-focused startups. Companies are differentiating products through features like AI-based sleep tracking, IoT connectivity, and customizable comfort. Strategic partnerships with hospitals, wellness centers, and luxury hotels are common to expand market reach. Some players focus on high-end consumer segments, while others target healthcare applications. Continuous investment in R&D, marketing, and smart home integration defines competitive positioning. Global expansion, patent development, and mergers or acquisitions are shaping market dynamics, encouraging rapid innovation while increasing barriers for new entrants.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the accelerating consumer desire for preventative health management and wellness tracking. Smart beds address this by offering sophisticated, continuous, and passive monitoring of vital signs, sleep cycles, and heart rate without requiring wearable devices. Furthermore, the rapid adoption of Internet of Things (IoT) technology in homes and the integration of smart beds with broader home automation systems, along with rising disposable incomes in developed nations, strongly support market expansion.

Q2. What are the main restraining factors for this market?

The major restraint is the significantly high price point of induction smart beds compared to traditional premium mattresses, which restricts adoption to affluent consumers. Consumers also show hesitation due to privacy and security concerns related to the continuous collection and storage of personal biometric health data over cloud networks. Additionally, the need for specialized technical support for complex sensor calibration and troubleshooting, combined with the potential for electronic obsolescence, poses a barrier in less developed markets.

Q3. Which segment is expected to witness high growth?

The Thermal Control Segment is projected for the highest growth because optimal body temperature regulation is scientifically proven to be the most effective way to improve sleep onset and duration. These smart beds directly solve the widespread issue of sleeping too hot or too cold. By offering personalized microclimates for dual users and adapting dynamically, this technology delivers a tangible benefit that strongly justifies the premium price.

Q4. Who are the top major players for this market?

The market is highly competitive, featuring both established bedding manufacturers and specialized technology firms. Top major players include Sleep Number Corporation, which pioneered adjustable comfort technology, Eight Sleep, known for its integrated temperature regulation, and Reverie. These companies compete by focusing on data accuracy, user experience, and establishing partnerships with tech giants (like Google and Amazon) to seamlessly integrate their sleep data with broader digital health ecosystems.

Q5. Which country is the largest player?

The United States is the largest country player in the Global Induction Smart Bed Market. This dominance is attributed to the country’s high levels of disposable income and high consumer willingness to invest heavily in personal wellness technology. The presence of major domestic smart bed manufacturers, widespread technological literacy, and a robust healthcare system that increasingly recognizes the importance of sleep health all contribute to the U.S. having the highest market value and fastest adoption rate for these innovative products.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model