Get Complete Analysis Of The Report - Download Updated Free Sample PDF

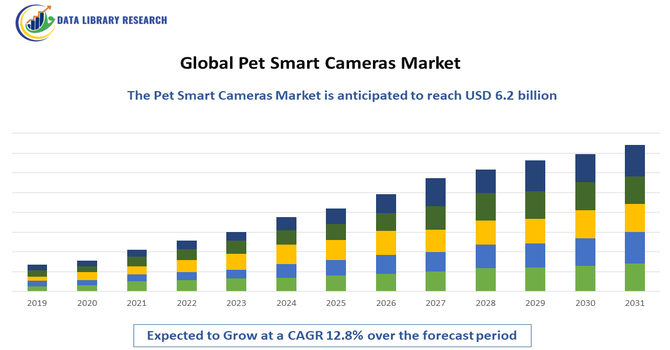

The Global Pet Smart Cameras Market encompasses connected camera devices designed for pet owners to remotely monitor, interact with, and care for their pets through features like live video streaming, two way audio, treat dispensing and motion detection. Driven by increasing pet humanization, rise in pet ownership and integration with smart homes, this market enables consumers to keep tabs on pets from anywhere, blending convenience, safety and engagement.

The global pet smart cameras market is being fuelled by strong drivers: a rise in pet ownership and the increasing humanisation of pets motivate owners to invest in devices that allow remote monitoring and interaction. Meanwhile, technological advancements such as AI driven features, two way video, treat dispensing, and smart home integration make these cameras more appealing and functional. Together with growing disposable incomes, widespread smartphone penetration and expanding online retail channels, these factors combine to accelerate adoption and growth worldwide.

The global pet smart cameras market is being shaped by several strong trends: artificial intelligence and machine learning are now embedded into devices, enabling behavior recognition, tailored alerts and predictive pet wellness insights. Integration with smart home ecosystems and voice assistants is becoming standard. Interactive features like treat dispensers, two way audio/video, remote play and health monitoring are gaining traction, shifting devices from mere surveillance to comprehensive pet care platforms.

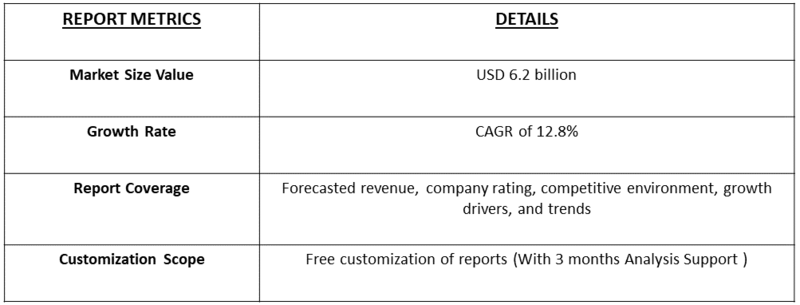

Segmentation: The Global Pet Smart Cameras Market is Segmented by Product Type (Interactive Cameras, Monitoring Cameras, Treat Dispensing Cameras and Others), Application (Including Pet Monitoring, Pet Training, Pet Entertainment and Other Use Cases), Distribution Channel (Online Retail, Supermarkets/Hypermarkets, Specialty Pet Or Electronics Stores and Other Channels), Connectivity/Feature (Wi Fi Enabled, Bluetooth, Cloud Connected, AI Enabled and Other Variants), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global pet smart cameras market is being significantly driven by the increasing number of pet owners and the growing trend of humanising pets. As more households view their pets as family members, there is heightened demand for devices that help monitor, interact with and care for animals when owners are away or busy.

Globally, approximately 16 million dogs and cats are living in shelters, waiting for their forever homes. In response, in September 2025, Mars, Incorporated hosted its second annual Global Adoption Weekend to connect these pets with loving families. Research from a survey commissioned by Mars and Calm found that 83 % of pet owners said their pet had improved their mental well-being, and 73 % reported their pet helped them stop overthinking or worrying. This trend is especially strong among younger demographics in urban areas, where dual income households and remote working lifestyles amplify the need for remote pet care solutions that deliver reassurance and engagement.

Another powerful driver is the rapid advancement of smart home technology, AI, connectivity and IoT-enabled devices. Pet smart cameras now incorporate features such as two way audio, treat dispensing, motion alerts, behaviour recognition and live streaming via mobile apps, making them more attractive and functional. As smart home ecosystems become more common, pet owners increasingly expect seamless integration of monitoring cameras into their automation platforms and voice assistant networks. This convergence of pet care and home technology significantly boosts adoption rates.

Market Restraint:

Despite robust growth potential, the pet smart cameras market is restrained by several critical factors. High upfront costs—especially for models with advanced features like AI analytics, treat dispensers and cloud subscriptions—make them less accessible to budget conscious consumers, particularly in emerging markets. In addition, concerns over data security and privacy, given that cameras stream video and audio from inside homes, have dampened some buyers’ enthusiasm. Connectivity issues in regions with unstable internet or low broadband penetration also limit functionality and user satisfaction, thereby slowing adoption in certain areas.

The Pet Smart Cameras Market has a significant socioeconomic impact, primarily rooted in the psychological and emotional benefits it provides to pet owners. By enabling constant remote monitoring and interaction, these devices alleviate pet-owner anxiety (separation anxiety) and enhance the emotional bond between humans and animals, contributing to overall mental well-being. Economically, the market fosters high-tech job creation in software development, AI analytics, and specialized manufacturing. Furthermore, the data collected can lead to early detection of health issues, potentially reducing veterinary costs and improving long-term pet health, which supports the broader, growing pet care economy.

Segmental Analysis

The interactive cameras segment in the global pet smart cameras market is poised for strong expansion as pet owners increasingly seek devices that do more than just surveillance. These cameras offer features such as treat dispensing, laser play, two way communication, and smartphone based interaction which enhance engagement and reduce pet anxiety. With the rise in dual income households, busy lifestyles and urban living, owners are willing to invest in technology that keeps pets entertained and monitored when they’re away. The trend toward viewing pets as family members is pushing demand for interactive solutions, making this segment a rapidly growing portion of the market.

The pet monitoring application segment is set to grow significantly as remote monitoring becomes a priority for pet owners who spend time away from home. Smart cameras designed for pet monitoring allow live video streaming, alerts for movement or sound, and two way communication, giving owners peace of mind about their pets’ wellbeing. The increasing adoption of smart home devices, higher disposable incomes and rising pet humanization are driving this demand. Moreover, urbanization and smaller living spaces make remote monitoring practical and desirable, positioning the pet monitoring segment as a key growth area within the broader pet smart cameras market.

The supermarkets and hypermarkets distribution channel is expected to experience notable growth for pet smart cameras as mass retail outlets expand their consumer electronics offerings and appeal to broad pet owner demographics. Large format stores offer the advantage of physical product display, in store demonstrations and immediate purchase, which appeals to shoppers preferring hands on evaluation. As smart pet accessories become more mainstream, parents of pets increasingly browse big box retailers during regular shopping trips. This visibility, combined with promotional tie ins and broad foot traffic, helps drive awareness and adoption through large retail chains, making this channel crucial for market expansion.

The Wi Fi enabled segment in the pet smart cameras market is set for robust growth thanks to its compatibility with home internet networks, mobile apps and smart home ecosystems. These devices support remote access, cloud storage, real time video and voice communication, features that tech savvy pet owners increasingly demand. As broadband speeds rise, wireless infrastructure becomes more prevalent and consumers seek seamless integration with smartphones and home assistants, Wi Fi cameras become the default choice. Moreover, the convenience of setup without additional wiring and the ability to view pets from anywhere further drives the adoption of Wi Fi enabled units.

The North America region is forecast to grow strongly in the pet smart cameras market due to high pet ownership rates, substantial disposable incomes and widespread adoption of smart home technologies. In recent years across North America, pet adoption rose as more people viewed animals as part of the family and expressed strong interest in shelter adoption. A study of 2,500 current and prospective pet owners revealed that younger generations were particularly likely to adopt a shelter pet, with adoption intention steadily rising. Meanwhile, shelters struggled with overcapacity as intake volumes increased and animals remained in care for longer periods.

Established retail channels, sophisticated e commerce ecosystems and a tech friendly culture further support market growth. As the desire for connectivity, convenience and pet well being features rises, North America remains a leading region and will continue powering global demand for pet smart camera innovations. For instance, in June 2022, Petlibro Granary Series 5 L Camera Monitoring Automatic Pet Feeder was launched in the U.S., retailing at around USD 129.99 via Petlibro’s online store and Amazon. Designed for pet owners focused on feeding, living, and staying connected with their fur friends, the feeder features a built in 1080p camera, Wi Fi connectivity and app controlled scheduling. Its introduction contributed to the U.S. smart pet care market by raising consumer expectations for integrated monitoring and feeding solutions, enhancing the appeal of tech enabled pet accessories and accelerating premium segment uptake in the U.S. market.

To Learn More About This Report - Request a Free Sample Copy

The Global Pet Smart Cameras Market features a highly competitive landscape driven by innovation in AI and features. The market sees rivalry between specialized pet-tech companies like Furbo and Petcube, who focus on unique functionalities like treat dispensing, and major smart home/security camera manufacturers (e.g., Arlo, Wyze, and TP-Link) that adapt their core technology for pet monitoring. Competition is intense in two key areas: integrating advanced AI for behavioral tracking and abnormal noise alerts, and offering seamless two-way audio/video communication. Brands are also fighting for market share through flexible online distribution, strategic pricing across low, medium, and premium tiers, and offering value through recurring subscription services for cloud storage and enhanced features.

The 20 major players for above market:

Recent Development

Q1. What the main growth driving factors for this market?

The main growth driver is the accelerating trend of pet humanization, where owners increasingly view their pets as family members and prioritize their well-being. This emotional bond translates into higher spending on pet safety and comfort. Additionally, the widespread adoption of smart home technology and the continuous integration of Artificial Intelligence (AI) into cameras are key factors. Features like two-way audio, remote treat dispensing, and AI-powered detection of barking or abnormal pet behavior provide owners with peace of mind and allow for remote interaction, strongly driving market demand.

Q2. What are the main restraining factors for this market?

The significant restraining factor is the relatively high cost of premium pet smart cameras, especially those offering advanced AI features, cloud storage, or high-resolution video. This initial investment, often coupled with recurring subscription fees for advanced features, can deter price-sensitive consumers. Another major restraint is growing concern over data privacy and security. Since these devices are constantly recording sensitive footage from inside the home, consumers are increasingly cautious about potential security breaches or misuse of personal data and video recordings.

Q3. Which segment is expected to witness high growth?

The Two-Way Video and Audio Functionality segment is expected to witness the highest growth. This is driven by the desire for interactive engagement rather than just passive monitoring. Pet owners want to communicate with their pets, provide comfort, and give commands remotely. This segment often includes features like treat dispensing and laser toys, enhancing the quality of remote interaction. The demand for these sophisticated, multifunctional devices is soaring, especially among younger, tech-savvy pet owners.

Q4. Who are the top major players for this market?

The market is led by companies that specialize in pet tech and smart home security systems. Top major players include Petcube, known for its interactive cameras and treat dispensers, and Furbo, which specializes in dog cameras with toss functionality. General smart home and camera manufacturers such as Arlo and Wyze also compete heavily by adapting their existing surveillance technology for pet-specific applications. The intense competition encourages continuous innovation in AI-powered features and connectivity.

Q5. Which country is the largest player?

North America, specifically the United States, currently holds the largest market share in the Pet Smart Cameras Market in terms of revenue. This is due to the very high rate of pet ownership, substantial disposable income dedicated to pet care, and the high adoption rate of smart home technologies. The region's established e-commerce infrastructure and a deeply ingrained culture of viewing pets as family members solidify its position as the primary revenue generator.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model