ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Overview and Analysis

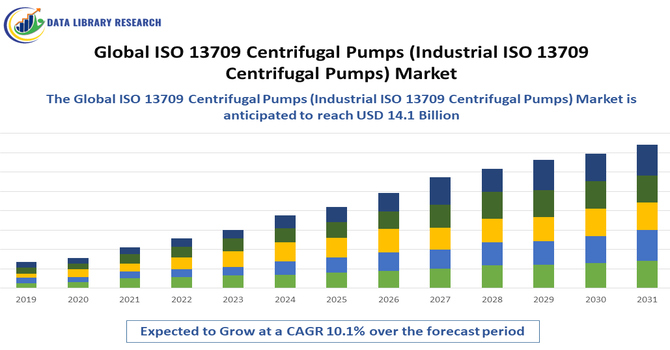

- The ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market size was valued at USD 9.2 Billion in 2025 and is projected to reach USD 14.1 Billion by 2032, growing at a CAGR of 10.1% from 2025 to 2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The ISO 13709 Centrifugal Pumps market refers to the global industry for centrifugal pumps designed and manufactured in compliance with ISO 13709 (API 610) standards, which outline rigorous specifications for heavy-duty, petroleum, petrochemical, and natural gas industry applications. These pumps are engineered for high performance, reliability, and durability in harsh industrial environments, making them essential in sectors like oil & gas, chemical processing, power generation, and water treatment. Market growth is driven by increasing industrialization, energy demand, infrastructure investments, and the need for standardized, efficient pumping solutions that meet stringent international safety and quality benchmarks.

ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Latest Trends

The key market trends for the ISO 13709 (API 610) centrifugal pumps are: increasing demand for energy efficient and environmentally friendly designs (variable speed drives, improved hydraulics, better materials) to reduce operating costs and emissions; integration of smart technologies / IoT, predictive maintenance and real time monitoring for better uptime and lower life cycle costs. Growth is being fueled by expanding downstream capacity in oil & gas, petrochemical plants, power generation and water treatment, especially in emerging markets (Asia Pacific, Middle East, Latin America). Also notable are shifts towards corrosion and wear resistant materials, modular/customizable designs to suit specific severe service or harsh environment applications. Rising standards and stricter regulatory requirements are pushing adoption of high performance, standardized pumps.

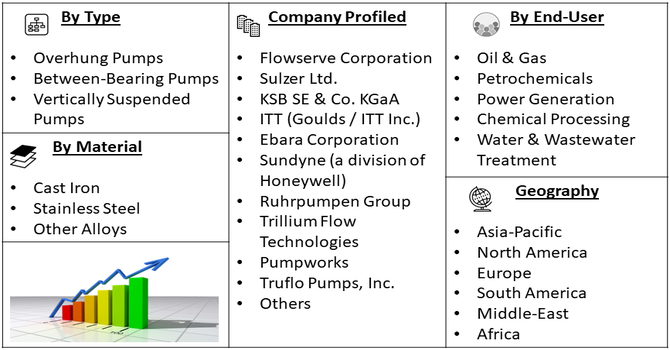

Segmentation: The ISO 13709 (Industrial API 610) Centrifugal Pumps market is Segmented by Product Type (Overhung Pumps, Between-Bearing Pumps, and Vertically Suspended Pumps), Material (Cast Iron, Stainless Steel, and Other Alloys), End-Use Industry (Oil & Gas, Petrochemicals, Power Generation, Chemical Processing, and Water & Wastewater Treatment), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

- Growing Demand in Oil & Gas Industry

The main drivers for the ISO 13709 centrifugal pumps market is the strong demand from the oil and gas sector. These pumps are designed to handle high-pressure and high-temperature fluids, making them ideal for refineries and petrochemical plants. As global energy demand rises, many countries are investing in new exploration and refining projects, especially in the Middle East and Asia. These projects require highly reliable pumps that meet strict international standards like ISO 13709. This trend is creating steady demand for API 610-compliant pumps, as companies seek efficient and safe equipment that ensures smooth operations with minimal downtime.

In January 2025, the Government of India reported that India’s petroleum industry involved exploration, production, refining, and distribution of oil and gas, playing a key role in energy security and economic growth. This activity drove strong demand for reliable equipment like ISO 13709 (API 610) centrifugal pumps. As operations expanded, the need for high-performance pumps to handle harsh conditions grew, directly supporting market growth in the oil & gas and industrial pump sectors.

- Focus on Equipment Reliability and Safety

Another major driver is the increasing focus on safety and equipment reliability in industrial operations. ISO 13709 centrifugal pumps are built to perform in extreme conditions and follow strict design and testing requirements. Industries like chemicals, power, and water treatment need equipment that can run continuously without failure, as breakdowns can lead to costly shutdowns or safety hazards. The high build quality, standardized design, and proven performance of these pumps make them a preferred choice. As industries continue to modernize and upgrade their systems, the demand for these reliable and safe pumping solutions is expected to grow significantly.

Market Restraints:

- High Initial Cost and Maintenance Complexity

The key restraint in the ISO 13709 centrifugal pumps market is the high initial cost and complex maintenance needs. These pumps are made from advanced materials and are engineered to meet strict industrial standards, which makes them more expensive than regular pumps. For small and medium-sized businesses, this upfront cost can be a major hurdle. Additionally, the pumps require skilled personnel for installation, monitoring, and maintenance, which adds to operational costs. In regions with limited technical expertise or tighter budgets, companies may choose lower-cost alternatives, even if they are less reliable. This can slow down adoption, especially in price-sensitive or less-developed markets.

Socio Economic Impact on ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market

The socioeconomic landscape of the ISO 13709 (Industrial API 610) centrifugal pumps market is influenced by industrialization trends, infrastructure development, and energy demand, particularly in emerging economies. As countries like India, China, and several Middle Eastern nations invest heavily in oil refining, petrochemicals, and power generation, the demand for standardized and reliable pumping solutions grows. This industrial expansion creates jobs, supports local manufacturing, and drives technology transfer. At the same time, rising environmental awareness and regulatory pressures are pushing industries to adopt more efficient and safer equipment, influencing purchasing decisions. However, in lower-income regions, high equipment costs and lack of technical expertise may limit accessibility, highlighting the gap between developed and developing markets in terms of industrial capability and technological adoption.

Segmental Analysis:

- Vertically Suspended Pumps Segment is Expected to Witness Significant Growth Over the Forecast Period

The vertically suspended pumps segment is projected to experience substantial growth due to its suitability for applications involving deep well pumping, cooling water systems, and handling large volumes of fluid in limited space. These pumps are widely used in power plants, refineries, and water treatment facilities where space efficiency and vertical installation are critical. Their robust design and ability to operate under harsh conditions make them ideal for critical industrial applications. With increasing global investments in power generation and oil & gas infrastructure, especially in Asia-Pacific and the Middle East, the demand for vertically suspended pumps is expected to rise. Additionally, the push toward upgrading older pumping systems with more efficient and reliable alternatives is fueling market expansion in this segment.

- Cast Iron Segment is Expected to Witness Significant Growth Over the Forecast Period

The cast iron segment is anticipated to grow significantly due to its cost-effectiveness, durability, and wide applicability across various industrial sectors. Cast iron pumps are commonly used in water and wastewater management, general industrial processes, and applications where fluid characteristics are non-corrosive. As developing regions focus on expanding their municipal and industrial water infrastructure, the demand for affordable and reliable pump materials like cast iron is rising. Additionally, cast iron offers ease of manufacturing and maintenance, making it a practical choice for both OEMs and end-users. Its growth is also supported by the steady expansion of small and medium-sized industries, particularly in Asia-Pacific and Latin America, where budget-conscious investments in robust equipment are driving adoption.

- Power Generation Segment is Expected to Witness Significant Growth Over the Forecast Period

The power generation sector is expected to be a major driver of growth in the ISO 13709 centrifugal pumps market due to increasing global electricity demand and investments in modernizing aging power infrastructure. These pumps are essential for cooling water circulation, boiler feed applications, and other critical processes in both thermal and nuclear power plants. As governments across Asia-Pacific, the Middle East, and Africa invest in expanding power capacity to meet growing urban and industrial needs, the demand for high-performance, API 610-compliant pumps will rise. Moreover, the transition toward more efficient and environmentally sustainable power systems is encouraging the use of durable and energy-efficient pumping solutions, further fueling the growth of this segment in the forecast period.

- Asia Pacific Region is Expected to Witness Significant Growth Over the Forecast Period

The Asia Pacific region is set to witness significant growth in the ISO 13709 centrifugal pumps market, driven by rapid industrialization, urban expansion, and major infrastructure investments. Countries like China, India, and Southeast Asian nations are heavily investing in oil & gas, power generation, water treatment, and chemical processing—industries that heavily rely on high-performance centrifugal pumps. Government initiatives to improve energy security, expand refining capacity, and upgrade municipal infrastructure are creating strong demand for ISO-compliant pumping systems.

Additionally, the presence of local pump manufacturers and growing foreign direct investment in industrial sectors are enhancing market accessibility. For instance, in January 2025, the Chinese China’s total oil demand, including all petroleum products, was projected to peak by 2027, with a modest increase of around 100,000 barrels per day in the current year, mainly driven by growth in the petrochemicals sector. However, the rapid rise in electric vehicle (EV) adoption—particularly in the world’s largest oil-importing country—was significantly reducing demand for conventional fuels. In 2025 alone, EV usage was expected to replace at least 25 million metric tons of gasoline, equivalent to about 582,000 barrels per day, highlighting a major shift in energy consumption patterns away from traditional fossil fuels, reported that China’s total oil demand, including all petroleum products, was projected to peak by 2027, with a modest increase of around 100,000 barrels per day in the current year, mainly driven by growth in the petrochemicals sector. However, the rapid rise in electric vehicle (EV) adoption—particularly in the world’s largest oil-importing country—was significantly reducing demand for conventional fuels. In 2025 alone, EV usage was expected to replace at least 25 million metric tons of gasoline, equivalent to about 582,000 barrels per day, highlighting a major shift in energy consumption patterns away from traditional fossil fuels. With a large and growing population, increasing energy needs, and favourable economic policies, Asia Pacific remains a key growth engine for the market during the forecast period.

| Report Matrics |

Details |

| Market Size Value |

USD 14.1 Billion |

| Growth Rate |

CAGR of10.1% |

| Forecast |

2026-2033 |

| Historical data |

2021-2024 |

| Base Year |

2025 |

| Report Coverage |

Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage |

Type, Application, End-User, Geography |

| Regional Scope |

North America, Europe, Asia Pacific, Middle East |

| Customized scope |

Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report |

Request a Free Sample Copy |

ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Competitive Landscape

The competitive landscape of the ISO 13709 (API 610) centrifugal pumps market is fairly consolidated, dominated by global players who compete on performance, reliability, product range, and service. Companies like Flowserve, Sulzer, KSB, ITT, Xylem, and Ebara are prominent, investing heavily in R&D to bring innovations like smart/IoT-enabled pumps, energy efficient designs, and improved materials to meet stringent standards. Strategic partnerships, mergers & acquisitions are common ways to expand portfolios and geographic presence—addressing demand in emerging markets. Regional or niche manufacturers carve out segments by specializing (e.g. harsh service, custom materials, small batch) or offering better after sales support to compete with large incumbents. High barriers to entry (due to regulatory / standard compliance, production costs) keep competition intense but with fewer new big entrants.

Here are 20 major players in the ISO 13709 (API 610) / industrial centrifugal pump:

- Flowserve Corporation

- Sulzer Ltd.

- KSB SE & Co. KGaA

- ITT (Goulds / ITT Inc.)

- Ebara Corporation

- Sundyne (a division of Honeywell)

- Ruhrpumpen Group

- Trillium Flow Technologies

- Pumpworks

- Truflo Pumps, Inc.

- Kirloskar Brothers Limited (Kirloskar / Kirloskar Pompen)

- Carver Pump

- Beijing Aerospace Propulsion Institute (No. 11 Institute)

- APX Flow

- PSG Dover

- Grundfos Holding A/S

- Xylem Inc.

- Wilo SE

- ANDRITZ AG

- DESMI A/S

Recent News:

- In May 2025, an article published by Centre for Life-Cycle Engineering and Management, Cranfield University, reported that AI-driven maintenance tool enhances the appeal of ISO 13709 (API 610) centrifugal pumps by significantly reducing downtime and maintenance costs—up to 80% in case studies. This drives market growth as industries seek more reliable, cost-effective solutions for critical operations. By enabling predictive maintenance using limited data, the tool supports wider adoption of high-performance pumps in oil & gas and other sectors. It also aligns with digital transformation trends, making API 610 pumps more attractive for smart, connected operations.

- In January 2024, an article published by Scientific and Technical Complex reported that study introduced a more accurate method for predicting the corrosion resistance of duplex stainless steels (DSSs), which have complex microstructures due to their dual-phase nature (austenite and ferrite) and the presence of secondary phases. Traditionally, corrosion resistance was estimated using the Pitting Resistance Equivalent Number (PREN), but this approach often overlooked the impact of secondary phases like niobium carbonitride and chromium nitride. Researchers investigated two DSS grades under identical heat treatments and observed opposite corrosion behaviors. To address this, they developed an improved metric called PRENeff (effective PREN), which accounted for individual phase contributions and secondary phases, offering better predictive accuracy. This approach helped define critical temperature ranges and provided a framework for designing new DSS compositions with enhanced corrosion resistance.

Frequently Asked Questions (FAQ) :

Q1. What are the main growth driving factors for this market?

The primary growth drivers are the increasing global demand for energy-efficient pumping systems and the expansion of the oil and gas sector. Industries are heavily investing in modernizing infrastructure and adopting pumps that comply with the ISO 13709/API 610 standards for high reliability and safety in harsh environments. Additionally, the rapid industrialization and urbanization, particularly in emerging economies, alongside growing investments in water and wastewater management, are significantly propelling the demand for these robust centrifugal pumps. Technological advancements, like the integration of IoT for predictive maintenance, also contribute to market growth.

Q2. What are the main restraining factors for this market?

The market is mainly restrained by the high initial capital investment required for acquiring and installing ISO 13709-compliant pumps, which can be a barrier for small and medium-sized enterprises. Furthermore, the specialized and complex nature of these high-performance pumps leads to higher maintenance and operational costs. The centrifugal pump technology itself can be sensitive to issues like cavitation and dry-run failures, which can damage pump components and reduce efficiency. Fluctuating raw material prices and stringent regulatory standards also impose additional cost and compliance burdens on manufacturers.

Q3. Which segment is expected to witness high growth?

The Oil and Gas segment, specifically for midstream and downstream applications, is expected to maintain its dominance and witness high growth due to increasing global energy demand and continuous investment in refining and transportation infrastructure. From a regional perspective, the Asia-Pacific region is projected to exhibit the fastest growth rate. This is driven by rapid industrialization, large-scale infrastructure projects, and expanding investment in petrochemical and water treatment facilities in countries like China and India, creating a strong demand for high-performance process pumps.

Q4. Who are the top major players for this market?

The ISO 13709 (API 610) centrifugal pumps market is dominated by a few major, established, global players. Key players, who collectively hold a significant market share, include Flowserve Corporation, KSB SE & Co. KGaA, and Sulzer Ltd. Other prominent companies are Ebara Corporation, Sundyne, Ruhrpumpen, and Trillium Flow Technologies. These top players focus on maintaining technological superiority, offering highly engineered, reliable pump solutions, and securing large contracts, particularly within the demanding petroleum, petrochemical, and power generation industries.

Q5. Which country is the largest player?

Based on regional market revenue share, Asia-Pacific is the largest geographical market for the broader centrifugal pump industry, driven significantly by China and India due to their rapid industrial and infrastructure growth. However, in terms of production and technological leadership for the specialized ISO 13709/API 610 pumps, North America (primarily the United States) holds a major share. This is supported by its mature industrial base, a strong focus on advanced manufacturing, and the significant presence of global market leaders within the region.

List of Figures

Figure 1: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue Breakdown (USD Billion, %) by Region, 2023 & 2029

Figure 2: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 3: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 4: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 5: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 6: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 7: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 8: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 9: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 10: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 11: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 12: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 13: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 14: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 15: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value (USD Billion), by Region, 2023 & 2029

Figure 16: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 17: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 18: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 19: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 20: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 21: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 22: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 23: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 24: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 25: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 26: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 27: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 28: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 29: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by U.S., 2018-2029

Figure 30: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Canada, 2018-2029

Figure 31: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 32: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 33: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 34: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 35: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 36: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 37: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 38: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 39: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 40: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 41: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 42: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 43: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 44: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Brazil, 2018-2029

Figure 45: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Mexico, 2018-2029

Figure 46: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Rest of Latin America, 2018-2029

Figure 47: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 48: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 49: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 50: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 51: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 52: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 53: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 54: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 55: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 56: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 57: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 58: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 59: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 60: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by U.K., 2018-2029

Figure 61: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Germany, 2018-2029

Figure 62: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by France, 2018-2029

Figure 63: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Italy, 2018-2029

Figure 64: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Spain, 2018-2029

Figure 65: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Russia, 2018-2029

Figure 66: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Rest of Europe, 2018-2029

Figure 67: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 68: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 69: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 70: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 71: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 72: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 73: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 74: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 75: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 76: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 77: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 78: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 79: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 80: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by China, 2018-2029

Figure 81: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by India, 2018-2029

Figure 82: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Japan, 2018-2029

Figure 83: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Australia, 2018-2029

Figure 84: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Southeast Asia, 2018-2029

Figure 85: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Rest of Asia Pacific, 2018-2029

Figure 86: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 1, 2023 & 2029

Figure 87: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 88: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 89: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 2, 2023 & 2029

Figure 90: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 91: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 92: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 93: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 94: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Value Share (%), By Segment 3, 2023 & 2029

Figure 95: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 96: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 97: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 98: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Others, 2018-2029

Figure 99: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by GCC, 2018-2029

Figure 100: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by South Africa, 2018-2029

Figure 101: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Forecast (USD Billion), by Rest of Middle East & Africa, 2018-2029

List of Tables

Table 1: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 2: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 3: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 4: Global ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Region, 2018-2029

Table 5: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 6: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 7: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 8: North America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 9: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 10: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 11: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 12: Europe ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 13: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 14: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 15: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 16: Latin America ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 17: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 18: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 19: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 20: Asia Pacific ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 21: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 22: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 23: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 24: Middle East & Africa ISO 13709 Centrifugal Pumps (Industrial ISO 13709 Centrifugal Pumps) Market Revenue (USD Billion) Forecast, by Country, 2018-2029