Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Positive Displacement Pumps Market encompasses the production, distribution, and use of pumps designed to move fluids by trapping a fixed amount and forcing it through an outlet. Unlike centrifugal pumps, positive displacement pumps deliver consistent flow regardless of pressure changes, making them ideal for high-viscosity, abrasive, or shear-sensitive liquids. Key types include gear, piston, diaphragm, rotary lobe, and peristaltic pumps, used across industries such as oil and gas, chemical processing, food and beverage, pharmaceuticals, and water treatment. Market growth is driven by industrial automation, stringent environmental regulations, and increasing demand for efficient fluid handling solutions.

The Global Positive Displacement Pumps market is experiencing steady growth driven by demand for precise fluid handling across industries like oil & gas, chemical processing, water/wastewater treatment, and food & beverage. Key trends include the development of energy-efficient and smart pump systems with IoT-enabled monitoring and predictive maintenance, improving uptime and reducing lifecycle costs. Rotary and reciprocating designs remain dominant, while emerging technologies such as peristaltic and magnetic-drive pumps gain traction for specialized applications.

Segmentation: The Global Positive Displacement Pumps market is segmented by Pump Type (Rotary Positive Displacement Pumps (Gear Pumps, Lobe Pumps, Screw Pumps, and Peristaltic Pumps), and Reciprocating Positive Displacement Pumps (Piston Pumps, Plunger Pumps, and Diaphragm Pumps), Discharge Pressure (Low Pressure (Up to 10 bar), Medium Pressure (10–50 bar) and High Pressure (Above 50 bar)), Operation (Electric Driven Pumps, Diesel Engine Driven Pumps, Hydraulic Driven Pumps and Manual Pumps), Material (Stainless Steel, Cast Iron, Alloy Steel, Plastic / Polymer and Others), End-User Industry (Oil & Gas, Chemical & Petrochemical, Water & Wastewater Treatment, Food & Beverage, Pharmaceuticals, Mining & Construction, Power Generation and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing industrial automation and process optimization is driving demand for positive displacement pumps globally. As manufacturing sectors expand, companies increasingly prioritize precise flow control, consistent delivery, and improved energy efficiency. Positive displacement pumps offer stable output regardless of pressure changes, making them ideal for high-viscosity fluids, chemicals, and dosing applications. Integration with smart sensors and predictive maintenance systems further enhances operational reliability and reduces downtime. As industries such as oil & gas, chemical processing, food & beverage, and pharmaceuticals modernize facilities, the need for advanced fluid-handling solutions continues to rise, supporting market growth.

Rising infrastructure investments in water supply and wastewater treatment are significantly boosting the positive displacement pumps market. Many regions are upgrading aging water networks and expanding treatment facilities to meet stricter environmental regulations and growing urban populations. Positive displacement pumps are well-suited for handling sludge, viscous fluids, and chemical dosing, ensuring consistent performance under varying conditions.

Government initiatives and public-private partnerships aimed at improving water quality and sustainability have accelerated demand for reliable pumping systems. For instance, EPA’s USD 450 million funding for the New England Heat Pump Accelerator Coalition accelerated global demand for positive displacement pumps by boosting heat pump adoption and related HVAC manufacturing. Increased electric heat pump deployment required more reliable fluid-handling systems, supporting higher sales of positive displacement pumps in residential and commercial heating applications worldwide.

Market Restraints

High initial costs and maintenance complexity of positive displacement pumps can restrain market growth, particularly for small and medium enterprises. Compared with centrifugal pumps, these systems often require more precise design and specialized components to handle varying fluid viscosities and pressures. Installation, calibration, and ongoing servicing may demand skilled technicians, increasing operational expenses. In addition, the risk of wear and tear when handling abrasive or corrosive fluids can shorten equipment life, further raising lifecycle costs. Budget constraints, especially in developing regions, may lead industries to choose lower-cost alternatives, slowing adoption despite performance advantages.

The positive displacement pumps market significantly influences global socioeconomic development by supporting essential industrial and municipal infrastructure. Reliable pumps enhance efficiency in oil & gas extraction, chemical manufacturing, and water treatment, facilitating job creation, industrial growth, and public health improvements. Investments in advanced pump technologies contribute to energy savings and reduced environmental impact, aligning with sustainable development goals. Market expansion stimulates manufacturing activity and trade, particularly in emerging economies where industrialization and urbanization fuel equipment demand.

Segmental Analysis:

The lobe pumps segment is expected to see the highest growth due to its versatility, gentle fluid handling, and ability to handle viscous and shear-sensitive liquids without damage. Widely used in food & beverage, pharmaceuticals, and wastewater treatment, lobe pumps deliver consistent flow and easy cleanability, meeting stringent hygiene standards. Their modular design allows customization for varied applications, driving adoption across industries focusing on quality and operational efficiency. Continued demand for efficient processing equipment, combined with innovations that reduce energy use and maintenance costs, further supports lobe pumps’ accelerated market growth over the forecast period.

The medium pressure (10–50 bar) segment is projected to grow fastest as it aligns with broad industrial requirements for balanced performance and energy efficiency. This pressure range suits many applications in chemical processing, water treatment, oil & gas, and manufacturing where high pressure is unnecessary but reliable, consistent flow is critical. Medium-pressure pumps offer flexibility, improved safety margins, and lower operational costs compared with high-pressure systems. As industries expand capacity and invest in modern infrastructure, demand for medium-pressure positive displacement pumps is rising due to their adaptability to diverse fluid properties, stable performance, and lower lifecycle expenses.

The hydraulic driven pumps segment is anticipated to achieve the highest growth owing to its strong suitability for heavy-duty and remote applications. Hydraulic pumps deliver high torque and controlled power, making them ideal for construction, mining, oil & gas, and industrial sectors that require robust performance under variable loads. Their ability to function in areas without reliable electrical infrastructure further fuels adoption. Continuous development in hydraulic systems that improve efficiency, reduce leakage, and offer better integration with mobile equipment enhances their competitiveness. This segment’s momentum reflects increasing demand for durable, high-force pumping solutions where precision and reliability are essential.

The alloy steel segment is expected to grow fastest due to its exceptional strength, corrosion resistance, and durability under challenging conditions. Alloy steel pumps are increasingly preferred in chemical, petrochemical, oil & gas, and wastewater applications where abrasive fluids and extreme environments demand tougher materials. Superior mechanical properties reduce maintenance frequency and extend service life, lowering total cost of ownership. As industries prioritize long-lasting, high-performance equipment that can withstand thermal, mechanical, and corrosive stress, alloy steel emerges as the material of choice. Ongoing innovations in metallurgy and fabrication further elevate alloy steel’s appeal in demanding pump applications.

The water & wastewater treatment segment is poised for highest growth due to global emphasis on clean water access and environmental sustainability. Aging infrastructure, stricter discharge regulations, and expanding urban populations drive increased investment in advanced pumping solutions for effective fluid management. Positive displacement pumps offer precise flow control and high reliability, essential for handling sludge, chemicals, and varied fluid viscosities typical in treatment facilities. Government initiatives and public–private partnerships to upgrade water systems also boost market demand. As municipalities modernize operations and focus on energy efficiency, this segment’s expansion reflects the critical role of robust pumping technology in ensuring safe, sustainable water services.

The Asia-Pacific region is expected to witness the highest growth in the positive displacement pumps market over the forecast period, driven by rapid industrialization, urbanization, and infrastructure development. Expanding oil & gas, chemical, and wastewater treatment sectors in China, India, and Southeast Asia are increasing demand for efficient and reliable fluid-handling solutions.

Additionally, rising investments in power generation and food & beverage processing are boosting pump adoption. For instance, in October 2024, EBARA’s 16 billion yen investment in Japan’s first full-scale liquid hydrogen pump test center is expected to strengthen the Asia-Pacific positive displacement pumps market by driving innovation in cryogenic and high-pressure pump technology. Real-world testing will accelerate development and validation of reliable, efficient pumps for hydrogen production, storage, and fueling infrastructure. This facility will support regional R&D, foster industry collaboration, and boost demand across energy, chemical, and industrial sectors, enhancing Asia-Pacific’s leadership in advanced fluid-handling solutions.

Government initiatives focused on water management and environmental compliance further support market expansion. The presence of manufacturing hubs and growing industrial automation also contribute to accelerated growth in the region. For instance, in 2024, Ingersoll Rand broadened its hydraulics capabilities by acquiring APSCO, Blutek, and UT Pumps, in a deal valued at USD 135 million. Thus, all such factors are fuelling this market’s growth in this region.

| Report Matrics | Details |

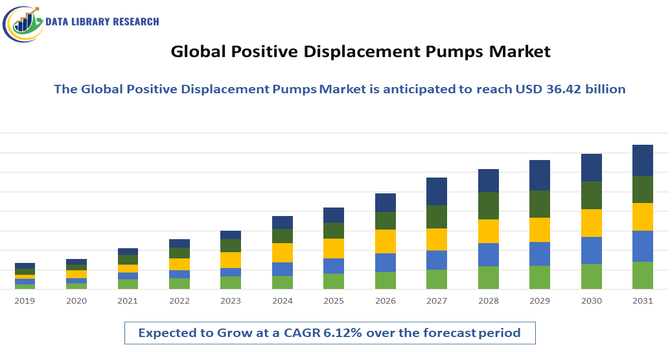

| Market Size Value | USD 36.42 billion |

| Growth Rate | CAGR of 6.12% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Positive Displacement Pumps market is moderately concentrated, featuring established industrial equipment manufacturers competing on technology, product range, and after-sales support. Leading companies such as Ingersoll Rand, SPX Flow, Alfa Laval, Flowserve, Grundfos, and IDEX focus on innovation, digital integration, and expanded service networks to differentiate offerings and capture market share. Competition centers on developing energy-efficient, low-maintenance pumps with enhanced reliability, while strategic partnerships, mergers, and geographic expansion strengthen global footprints. Market players also leverage customization for specific end-use sectors and invest in smart pump technologies to meet evolving customer demands and regulatory standards, creating both competitive challenges and growth opportunities.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Rapid industrialization and the expansion of the water and wastewater treatment sectors are primary drivers. These pumps are essential for handling high-viscosity fluids in the oil and gas, food and beverage, and pharmaceutical industries. Increasing demand for energy-efficient pumping solutions and stringent environmental regulations regarding fluid handling further propel market growth.

Q2. What are the main restraining factors for this market??

High initial investment costs and significant maintenance requirements act as major deterrents for small-scale enterprises. Positive displacement pumps are technically complex, leading to higher repair expenses compared to centrifugal alternatives. Additionally, fluctuations in raw material prices and the slowing of traditional oil and gas activities in certain regions may hinder market expansion.

Q3. Which segment is expected to witness high growth?

The hydraulic driven pumps segment is expected to grow fastest due to its strong suitability for heavy-duty and remote applications. With high torque, reliable performance under variable loads, and compatibility with mobile equipment, hydraulic pumps are increasingly adopted in construction, mining, and oil & gas, driving market growth over the forecast period.

Q4. Who are the top major players for this market?

Key industry participants include Flowserve Corporation, Grundfos Holding A/S, Sulzer Ltd., and Xylem Inc. Other significant players include Dover Corporation (PSG), ITT Inc., and IDEX Corporation. These companies maintain their market position through continuous R&D, strategic acquisitions, and the development of IoT-integrated smart pumping systems for industrial monitoring.

Q5. Which country is the largest player?

China is the largest player in the global market, driven by its massive manufacturing base and extensive investments in infrastructure. The country’s dominant position is supported by its booming chemical processing industry and large-scale water management projects. Furthermore, local government initiatives promoting industrial automation continue to solidify China’s lead in production and consumption.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model