Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global market for gearless machines for elevators is experiencing strong growth as rapid urbanization, proliferation of high-rise residential and commercial buildings, and increasing global investments in modern infrastructure drive demand for efficient vertical transportation. As cities densify and space becomes constrained, developers favour elevators equipped with gearless traction systems that deliver smoother, quieter, and faster rides — particularly in high-rise towers, offices, and premium housing.

The locomotive door market is increasingly being shaped by automation, safety enhancing technologies and sustainability-driven design — electrically operated, sensor-equipped sliding doors are rapidly replacing older pneumatic or manual systems as rail operators prioritize passenger safety, energy efficiency, and lower maintenance. There's also rising demand for lightweight, corrosion-resistant door materials (e.g. aluminum alloys or composites) and modular door systems that reduce overall train weight and improve energy efficiency, aligning with green transport initiatives and stricter emission/sustainability norms.

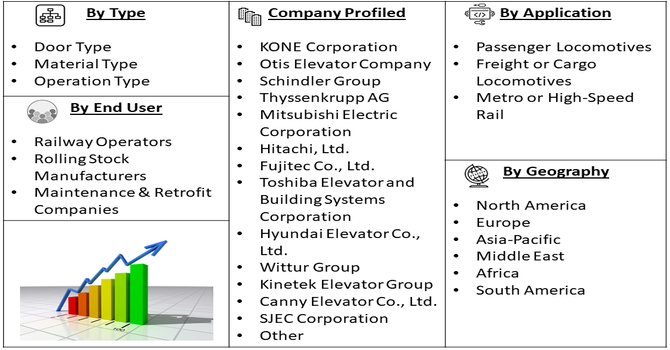

Segmentation: Global Locomotive Door Market is segmented By Door Type (Sliding Doors, Swing Doors, Folding Doors), Material Type (Aluminum, Stainless Steel, Composites / Lightweight Materials), Operation Type (Manual Doors, Pneumatic Doors, Electric / Motorized Doors), Application (Passenger Locomotives, Freight / Cargo Locomotives, Metro / High-Speed Rail), End-User (Railway Operators, Rolling Stock Manufacturers, Maintenance & Retrofit Companies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growth of urban populations and rapid industrialization is driving significant expansion in rail networks worldwide, particularly in developing regions such as the Asia-Pacific and parts of Africa. Governments and private operators are investing heavily in passenger trains, metro systems, and high-speed rail networks to improve public transportation efficiency, reduce traffic congestion, and meet environmental sustainability goals. For instance, In June 2025, Norfolk Southern unveiled a heritage locomotive in the classic Delaware & Hudson Railway livery, highlighting America’s rail legacy. This tribute emphasized how historical rail developments supported the expansion of rail infrastructure and urbanization. By connecting modern operations with the industry’s past, the locomotive underscored the role of pioneering rail companies in shaping cities and facilitating broader economic growth.

Rail operators and manufacturers are increasingly prioritizing passenger safety and operational efficiency. Modern locomotive doors are designed with advanced features such as obstacle detection sensors, real-time diagnostics, automatic locking mechanisms, and integration with train control systems. For instance, in June 2025, Ireland received two historic American locomotives, originally brought in during the 1960s, now relocated to County Down. Their preservation highlights the ongoing emphasis on safety, energy efficiency, and advanced technology in modern rail systems. This event underscores trends in the global locomotive door market, where innovative, compliant designs are increasingly essential for blending heritage with contemporary operational standards.

These innovations align with global trends toward sustainable, energy-efficient rail transport and stringent safety regulations, driving widespread adoption of advanced locomotive door systems across new and refurbished fleets.

Market Restraints:

Differences in safety, fire, and accessibility standards across regions create significant challenges for locomotive door manufacturers. Designs that meet one country’s requirements may fail in another, complicating certification and increasing development costs. Fire-resistant materials, emergency egress features, and accessibility compliance must often be customized for each market. This complexity affects production timelines, supply chains, and regulatory approval processes, making global deployment more difficult. In the global locomotive door market, manufacturers must navigate these regional variations while balancing cost, durability, and performance. Companies that successfully manage compliance gain a competitive advantage in expanding international markets.

Segmental Analysis

The global locomotive door segment is expected to witness the highest growth over the forecast period due to increasing investments in rail infrastructure, rapid expansion of urban transit and high-speed rail systems, and growing demand for advanced doors that offer enhanced safety, energy efficiency, and compliance with modern rolling stock standards.

Sliding doors are the most commonly used door type in modern locomotives, metro trains, and high-speed rail systems due to their space-efficient design and ease of operation. These doors allow quick passenger boarding and alighting, reduce platform dwell times, and are compatible with automated and sensor-controlled systems, enhancing safety and operational efficiency. Sliding doors are particularly preferred in urban transit systems with high passenger traffic.

Aluminum is increasingly used in locomotive door manufacturing because of its lightweight, corrosion-resistant, and durable properties. Using aluminum reduces the overall weight of the train, which in turn lowers energy consumption and improves fuel efficiency. Aluminum doors also contribute to smoother operations and easier handling during maintenance, making them ideal for modern passenger and metro trains.

Electric or motorized doors are gaining prominence over manual and pneumatic systems due to their automation, smoother operation, and integration with modern safety features such as obstacle detection and remote monitoring. They reduce human intervention, improve operational reliability, and are suitable for high-speed and high-frequency rail applications.

Passenger locomotives represent a key application segment for locomotive doors. These doors are critical for ensuring passenger safety, efficient boarding, and energy efficiency in long-distance trains, urban commuter trains, and metro systems. Features like automatic operation, quiet performance, and durable construction are essential in this segment.

Railway operators are the primary end-users driving demand for advanced locomotive doors. Operators seek durable, safe, and low-maintenance door solutions to enhance passenger experience, comply with regulatory standards, and optimize operational efficiency. Continuous investments in fleet modernization and new rail projects further support market growth.

The Asia-Pacific region is projected to experience the highest growth in the global locomotive door market over the forecast period. Rapid urbanization, expanding rail networks, and increasing investments in high-speed and freight rail infrastructure are key drivers in countries such as China, India, and Japan. For instance, in June 2025, India’s Prime Minister unveiled the country’s first D9-9000 horsepower electric locomotive, marking a major milestone in rail modernization. Developed with advanced engineering, its critical components were produced by Siemens Mobility in Indian cities such as Nashik, Aurangabad, and Mumbai. The launch underscores India’s emphasis on domestic manufacturing and the adoption of state-of-the-art electric rail technology.

Rising demand for modern, safe, and energy-efficient locomotives is pushing manufacturers to adopt advanced door technologies that meet stringent safety, fire, and accessibility standards. Additionally, government initiatives supporting domestic manufacturing and rail modernization further boost market growth. As a result, the region is expected to dominate the locomotive door market, attracting both global and local industry players.

| Report Matrics | Details |

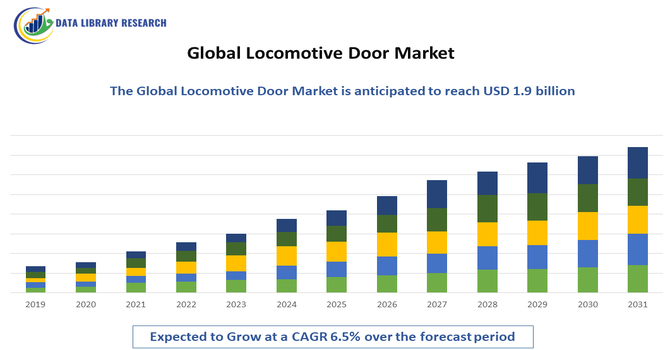

| Market Size Value | USD 0.576 billion |

| Growth Rate | CAGR of 6.5% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the global locomotive door market is highly dynamic and consists of established rolling stock manufacturers, specialized door system suppliers, and innovative technology providers. Companies compete based on product quality, material technology, energy efficiency, safety features, automation, and compliance with international standards. Key strategies include the development of lightweight, corrosion-resistant doors, integration of smart sensors and IoT-based monitoring, and expansion into emerging rail markets. Strategic partnerships, mergers, acquisitions, and continuous R&D to enhance durability, noise reduction, and operational efficiency are common, as firms aim to cater to rising demand from passenger locomotives, metro systems, and high-speed rail networks. Providers with strong after-sales service networks and global distribution capabilities are better positioned to capture a larger market share.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is heavily driven by global rail network expansion and modernization, especially the shift toward high-speed rail and urban mass transit systems. Governments worldwide are investing heavily in new infrastructure and replacing old rolling stock. This focus on improving passenger safety and comfort, alongside the demand for reliable automated systems, increases the need for advanced door sets.

Q2. What are the main restraining factors for this market?

A key challenge is the long life cycle of railway rolling stock, often lasting 20-30 years, meaning door systems are not frequently replaced unless they fail. Furthermore, the high initial cost associated with sophisticated door technologies, especially electric and pneumatic automated systems, can limit new purchases for operators with tighter budget constraints or those managing older, regional fleets

Q3. Which segment is expected to witness high growth?

The passenger locomotive segment is anticipated to exhibit the strongest growth. Increasing urbanization and the rise in daily commuter and intercity traffic are boosting the demand for modern, high-speed passenger trains. These applications require high-performance, complex entrance doors that prioritize rapid passenger throughput, enhanced sealing, and superior safety features compared to freight or utility doors.

Q4. Who are the top major players for this market?

The market includes key global railway equipment suppliers and specialized door system manufacturers. Top players often include Nabtesco Corporation, Knorr-Bremse AG, Faiveley Transport (now part of Wabtec), and Schaltbau Holding AG. These major companies provide integrated door control and drive systems, relying on robust technology and strategic partnerships with the primary locomotive builders.

Q5. Which country is the largest player?

China is recognized as the largest player, dominating the market through its massive, continuous investment in railway expansion. The country possesses the world's most extensive high-speed rail network and a robust domestic manufacturing sector, led by companies like CRRC Corporation Limited, which drives unparalleled volume in both new locomotive production and the subsequent demand for sophisticated door systems.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model