Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Luxury Pet Furniture Market refers to the industry focused on high-end, premium-quality furniture and accessories designed specifically for pets, including beds, sofas, climbing structures, and feeding stations. These products emphasize aesthetics, comfort, durability, and innovative designs that align with owner lifestyles. The market caters to pet owners seeking stylish, functional, and durable solutions that enhance both pet well-being and home décor.

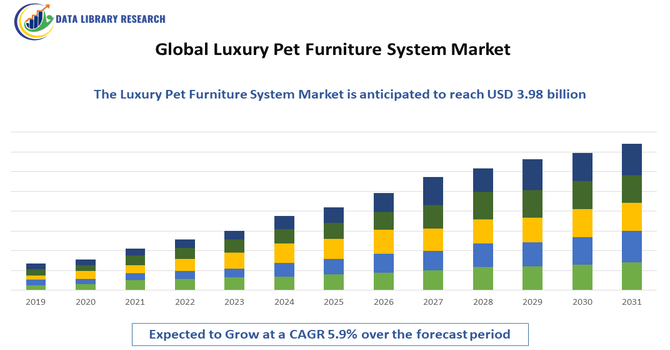

The Global Luxury Pet Furniture Market is driven by rising pet humanization, increasing disposable incomes, and growing awareness of pet comfort and wellness. Urbanization and premium lifestyle trends encourage owners to invest in stylish, functional, and high-quality furniture. Additionally, innovative designs, use of eco-friendly and durable materials, and expanding e-commerce channels enhance accessibility and adoption. The growing demand for customized, designer pet furniture further accelerates market growth globally.

The luxury pet furniture market is evolving with strong consumer demand for designer, eco-conscious, and multifunctional pieces that harmonize with home décor. Premium materials like memory foam, walnut wood, and memory foam blends are increasingly used. Smart furniture with built-in heating or connectivity features is gaining traction. Customization—such as monogrammed beds or modular climbing systems—is also a major trend. Furthermore, direct-to-consumer e-commerce platforms and curated boutique collections are shaping how affluent pet owners shop for luxury pet furnishings.

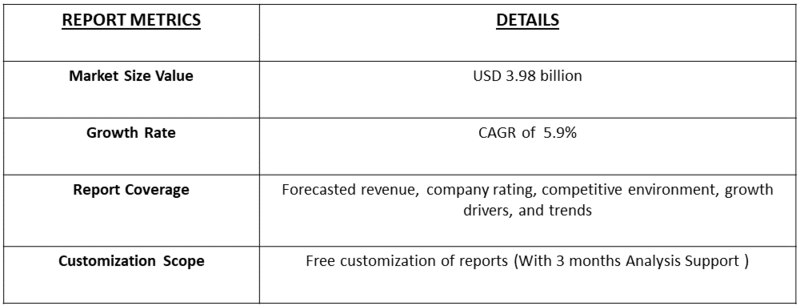

Segmentation: The Global Luxury Pet Furniture Market is segmented by Product Type (Beds & Sofas, Houses & Condos, Scratching Posts & Trees, Dining & Feeding Furniture, and Other Furniture), Animal Type (Dogs, Cats and Others), Distribution Channel (Online/E-commerce and Offline/Retail Stores), Material (Wood & Metal, Fabric & Textile, and Plastic & Composites), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing trend of pet humanization is a primary driver of the Global Luxury Pet Furniture Market. Pet owners increasingly regard pets as family members, prompting investments in high-quality, stylish, and functional furniture that enhances both comfort and home décor. Rising disposable incomes, particularly among urban households, support spending on premium beds, sofas, and multifunctional furniture. Designer collaborations, customization options, and innovative materials such as memory foam, leather, and sustainable wood further fuel adoption. Social media influence and lifestyle trends encourage consumers to purchase luxury furniture that aligns with their personal aesthetic. This focus on comfort, design, and premiumization continues to drive strong demand, expanding the market globally across all major regions.

The expansion of e-commerce and direct-to-consumer (DTC) channels is significantly boosting the luxury pet furniture market. Online platforms provide convenience, broader product selection, competitive pricing, and access to designer or niche brands that may not be available locally. Consumers can compare products, read reviews, and order customized or premium furniture from the comfort of their homes. The adoption of smartphones, secure digital payments, and efficient logistics networks supports this growth. Additionally, subscription-based models and curated online marketplaces increase repeat purchases. E-commerce also allows brands to reach international markets, expanding their customer base. Collectively, these trends drive higher sales, enhance market penetration, and accelerate growth in the luxury pet furniture segment globally.

Market Restraints:

A key restraint for the Global Luxury Pet Furniture Market is the high cost associated with premium and designer products. Luxury beds, sofas, and furniture crafted from materials such as leather, memory foam, wood, and metal can be prohibitively expensive for middle-income pet owners. Customization, designer collaborations, and limited-edition collections further increase prices, limiting accessibility to affluent consumers only. Additionally, recurring costs for replacement parts, maintenance, and accessories add financial burden. In emerging markets, lack of awareness and lower disposable incomes hinder adoption. High costs may also divert consumers toward affordable alternatives or mass-market products, slowing market penetration. Consequently, pricing remains a significant barrier to wider adoption, restraining overall growth in the luxury pet furniture segment.

The growing market for luxury pet furniture reflects rising disposable income, especially among urban, affluent pet owners who view pets as family members. This humanization of pets drives spending on high-end, design-forward products that align with owner lifestyles. As pet adoption rises, so does investment in premium, long-lasting furniture. Moreover, increased online retail penetration empowers niche luxury brands to reach customers globally, fueling economic growth in the specialized pet furnishing segment and creating jobs in design, manufacturing, and logistics sectors.

Segmental Analysis:

The Beds & Sofas segment is expected to witness the highest growth over the forecast period due to increasing demand for comfortable, stylish, and multifunctional furniture for pets. Pet owners are increasingly prioritizing both aesthetics and functionality, seeking furniture that complements home décor while providing maximum comfort. Innovations such as memory foam mattresses, orthopedic support, and washable covers are driving adoption.

The humanization of pets, coupled with rising disposable incomes, encourages owners to invest in premium sleeping and lounging solutions. Additionally, customized and designer beds and sofas are gaining traction among affluent consumers. As pets spend more time indoors, demand for high-quality beds and sofas that enhance comfort and well-being continues to expand globally. For instance, in October 2023, Bedsure, a textile manufacturer based in California, U.S., introduced an exclusive pet product line featuring the Bedsure Sherpa dog bed, a slow rebound dog bed, and a supportive foam dog bed. Thus, such factrs are driving this segment’s growth.

The dogs segment is projected to witness the highest growth over the forecast period, driven by the large and growing population of pet dogs worldwide. Dogs are increasingly viewed as family members, prompting owners to invest in premium furniture that offers comfort, style, and functionality. The rising prevalence of urban living has increased demand for compact, stylish, and multi-purpose furniture suitable for apartments and homes. Specialized beds, sofas, and modular furniture designed specifically for dogs are gaining popularity. Additionally, trends in dog humanization and social media influence encourage owners to purchase designer furniture. Rising spending on dog health, wellness, and lifestyle products further fuels growth in this segment globally.

The Online/E-commerce segment is expected to witness the highest growth during the forecast period, driven by convenience, wider product availability, and competitive pricing. Increasing internet penetration, smartphone usage, and digital payment adoption have transformed purchasing behaviors among pet owners. Online platforms allow consumers to access a diverse range of luxury pet furniture, compare products, read reviews, and order customized or designer items from the comfort of their homes. The COVID-19 pandemic further accelerated e-commerce adoption, establishing long-term buying habits. E-commerce also enables brands to reach global markets, reducing geographic limitations. Subscription services, direct-to-consumer models, and curated online marketplaces further enhance accessibility, making online channels the fastest-growing segment in the luxury pet furniture market.

The Wood & Metal segment is projected to witness the highest growth over the forecast period, driven by demand for durable, premium-quality, and aesthetically appealing pet furniture. Pet owners increasingly prefer furniture crafted from natural wood, steel, and aluminum for longevity, strength, and modern design appeal. These materials allow for multifunctional designs, modular structures, and customization, aligning with contemporary home interiors. The durability of wood and metal ensures long-term usage, justifying higher investment by consumers. Rising awareness of eco-friendly and sustainably sourced materials further boosts the segment. Additionally, designers are combining wood and metal with fabrics, memory foam, and other luxury finishes to create sophisticated beds, sofas, and furniture sets, enhancing adoption globally.

The North America region is expected to witness the highest growth over the forecast period due to high pet ownership rates, strong consumer spending, and a growing trend of pet humanization. Affluent pet owners in the region increasingly prioritize comfort, wellness, and home-integrated designs when purchasing luxury pet furniture.

Advanced retail infrastructure, widespread e-commerce adoption, and availability of designer brands further accelerate market expansion. Also, prominent companies are prioritizing the development of eco-friendly products using sustainable materials. For example, in April 2023, Naturepedic, a bedding company based in Ohio, U.S., introduced its organic dog bed collection. This new line includes GOTS-certified latex and organic cotton, emphasizing environmentally responsible manufacturing. This shift towards sustainable and eco-friendly pet furniture strengthens the North American market by appealing to environmentally conscious consumers. As demand for green products rises, brands like Naturepedic set new industry standards, encouraging innovation and driving competitive advantage. The focus on organic and non-toxic materials aligns with regional regulatory trends and consumer values, promoting growth and increasing market share for sustainable luxury pet furniture in North America.

Additionally, rising awareness about pet health, ergonomics, and quality materials encourages investment in premium beds, sofas, and furniture. Partnerships between luxury furniture designers and pet product companies, along with strong marketing initiatives, further stimulate demand. Collectively, these factors position North America as the dominant and fastest-growing region in the luxury pet furniture market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Luxury Pet Furniture Market features established pet brands, designer furniture houses, and emerging boutique firms vying for affluent consumers. Companies differentiate through premium materials, bespoke designs, sustainability, and smart furniture features. Strategic collaborations between pet accessory brands and high-end furniture designers amplify reach. E-commerce channels and direct-to-consumer models intensify competition, while niche players focus on customization and craftsmanship. Mergers, acquisitions, and partnerships continue to reshape the landscape, with innovation and design leadership as key determinants of market success.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the pervasive trend of pet humanization, where owners treat their pets as family members and are willing to spend significant amounts on their comfort and luxury. This sentiment is coupled with rising disposable incomes in developed economies, enabling owners to purchase high-end, designer furniture that blends seamlessly with modern home décor. Furthermore, the increasing urbanization and smaller living spaces necessitate multifunctional and aesthetically pleasing pet products that serve both the pet's needs and the owner's design preferences.

Q2. What are the main restraining factors for this market?

The most significant constraint is the high price point of luxury pet furniture, which limits the market to a very niche, affluent consumer base, excluding the majority of general pet owners. Unlike essential pet supplies, this furniture is considered a non-essential, discretionary purchase, making the market highly vulnerable to economic downturns. Additionally, the durability challenge persists, as pets can easily damage or outgrow expensive items, leading to consumer hesitation regarding the substantial investment.

Q3. Which segment is expected to witness high growth?

The Designer Beds and Sofas Segment is anticipated to witness the highest growth. These products are replacing simple mats or plastic beds as owners seek ergonomic support combined with bespoke, aesthetically pleasing designs that match high-end interior furnishings. Growth is driven by innovations in materials, such as orthopedic memory foam, hypoallergenic fabrics, and sustainable wood frames, justifying the premium price tag. The visual appeal and the perception of superior pet comfort strongly influence purchasing decisions in this segment.

Q4. Who are the top major players for this market?

The market is fragmented, comprising both established luxury interior brands that have diversified into pet accessories and specialized high-end pet retailers. Top players include MiaCara, known for its minimalist European design; Tuft & Needle (expanding its human sleep expertise to pets); and smaller, niche brands like Pets Stop and Enchanted Home Pet. These players focus on design innovation, premium materials (leather, solid wood), and strong direct-to-consumer (D2C) marketing strategies to build their exclusive brand identity.

Q5. Which country is the largest player?

The United States, located within the North American region, is the largest consumer market for luxury pet furniture. This dominance is driven by the country's huge pet-owning population, high rates of disposable income, and a strong, established culture of pet humanization. The presence of major e-commerce platforms and influential social media trends that showcase high-end pet living spaces further accelerate consumer demand and spending on premium, designer items that reflect their personal luxury lifestyle.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model