Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global market for medical nucleic acid rapid hybridization instruments refers to worldwide sales and use of devices that quickly hybridize DNA/RNA for diagnostics and research—covering instruments, geographies, product types and applications, across hospitals and labs.

The global market for Medical Nucleic Acid Rapid Hybridization Instruments is experiencing robust growth, primarily fueled by the accelerating worldwide prevalence of infectious diseases and various types of cancer, which necessitates rapid, sensitive, and accurate molecular diagnostic solutions in clinical and research settings. A crucial driver is the continuous advancement and maturation of molecular diagnostic technologies, including significant improvements in instrument sensitivity, specificity, and the integration of full automation features that enhance laboratory workflow efficiency and throughput.

The Global Medical Nucleic Acid Rapid Hybridization Instrument Market is witnessing notable trends such as the integration of automation and AI/ML algorithms to enhance detection accuracy and reduce manual errors, along with a growing shift toward portable and point-of-care hybridization systems that enable rapid diagnostics outside traditional laboratories. Advancements in miniaturization and user-friendly interface designs are making these instruments more accessible to healthcare professionals, while increasing adoption in precision medicine, infectious disease testing, and early genetic disorder detection is driving consistent technological innovation and market expansion.

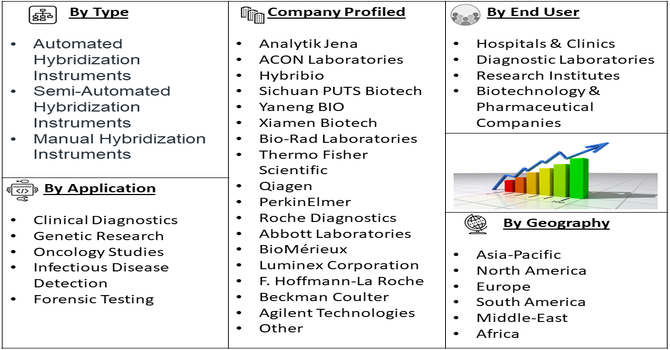

Segmentation: Global Medical Nucleic Acid Rapid Hybridization Instrument Market is segmented By Product Type (Automated Hybridization Instruments, Semi-Automated Hybridization Instruments, Manual Hybridization Instruments), Application (Clinical Diagnostics, Genetic Research, Oncology Studies, Infectious Disease Detection, Forensic Testing), End-User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Biotechnology & Pharmaceutical Companies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing global burden of infectious diseases such as COVID-19, tuberculosis, and HIV, along with a surge in genetic and hereditary disorders, is a major factor driving the demand for medical nucleic acid rapid hybridization instruments. These instruments play a vital role in enabling precise and fast identification of pathogens or genetic anomalies through DNA and RNA analysis.

In 2025, an article published by American Journal of Medical Genetics, reported the UDN (Undiagnosed Diseases Network) cohort (2,799 subjects), 766 (27.4%) were diagnosed, and 93.4% had a genetic disease. 4.2% of diagnosed subjects had multiple molecular diagnoses, with some having up to three concurrent Mendelian disorders, underscoring the high incidence and complexity of genetic diseases despite prior genome sequencing. The rising prevalence of infectious and genetic diseases is driving the growth of the global Medical Nucleic Acid Rapid Hybridization Instrument market, as demand for faster, more accurate molecular diagnostics continues to increase worldwide.

With the growing emphasis on early diagnosis and timely treatment, healthcare providers and diagnostic laboratories are increasingly adopting advanced hybridization instruments that offer high sensitivity, accuracy, and reduced turnaround times. This rising need for reliable molecular diagnostic tools across both developed and developing nations is significantly propelling market growth.

Continuous innovations in molecular biology and automation technologies are transforming nucleic acid hybridization methods, making them faster, more accurate, and user-friendly. Modern instruments now integrate automation, AI-based data interpretation, and high-throughput capabilities, enabling simultaneous analysis of multiple samples with minimal human intervention. Such advancements have improved reproducibility, reduced operational errors, and increased laboratory efficiency.

In 2021, BD (Becton, Dickinson and Company) launched a new fully automated, high-throughput diagnostic system that utilized robotics and advanced sample management software algorithms, setting a new standard for automation in infectious disease molecular testing across core and centralized laboratories in the United States. Additionally, the trend toward compact and automated hybridization platforms for point-of-care and near-patient testing is expanding market accessibility and applications, especially in decentralized healthcare settings. These technological breakthroughs are a key growth driver enhancing the overall adoption and performance of nucleic acid rapid hybridization instruments globally.

Market Restraints:

The growth of the global medical nucleic acid rapid hybridization instrument market is restrained by several factors, including the high cost of equipment and maintenance, which limits adoption among small and medium-sized diagnostic laboratories and research centers. The complexity of operation and requirement for skilled personnel to handle hybridization procedures and data interpretation also pose challenges, particularly in developing regions with limited technical expertise. Additionally, stringent regulatory approval processes for diagnostic instruments slow down product commercialization and market entry. Moreover, the availability of alternative molecular diagnostic methods, such as real-time PCR and next-generation sequencing (NGS), which offer faster and more versatile results, further constrains the market’s expansion potential.

The global Medical Nucleic Acid Rapid Hybridization Instrument market has significant socioeconomic impact, driving advancements in molecular diagnostics, early disease detection, and personalized medicine. By enabling faster, more accurate identification of infectious and genetic diseases, these instruments help reduce healthcare costs through timely intervention and improved patient outcomes. The market’s growth also stimulates employment opportunities in biotechnology, healthcare, and manufacturing sectors, while promoting technological innovation and global collaboration in medical research. Additionally, increased accessibility to advanced diagnostic tools in developing regions enhances public health infrastructure, narrowing healthcare disparities and supporting sustainable economic development.

Segmental Analysis

The Automated Hybridization Instruments segment is expected to dominate the market during the forecast period, owing to its ability to deliver high precision, reproducibility, and reduced hands-on time. Automation minimizes human errors and enhances throughput, making it highly suitable for large-scale diagnostic and research applications. The increasing adoption of automated platforms in clinical and genomic laboratories is fueling segmental growth.

In October 2025, Volta Labs, a pioneer in next-generation sequencing (NGS) sample preparation solutions, announced the launch of the Hybridization Capture App for the Twist Standard Hybridization v2 Kit on the Callisto platform. Co-developed with Twist Bioscience, the method combined Twist’s advanced hybrid capture chemistry with Volta’s fully automated Callisto system, enabling researchers and clinical laboratories to achieve highly consistent enrichment performance with a streamlined workflow. This launch accelerated adoption of automated hybridization instruments, enhancing workflow efficiency and reliability, while driving growth in the Global Medical Nucleic Acid Rapid Hybridization Instrument market.

The Clinical Diagnostics segment holds the largest share, driven by the rising prevalence of infectious diseases and genetic disorders requiring rapid and accurate molecular testing. The growing emphasis on personalized medicine and the need for early and precise diagnosis have accelerated the use of nucleic acid hybridization instruments in clinical laboratories and hospitals.

The Diagnostic Laboratories segment leads the market due to their widespread use of hybridization instruments for routine disease screening, genetic testing, and pathogen detection. These laboratories are increasingly adopting advanced instruments to improve efficiency and accuracy while meeting growing diagnostic demands. @@@@ In September 2025, Volta Labs announced that the Prinses Máxima Center for Pediatric Oncology had acquired the Callisto platform to streamline sample preparation across multiple genomics workflows, supporting both Illumina and Oxford Nanopore Technologies (ONT) sequencing platforms. As Europe’s largest pediatric cancer center, the implementation enhanced efficiency, reproducibility, and reduced hands-on time for laboratory staff. This adoption strengthened the Diagnostic Laboratories segment by enabling faster, more reliable molecular testing and contributed to growth in the Global Medical Nucleic Acid Rapid Hybridization Instrument market through increased demand for automated, high-throughput hybridization solutions.

The North America region is expected to witness the highest growth over the forecast period, driven by the strong presence of advanced healthcare infrastructure, increasing investments in molecular diagnostics, and widespread adoption of innovative hybridization technologies. The region’s high prevalence of infectious and genetic diseases, coupled with growing awareness of early disease detection, has significantly boosted the demand for medical nucleic acid rapid hybridization instruments.

Additionally, robust R&D activities supported by government funding, well-established biotechnology and pharmaceutical industries, and the rapid integration of automation and AI in diagnostic workflows are fueling market expansion. For instance, in January 2025, Leica Biosystems, a global leader in cancer diagnostics and workflow solutions, and Molecular Instruments (MI), the inventor of HCR Imaging technology, announced a partnership to enable fully integrated RNA-ISH using the BOND RX and BOND RXm research staining systems. This collaboration enhanced North America’s Global Medical Nucleic Acid Rapid Hybridization Instrument market by accelerating the adoption of automated RNA analysis technologies, improving research efficiency, and strengthening regional leadership in molecular diagnostics innovation and precision medicine.

The United States, in particular, dominates the regional market due to the presence of leading manufacturers, favorable regulatory frameworks, and the rising focus on personalized medicine and precision diagnostics. For instance, in October 2023, President Biden issued a landmark Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence, directing the federal government to reduce risks related to synthetic nucleic acids and enhance biosecurity measures. The National Science and Technology Council (NSTC) and OSTP subsequently developed a unified framework to screen purchases of synthetic nucleic acids and benchtop synthesis equipment, ensuring secure and ethical use. This initiative strengthened North America’s regulatory landscape, fostering a favorable environment for innovation, compliance, and growth within the Global Medical Nucleic Acid Rapid Hybridization Instrument market through improved biosafety and accountability. Thus, such factors are driving the growth of above market in North American region.

| Report Matrics | Details |

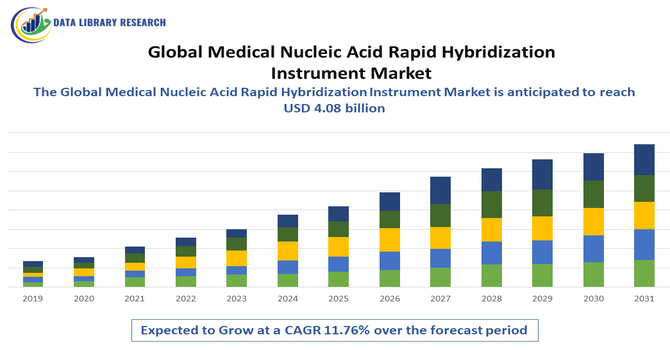

| Market Size Value | USD 4.08 billion |

| Growth Rate | CAGR of 11.76% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global medical nucleic acid rapid hybridization instrument market is highly competitive, characterized by technological innovation, strategic partnerships, and continuous R&D investments. Leading players focus on developing automated, high-throughput, and portable hybridization systems to enhance diagnostic accuracy and speed. The market also witnesses growing collaborations between biotechnology firms and diagnostic laboratories to expand application areas and improve global accessibility.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the escalating demand for rapid, sensitive, and accurate molecular diagnostic techniques, which are crucial for timely clinical decisions. The rising global prevalence of infectious diseases, including emerging viral outbreaks, and the growing adoption of personalized medicine for cancer and genetic disorders fuel this demand. Furthermore, technological advancements leading to Point-of-Care (POC) testing devices that offer fast results outside of central labs are significantly expanding the market's reach and utility.

Q2. What are the main restraining factors for this market?

The growth of this market is chiefly restrained by the high cost of advanced instruments, specialized reagents, and probes. These significant capital expenses limit adoption, particularly in emerging economies and smaller healthcare facilities. Additionally, the technical complexities associated with nucleic acid hybridization procedures, which require meticulous sample preparation, highly skilled personnel, and optimization for different sample types, pose a continuous challenge to widespread implementation.

Q3. Which segment is expected to witness high growth?

The Infectious Disease Diagnosis application segment is expected to witness high growth, driven by the continuous global threat of new pathogens and the necessity for rapid, specific detection of viral and bacterial agents. Furthermore, the Reagents and Kits product segment is projected to show the highest growth rate. This is due to the constant need for high-purity, standardized, and diverse probes and kits that ensure accuracy and reproducibility across various clinical and research assays.

Q4. Who are the top major players for this market?

The global market for molecular diagnostic instruments and related hybridization technologies is dominated by major life science and diagnostics companies. Key players include Thermo Fisher Scientific Inc., F. Hoffmann-La Roche AG, QIAGEN, Abbott Laboratories, and Becton, Dickinson and Company (BD). These companies maintain their market leadership through continuous R&D investment in automated, high-throughput systems and proprietary probe chemistries to enhance assay sensitivity and speed.

Q5. Which country is the largest player?

North America, spearheaded by the United States, holds the largest market share by revenue. This dominance is attributed to a highly advanced healthcare infrastructure, substantial government and private funding in genomics and biomedical research, and the early, widespread adoption of advanced molecular diagnostic technologies. High rates of infectious disease testing and the push for personalized medicine further solidify the U.S.'s leading position in the adoption of rapid hybridization instruments.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model