Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global 4D Ultrasonic Instrument Market refers to the industry focused on developing, manufacturing, and distributing advanced ultrasound systems that provide real-time 3D imaging with temporal (4D) visualization for medical diagnostics. The Global 4D Ultrasonic Instrument Market is experiencing robust growth, primarily driven by the rising demand for advanced diagnostic imaging technologies in healthcare. The increasing prevalence of chronic diseases, high-risk pregnancies, and the growing need for early and accurate detection of fetal and cardiac abnormalities are key factors fueling market expansion. Technological advancements, such as real-time 4D imaging and enhanced image resolution, have significantly improved diagnostic accuracy, encouraging healthcare providers to adopt these instruments. Additionally, the rising awareness of maternal and fetal health, coupled with increasing investments in healthcare infrastructure, particularly in emerging economies, is further propelling market growth.

The global 4D ultrasound instrument market is witnessing transformative trends in 2025, driven by significant technological advancements and evolving clinical demands. Artificial Intelligence (AI) integration is at the forefront, enhancing diagnostic accuracy through automated image interpretation, real-time guidance, and predictive analytics, thereby streamlining workflows and reducing human error. Furthermore, the application of 4D ultrasound is expanding beyond obstetrics to include cardiology, oncology, and neurology, with innovations like High-Intensity Focused Ultrasound (HIFU) enabling non-invasive treatments for conditions such as uterine fibroids and pancreatic tumors. Collectively, these trends are reshaping the landscape of diagnostic imaging, making it more accessible, efficient, and precise.

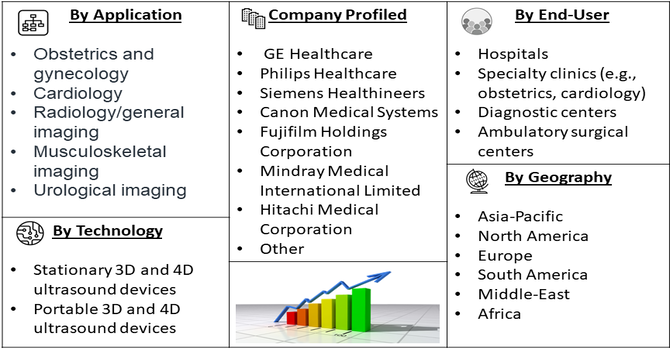

Segmentation: Global 4D Ultrasonic Instrument Market is segmented By Technology (Stationary 3D and 4D ultrasound devices, Portable 3D and 4D ultrasound devices), Portability (Trolley or cart-based ultrasound systems, Compact/handheld ultrasound systems, Point-of-care (PoC) ultrasound systems), Application(Obstetrics and gynecology, Cardiology, Radiology/general imaging, Musculoskeletal imaging, Urological imaging), End-User (Hospitals, Specialty clinics (e.g., obstetrics, cardiology), Diagnostic centers, Ambulatory surgical centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing prevalence of chronic diseases, high-risk pregnancies, and cardiovascular disorders has significantly increased the demand for precise and non-invasive diagnostic tools. For instance, in 2024, the CDC reported that approximately 805,000 people in the United States experienced a heart attack each year. Of these, 605,000 were first-time heart attacks, while 200,000 occurred in individuals who had previously suffered a heart attack. 4D ultrasonic instruments provide real-time, high-resolution imaging, enabling healthcare professionals to monitor fetal development, detect congenital abnormalities, and assess cardiac function more accurately. Unlike traditional 2D or 3D ultrasound systems, 4D ultrasonography allows dynamic visualization, offering a comprehensive view of organ structures and movement, which improves diagnostic confidence. This demand is further fueled by hospitals and diagnostic centers aiming to enhance patient outcomes, reduce misdiagnosis, and adopt state-of-the-art imaging technologies.

Rapid technological innovations are a major driver in the 4D ultrasonic instrument market. The integration of artificial intelligence (AI) and machine learning algorithms allows for automated image analysis, anomaly detection, and workflow optimization, reducing human error and increasing efficiency. Furthermore, advancements in miniaturization have led to portable and handheld 4D ultrasound devices, expanding access to point-of-care diagnostics in remote areas, emergency care, and home healthcare. For instance, in February 2025, PIUR IMAGING, a global player in tomographic 3D ultrasound technology, received FDA clearance for PIUR tUS inside, integrated with select GE HealthCare LOGIQ ultrasound systems. This approval enabled U.S. healthcare providers to enhance imaging workflows and utilize advanced AI-supported 3D imaging capabilities. These innovations not only improve image quality and diagnostic speed but also support early detection and timely intervention, making 4D ultrasonic instruments more attractive to healthcare providers globally.

Market Restraints:

Advanced 4D ultrasound systems come with significant capital expenditures, often exceeding USD 100,000. This high cost includes not only the purchase price but also ongoing maintenance, software updates, and specialized training for operators. Such financial burdens can deter smaller clinics, hospitals in emerging markets, and point-of-care facilities from adopting these technologies. Moreover, the cost-intensive nature of advanced 4D ultrasound systems can limit accessibility and slow market penetration in price-sensitive regions. Even with high diagnostic value, smaller healthcare providers may prioritize more affordable imaging alternatives, delaying widespread adoption. This has prompted manufacturers to explore leasing models, modular systems, and portable solutions to reduce upfront expenses and expand reach, ultimately supporting broader utilization of 4D ultrasound technology in both developed and emerging healthcare markets.

The Global 4D Ultrasound Technology Market has had significant socioeconomic impacts by enhancing diagnostic capabilities and improving patient care across multiple medical disciplines, including cardiology, obstetrics, and critical care. By providing real-time, high-resolution imaging, 4D ultrasound has enabled earlier detection of complex conditions, reducing hospitalizations, treatment costs, and long-term healthcare burdens. The technology has also stimulated employment and skill development in healthcare and biomedical engineering sectors, fostering innovation and high-tech workforce growth. However, high capital costs and maintenance requirements have limited adoption in smaller clinics and emerging markets, highlighting disparities in access. Overall, 4D ultrasound technology has strengthened healthcare quality, promoted medical education, and driven economic growth within the global medical imaging industry.

Segmental Analysis:

Portable 3D and 4D ultrasound devices are witnessing significant adoption due to their compact design, ease of transportation, and ability to deliver real-time imaging comparable to stationary systems. These devices are particularly favored in emergency care, outpatient facilities, and remote healthcare settings where space and mobility are critical. The growing preference for bedside diagnostics, coupled with technological advancements like AI-assisted imaging and wireless connectivity, enhances their utility. This segment is expected to show strong growth as hospitals and clinics seek flexible imaging solutions that reduce patient movement and streamline workflow.

Point-of-care ultrasound systems allow healthcare professionals to perform imaging at the patient’s bedside, enabling immediate diagnosis and treatment decisions. These systems are increasingly used in critical care units, emergency rooms, and home healthcare services. Their rapid deployment, combined with user-friendly interfaces and high-resolution imaging, makes them indispensable for quick assessments of cardiac function, obstetric monitoring, and trauma evaluation. The growing demand for decentralized and patient-centric care is driving the expansion of this segment globally.

The obstetrics and gynecology segment dominates the application spectrum for 4D ultrasonic instruments. These devices provide real-time visualization of the fetus, helping monitor growth, detect congenital anomalies, and assess maternal-fetal health accurately. The high adoption rate is driven by increasing awareness of maternal health, rising prenatal care standards, and the ability of 4D ultrasound to offer detailed imaging for fetal heart rate, facial features, and movement. The segment is expected to grow steadily as more healthcare providers integrate advanced imaging in routine prenatal care.

Hospitals are the largest end-users of 4D ultrasonic instruments due to their high patient volumes and diverse diagnostic needs. Large-scale hospitals invest in advanced imaging systems to provide comprehensive diagnostic services across multiple departments, including obstetrics, cardiology, and radiology. The demand is further driven by the need for precise diagnostics, high throughput, and integration with hospital information systems (HIS). Hospitals in emerging economies are also expanding infrastructure, creating a growing market for 4D ultrasound systems.

North America is a leading market for 4D ultrasonic instruments, driven by advanced healthcare infrastructure, high healthcare expenditure, and early adoption of innovative medical technologies. The presence of major market players, widespread awareness of maternal and cardiac health, and reimbursement support for advanced imaging procedures contribute to strong regional growth.

The United States, in particular, is a key contributor due to high adoption rates in hospitals and diagnostic centers, supported by continuous technological innovation and regulatory support. For instance, in 2021, CAE Healthcare launched CAE Vimedix 3.2, an advanced simulation software offering enhanced fidelity, ultrasonography realism, 3D/4D ultrasound, and multiplanar reconstruction (MPR) across its platform. The system enabled remote ultrasound training in cardiology, emergency medicine, ICU, and Ob/Gyn, featuring a library of over 200 pathologies. It supported virtual lectures, lesson-building, ICCU e-learning, and hands-on practice with manikins and probes, including transgastric abdominal ultrasonography exercises. The launch aimed to improve cognitive and psychomotor skills, ensuring medical students and professionals achieved clinical preparedness and patient safety in critical care scenarios. Thus, such developments are fueling the growth of the studied market in this region.

| Report Matrics | Details |

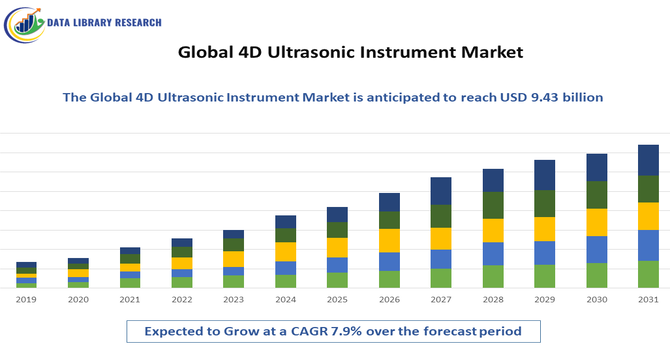

| Market Size Value | USD 9.43billion |

| Growth Rate | CAGR of 7.9% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global 4D ultrasonic instrument market is characterized by a competitive landscape featuring a mix of established multinational corporations and specialized regional players. These companies are actively engaged in product innovation, strategic partnerships, and expanding their market presence to cater to the growing demand for advanced imaging solutions in healthcare. Key players are focusing on integrating artificial intelligence, enhancing image quality, and developing portable systems to meet diverse clinical needs across various applications, including obstetrics, cardiology, and musculoskeletal imaging.

Key Players:

Recent Development

Q1. What are the main growth driving factors for this market?

The market is mainly driven by the growing demand for advanced diagnostic imaging, especially for applications like fetal, cardiac, and abdominal scans. Key factors include continuous technological advancements leading to more portable and user-friendly devices, an aging global population requiring more sophisticated diagnostic tools, and increasing emphasis on preventative healthcare and early disease detection. The superior, real-time visualization of 4D ultrasound allows for more accurate diagnoses, bolstering adoption in various medical settings.

Q2. What are the main restraining factors for this market?

The primary constraints are the high initial cost of purchasing and maintaining advanced 4D ultrasonic instruments. This financial burden is particularly challenging for smaller healthcare facilities and providers in developing regions. Additionally, the need for specialized training for medical professionals to effectively operate and utilize the complex 4D systems acts as another barrier to widespread adoption and market penetration.

Q3. Which segment is expected to witness high growth?

The "Portable 4D Ultrasonic Instrument" segment is anticipated to witness significant growth. This is due to the rising trend of point-of-care diagnostics, which requires compact and easily movable systems. The demand for improved accessibility in remote or underserved areas, coupled with technological advancements leading to miniaturization and enhanced functionality, drives the high growth of portable and handheld devices.

Q4. Who are the top major players for this market?

The global market for 4D ultrasonic instruments is dominated by a few key multinational healthcare technology companies. The top major players include industry giants like GE HealthCare, Koninklijke Philips N.V. (Philips Healthcare), and Siemens Healthineers. Other significant players are FUJIFILM Corporation and Canon Medical Systems Corporation, all known for their advanced product portfolios and extensive R&D.

Q5. Which country is the largest player?

Based on market share and adoption of advanced systems, the North American region, with the United States as a major contributor, currently holds the largest share of the 4D ultrasonic instrument market. This dominance is primarily driven by high healthcare expenditure, established advanced healthcare infrastructure, and the early adoption of new, sophisticated imaging technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model