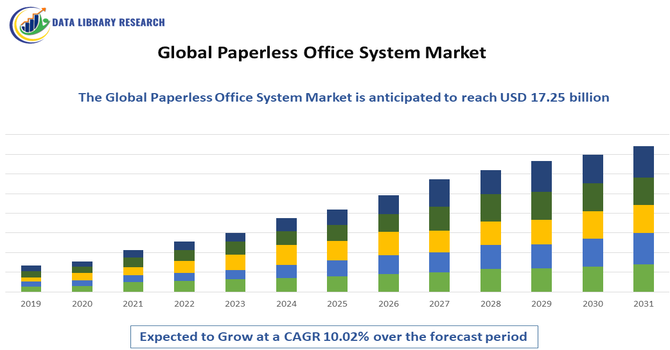

The Global Paperless Office System Market is valued at approximately USD 4.9 billion in 2026, the market is projected to grow at a CAGR of over 10.02%, reaching to USD 17.25 billion by 2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Paperless Office System Market refers to digital solutions that reduce or eliminate paper use in business operations by converting documents into electronic formats. These systems include document management software, workflow automation, electronic signature tools, and cloud-based storage, enabling organizations to create, share, store, and retrieve information digitally. They support functions such as HR, finance, legal, and administrative processes by improving efficiency, reducing physical storage needs, and enhancing collaboration. Adoption is driven by cost savings, sustainability goals, regulatory compliance, and the rise of remote work.

The Global Paperless Office System market is increasingly driven by digital transformation, remote work, and automation. Organizations are adopting cloud-based document management and workflow tools to streamline operations and improve collaboration across teams. AI and machine learning are being integrated for smarter document classification, data extraction, and automated approvals. Electronic signatures and secure digital storage are becoming standard, reducing reliance on physical paperwork.

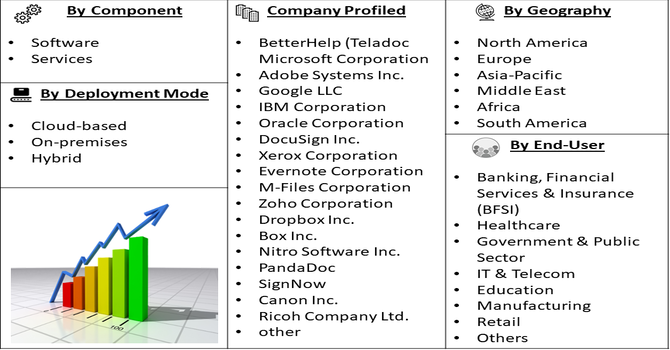

Segmentation: The Global Paperless Office System market is segmented by Component (Software (Document Management Systems (DMS), Workflow Automation, E-signature & Digital Approval, Content Management and Data Capture & OCR), and Services (Consulting & Implementation, Maintenance & Support and Training & Integration), Deployment Mode (Cloud-based, On-premises and Hybrid), End-User Industry (Banking, Financial Services & Insurance (BFSI), Healthcare, Government & Public Sector, IT & Telecom, Education, Manufacturing, Retail and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global shift toward digital transformation and remote work has significantly accelerated demand for paperless office systems. Organizations are replacing manual, paper-based processes with digital workflows to support remote collaboration and maintain operational continuity. Cloud-based document management and e-signature tools enable employees to access, share, and approve documents from anywhere, improving efficiency and reducing turnaround time. As businesses adapt to hybrid work models, the need for secure, scalable, and integrated paperless solutions continues to rise. This trend is particularly strong in sectors where documentation is heavy and time-sensitive, such as finance, healthcare, and government.

Cost savings and environmental sustainability are major drivers of paperless office adoption. By reducing paper consumption, printing, and physical storage needs, organizations can cut operational expenses and improve workplace efficiency. Paperless systems also support corporate sustainability goals by lowering carbon footprint and minimizing waste. For instance, Fujitsu Laboratories’ digital trust technology strengthened the paperless office market by ensuring document authenticity and integrity. It verified who created data and whether it was altered, boosting confidence in digital workflows and supporting wider adoption of paperless systems across businesses and government.

Many businesses are integrating green policies into their corporate strategies, making digital document workflows a priority. In addition, paperless processes help companies comply with regulations related to records management and data security, making them more attractive for organizations seeking both financial and environmental benefits.

Market Restraints:

Despite the advantages, paperless office systems face challenges related to data security and regulatory compliance. Digitizing sensitive documents increases the risk of cyber threats such as data breaches, unauthorized access, and ransomware attacks. Organizations must invest in strong encryption, access controls, and secure storage solutions, which can increase implementation costs. Additionally, compliance requirements vary across regions and industries, creating complexity in managing electronic records and ensuring legal validity of digital signatures. These concerns can slow adoption, particularly among highly regulated sectors and organizations with limited IT capabilities, making it harder for some businesses to transition fully to paperless operations.

Paperless office systems contribute significantly to cost savings, environmental sustainability, and operational efficiency. By reducing paper consumption, printing, and physical storage needs, businesses lower expenses and shrink their carbon footprint. The shift supports faster decision-making and improved productivity through automated workflows and instant document access. It also enhances data security by enabling encryption, access controls, and audit trails, reducing risks associated with physical documents. On a broader scale, paperless systems support remote work and digital inclusion, enabling businesses to operate seamlessly across regions. This transformation also promotes greener practices and helps organizations meet sustainability goals and compliance standards.

Segmental Analysis:

The e-signature and digital approval segment is expected to see the highest growth over the forecast period as businesses prioritize faster, secure, and legally valid document workflows. Organizations are increasingly replacing physical signatures with digital alternatives to accelerate contract approvals, HR onboarding, and procurement processes. E-signatures reduce turnaround time, improve auditability, and enable remote collaboration, which is especially valuable in hybrid work environments. Regulatory acceptance of digital signatures across many regions has also boosted adoption. As companies strive to streamline operations and enhance compliance, e-signature and digital approval solutions are becoming essential components of paperless office systems.

The cloud-based segment is expected to experience the highest growth over the forecast period due to its flexibility, scalability, and ease of deployment. Cloud paperless systems allow organizations to access documents and workflows from anywhere, supporting remote and hybrid work models. They reduce the need for costly infrastructure and offer automatic updates, seamless collaboration, and secure storage. Cloud platforms also enable faster implementation and integration with other business tools, making them ideal for businesses of all sizes. As organizations seek more agile and cost-effective solutions, cloud-based paperless office systems continue to gain traction worldwide.

The IT & telecom segment is expected to witness the highest growth over the forecast period as companies in this sector increasingly adopt digital workflows to manage large volumes of documentation and customer data. Telecom and IT firms rely heavily on contracts, service agreements, invoices, and compliance records, making paperless systems essential for efficiency and speed. Additionally, these industries are early adopters of cloud and digital technologies, enabling quick implementation of document management, e-signature, and workflow automation solutions. As digital transformation accelerates in IT and telecom, demand for paperless office systems is expected to rise significantly.

The North American region is expected to witness the highest growth over the forecast period due to strong digital adoption, robust IT infrastructure, and high awareness of workplace automation. Businesses in North America are rapidly transitioning to paperless systems to enhance productivity, reduce costs, and improve compliance.

In July 2025, SCCA’s launch of a digital signature service strengthened the global paperless office system market by promoting legally binding e-signatures in arbitration and ADR processes. It enhanced document authenticity and compliance, supporting secure digital workflows in legal and dispute resolution settings. The move also aligned with global efforts to recognize electronic arbitration, boosting adoption of paperless solutions in international legal practice.

The region also benefits from favorable regulatory support for digital signatures and secure electronic records. With a large number of enterprises embracing cloud-based technologies and remote work, demand for paperless office solutions is growing steadily. Thus, North America remains a key driver for market expansion due to its advanced digital ecosystem and strong technology adoption.

| Report Matrics | Details |

| Market Size Value | USD 17.25 billion |

| Growth Rate | CAGR of 10.02% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the paperless office system market is dynamic and fragmented, featuring established software giants, niche providers, and emerging cloud-based startups. Major players compete on factors like platform scalability, integration capabilities, security features, and user experience. Differentiation often comes through advanced automation, AI-powered document processing, and industry-specific solutions. Partnerships and acquisitions are common as companies seek to expand offerings and enter new markets. Vendors also focus on improving mobile access and collaboration tools to cater to hybrid work environments. As demand rises, competition is expected to intensify, driving continuous innovation in digital document management and workflow automation.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the rising demand for eco-friendly personal mobility solutions in congested urban areas. Increasing fuel prices and growing environmental awareness push consumers toward electric alternatives. Furthermore, advancements in sensor technology and battery efficiency have improved safety and range, making these scooters attractive for short-distance commuting.

Q2. What are the main restraining factors for this market?

Growth is hampered by stringent government regulations regarding the use of self-balancing vehicles on public roads and sidewalks. Safety concerns, including high-profile battery fire incidents and rider injuries, have led to product recalls and negative perceptions. High initial costs compared to traditional kick-scooters also limit adoption in price-sensitive regions.

Q3. Which segment is expected to witness high growth?

The dual-wheel segment is expected to witness the highest growth due to its superior stability and ease of use for beginners. Unlike unicycles, dual-wheel scooters appeal to a broader demographic, including the elderly and children. Their increasing integration with smart features like Bluetooth and mobile app tracking further boosts popularity.

Q4. Who are the top major players for this market?

The market is dominated by Ninebot (which acquired Segway), Xiaomi Corporation, and Razor USA LLC. Other significant players include Hovertrax, Swagtron, and Koowheel. These companies maintain their leadership through continuous R&D, strong global distribution networks, and strategic branding that targets both tech enthusiasts and urban commuters seeking efficient transportation.

Q5. Which country is the largest player?

China is the largest player in this market, serving as both the leading manufacturer and a massive consumer base. The country's dominance is supported by its advanced electronic manufacturing infrastructure and government subsidies for electric vehicle production. Cities like Shenzhen serve as global hubs for the innovation and export of these devices.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model