PEGylation Proteins Technology Market Overview and Analysis

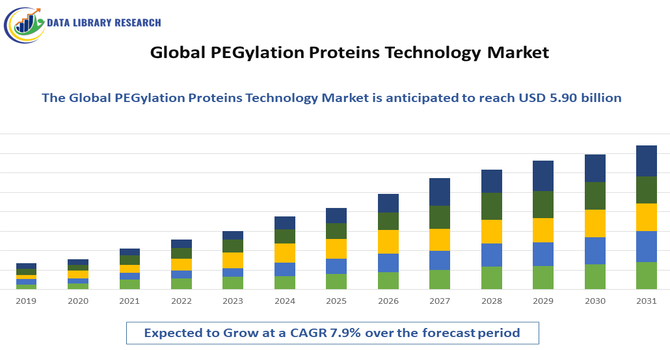

- The PEGylation Proteins Technology market size was valued at USD 2.12 billion in 2025. The market is expected to grow from USD 5.90 billion in 2032, growing with a CAGR of 8.6% from 2025-2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Global PEGylation Proteins Technology refers to the field focused on chemically or enzymatically attaching polyethylene glycol (PEG) to proteins, enhancing their stability, half-life, solubility, and therapeutic efficacy worldwide. The Global PEGylation Proteins Technology Market is witnessing substantial growth, primarily driven by the increasing demand for enhanced therapeutic proteins with improved pharmacokinetics and reduced immunogenicity. PEGylation technology extends the half-life of biologics, improves drug stability, and reduces dosing frequency, making treatments more effective and patient-friendly. The rising prevalence of chronic diseases such as cancer, autoimmune disorders, and rare genetic conditions is fueling the adoption of PEGylated protein therapies.

PEGylation Proteins Technology Market Latest Trends

The Global PEGylation Proteins Technology Market is witnessing several key trends that are reshaping the biopharmaceutical landscape. One prominent trend is the development of site-specific PEGylation techniques, which allow precise attachment of polyethylene glycol (PEG) chains to proteins, enhancing efficacy while minimizing side effects. Additionally, there is a growing focus on long-acting PEGylated biologics that reduce dosing frequency, improving patient compliance and convenience. The integration of novel PEG derivatives and multifunctional PEG molecules is enabling the creation of more stable and targeted therapeutics. Furthermore, collaborations between biotech firms and contract research organizations (CROs) are accelerating the development of innovative PEGylated drugs across oncology, autoimmune, and rare disease segments, reflecting a shift towards personalized and precision medicine.

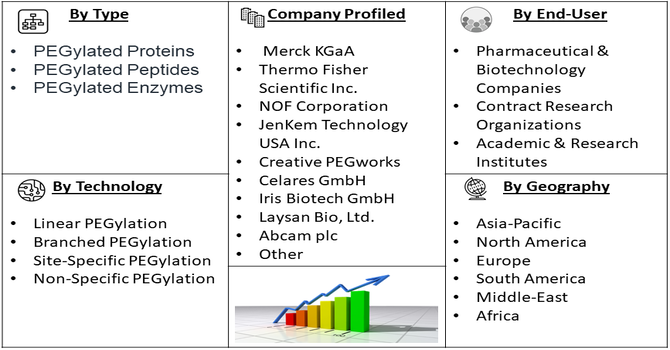

Segmentation: Global PEGylation Proteins Technology Market is segmented By Product Type (PEGylated Proteins, PEGylated Peptides, PEGylated Enzymes), Technology (Linear PEGylation, Branched PEGylation, Site-Specific PEGylation, Non-Specific PEGylation), End-User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

- Rising Demand for Enhanced Therapeutic Proteins

The primary driver of the PEGylation proteins technology market is the growing demand for biologics with improved therapeutic properties. PEGylation enhances the solubility, stability, and half-life of proteins, enzymes, and peptides, allowing for longer circulation in the bloodstream and reduced dosing frequency. This not only improves treatment efficacy but also enhances patient compliance, especially for chronic diseases such as cancer, autoimmune disorders, and rare genetic conditions.

In July 2025, an article titled, “Development of a Long-Acting Myeloid-Derived Growth Factor via Site-Specific PEGylation” reported that researchers developed a long-acting MYDGF by site-specific PEGylation at its C-terminus to overcome its short in vivo half-life. Human MYDGF with a C-terminal Asn-Ala-Leu motif was ligated to an azido-functionalized tetrapeptide using [G238V]BmAEP1, then conjugated with DBCO-PEG30,000 via copper-free click chemistry. The resulting PEG-MYDGF retained activity, showed prolonged half-life in mice, and enhanced wound healing in diabetic models, demonstrating therapeutic potential. This advancement highlighted the advantages of precise, enzymatic PEGylation, stimulated innovation in PEGylation technologies, and expanded applications of PEGylated proteins, thereby strengthening growth and competitiveness in the global PEGylation proteins technology market.

- Advancements in PEGylation Technology and Biopharmaceutical R&D

Continuous technological advancements in PEGylation processes are significantly fueling market growth. Innovations such as site-specific PEGylation allow precise attachment of polyethylene glycol molecules to target proteins, minimizing side effects while maintaining therapeutic activity. Additionally, the development of branched and multifunctional PEG molecules has expanded the scope of protein modification, enabling more stable and targeted drug delivery.

Pharmaceutical companies have increasingly formed strategic alliances with global partners to develop and commercialize PEGylated protein therapies. For example, in September 2022, Asahi Kasei Pharma partnered with Swedish Orphan Biovitrum to distribute pegcetacoplan, a PEGylated peptide for paroxysmal nocturnal hemoglobinuria, in Japan. These collaborations facilitated technology transfer, accelerated innovation, and expanded market access, while also enhancing PEGylation techniques and strengthening biopharmaceutical R&D. By promoting cross-border knowledge sharing and joint research, they have driven the development of more efficient, targeted, and long-acting biologics, advancing global progress in advanced drug delivery systems.

Market Restraints:

- High Cost of PEGylation Processes and Therapeutics

The development and production of PEGylated proteins involve complex chemical processes, specialized equipment, and stringent quality control measures, making them significantly more expensive than conventional biologics. This high cost of development, coupled with expensive end products, limits accessibility in price-sensitive markets and can slow adoption among smaller healthcare providers and emerging economies. Additionally, the regulatory and manufacturing challenges associated with PEGylated proteins further contribute to increased costs and longer development timelines. Ensuring batch-to-batch consistency, safety, and efficacy requires advanced analytical tools and compliance with rigorous global standards. These factors often restrict large-scale commercialization and limit participation of smaller biopharma firms, thereby creating a barrier to widespread adoption despite the strong therapeutic potential of PEGylated biologics.

Socio Economic Impact on PEGylation Proteins Technology Market

The Global PEGylation Proteins Technology market has had significant socio-economic impacts by improving healthcare outcomes and stimulating economic growth. By enabling the development of long-acting, stable, and safer biologics, PEGylation has enhanced patient access to advanced therapies for cancer, autoimmune, cardiovascular, and rare diseases, reducing hospitalizations and healthcare costs. The technology has also driven pharmaceutical and biotechnology R&D, creating high-skilled jobs and fostering innovation in drug development. Additionally, strategic partnerships, clinical advancements, and regulatory approvals have strengthened global supply chains and promoted investment in advanced manufacturing infrastructure. However, high development and production costs can limit accessibility in price-sensitive regions, highlighting the need for policies supporting equitable distribution of PEGylated therapeutics. Overall, PEGylation has advanced both health and economic growth globally.

Segmental Analysis:

- PEGylated Proteins segment is expected to witness highest growth over the forecast period

PEGylated proteins represent the largest product segment in the market due to their widespread therapeutic applications. PEGylation improves protein stability, solubility, and half-life, making these therapeutics more effective and convenient for patients, particularly in chronic diseases such as cancer, autoimmune disorders, and rare genetic conditions. Pharmaceutical companies prefer PEGylated proteins as they reduce dosing frequency, enhance patient compliance, and lower immunogenicity risks, contributing to strong adoption across hospitals and specialty care centers.

- Site-Specific PEGylation segment is expected to witness highest growth over the forecast period

Site-specific PEGylation is gaining traction as it allows precise attachment of polyethylene glycol molecules to specific sites on protein structures, ensuring therapeutic activity is preserved while minimizing side effects. This technique enables controlled pharmacokinetics, higher efficacy, and reduced immunogenicity compared to non-specific PEGylation. The adoption of site-specific PEGylation is particularly prominent in oncology and rare disease therapeutics, where precision and safety are critical, driving this segment’s growth significantly.

- Pharmaceutical & Biotechnology Companies segment is expected to witness highest growth over the forecast period

Pharmaceutical and biotechnology companies are the primary end-users of PEGylation technologies, as they are responsible for developing and commercializing PEGylated therapeutics. These organizations invest heavily in research and development to innovate protein modification techniques, improve drug stability, and expand therapeutic pipelines. Their focus on novel PEGylated biologics across multiple therapeutic areas, including cancer, autoimmune, and cardiovascular diseases, positions them as a key driver of market growth.

Moreover, the increasing demand for long-acting and targeted therapies has prompted these companies to adopt advanced PEGylation and alternative conjugation technologies to enhance drug efficacy and patient compliance. Strategic collaborations, licensing agreements, and FDA approvals of PEGylated products have further accelerated market expansion. As a result, the growing integration of PEGylation into biologic drug development pipelines continues to strengthen the competitive landscape and innovation potential of the global pharmaceutical and biotechnology sectors.

- North America region is expected to witness highest growth over the forecast period

North America dominates the PEGylation proteins technology market due to advanced healthcare infrastructure, high adoption of biologics, and strong regulatory and reimbursement frameworks supporting innovative therapies. The presence of leading pharmaceutical and biotechnology companies, coupled with substantial R&D investments and increasing prevalence of chronic and rare diseases, drives the region’s market growth. @@@@@ The United States, in particular, is a hub for PEGylation research, development, and commercialization, contributing significantly to global market revenue. For instance, The FDA’s approval of eflapegrastim-xnst (ROLVEDON) in September 2022 significantly accelerated the adoption of PEGylation technology across the U.S. biopharmaceutical sector. This milestone spurred market growth, encouraged broader application of PEGylated drugs in various therapeutic areas, and enhanced patient access to advanced, long-acting treatments, strengthening the overall innovation landscape of the U.S. PEGylation proteins market.

Similarly, In July 2024, Aligos Therapeutics entered into an agreement with Xiamen Amoytop Biotech to conduct Phase 1b clinical trials of ALG-000184 in combination with PEGBING (Mipeginterferon alfa-2b), a PEGylated Interferon alfa-2b. This collaboration enhanced PEGylation process optimization, expanded its therapeutic applications, and strengthened the role of PEGylated biologics in advancing modern medical treatments. @@@@@ Thus, such collaborations and clinical advancements have accelerated PEGylation technology adoption across the North American biopharma sector. They have stimulated R&D investments and cross-border partnerships, driving innovation in biologics. Consequently, the region has experienced robust market growth and strengthened leadership in advanced drug delivery technologies.

| Report Matrics |

Details |

| Market Size Value |

USD 5.90 billion |

| Growth Rate |

CAGR of 8.6% |

| Forecast |

2026-2033 |

| Historical data |

2021-2024 |

| Base Year |

2025 |

| Report Coverage |

Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage |

Type, Application, End-User, Geography |

| Regional Scope |

North America, Europe, Asia Pacific, Middle East |

| Customized scope |

Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report |

Request a Free Sample Copy |

PEGylation Proteins Technology Market Competitive Landscape

The Global PEGylation Proteins Technology Market is characterized by a competitive landscape featuring a mix of established multinational corporations and specialized regional players. These companies are actively engaged in product innovation, strategic partnerships, and expanding their market presence to cater to the growing demand for advanced PEGylated therapeutics. Key players are focusing on integrating artificial intelligence, enhancing drug stability, and developing long-acting formulations to meet diverse clinical needs across various applications, including oncology, autoimmune disorders, and rare diseases.

Key Players:

- Merck KGaA

- Thermo Fisher Scientific Inc.

- NOF Corporation

- JenKem Technology USA Inc.

- Creative PEGworks

- Celares GmbH

- Quanta BioDesign, Ltd.

- Biomatrik Inc.

- Iris Biotech GmbH

- Laysan Bio, Ltd.

- Abcam plc

- Enzon Pharmaceuticals, Inc.

- Profacgen

- Aurigene Pharmaceutical Services Ltd.

- NOF America Corp.

- Polypure AS

- Nektar Therapeutics

- Molecular Partners AG

- Horizon Therapeutics plc

- Takeda Pharmaceuticals Company Limited

Recent Development

- In June 2025, Biopharma PEG obtained U.S. FDA DMF approval for its self-developed HZ-PEG-HZ (1K) product (DMF No. 041864), showcasing its strong R&D and manufacturing expertise in high-quality PEG derivatives and ensuring reliable, compliant support for global pharma partners. This milestone boosted confidence in PEG-based technologies, expanded Biopharma PEG’s global footprint, and stimulated innovation and competition in the Global PEGylation Proteins Technology Market, driving growth and higher regulatory standards worldwide.

- In September 2022, A Bavarian consortium of XL-protein GmbH, Wacker Chemie AG, and LMU Munich developed a long-acting anti-CD40 antibody fragment using XL-protein’s PASylation® technology, funded by the Bavarian Research Foundation. The project aimed to enable safer, more effective immunosuppression for cardiac xenotransplantation and autoimmune diseases. This innovation boosted global interest in PASylation as a next-generation alternative to PEGylation, spurred R&D investments, and reshaped the protein modification market toward safer, long-acting biologics.

List of Figures

Figure 1: Global PEGylation Proteins Technology Market Revenue Breakdown (USD Billion, %) by Region, 2022 & 2029

Figure 2: Global PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 3: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 4: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 5: Global PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 6: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 7: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 8: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 9: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 10: Global PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 11: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 12: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 13: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 14: Global PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 15: Global PEGylation Proteins Technology Market Value (USD Billion), by Region, 2022 & 2029

Figure 16: North America PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 17: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 18: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 19: North America PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 20: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 21: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 22: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 23: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 24: North America PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 25: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 26: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 27: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 28: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 29: North America PEGylation Proteins Technology Market Forecast (USD Billion), by U.S., 2018-2029

Figure 30: North America PEGylation Proteins Technology Market Forecast (USD Billion), by Canada, 2018-2029

Figure 31: Latin America PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 32: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 33: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 34: Latin America PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 35: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 36: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 37: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 38: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 39: Latin America PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 40: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 41: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 42: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 43: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 44: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Brazil, 2018-2029

Figure 45: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Mexico, 2018-2029

Figure 46: Latin America PEGylation Proteins Technology Market Forecast (USD Billion), by Rest of Latin America, 2018-2029

Figure 47: Europe PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 48: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 49: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 50: Europe PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 51: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 52: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 53: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 54: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 55: Europe PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 56: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 57: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 58: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 59: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 60: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by U.K., 2018-2029

Figure 61: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Germany, 2018-2029

Figure 62: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by France, 2018-2029

Figure 63: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Italy, 2018-2029

Figure 64: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Spain, 2018-2029

Figure 65: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Russia, 2018-2029

Figure 66: Europe PEGylation Proteins Technology Market Forecast (USD Billion), by Rest of Europe, 2018-2029

Figure 67: Asia Pacific PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 68: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 69: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 70: Asia Pacific PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 71: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 72: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 73: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 74: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 75: Asia Pacific PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 76: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 77: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 78: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 79: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 80: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by China, 2018-2029

Figure 81: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by India, 2018-2029

Figure 82: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Japan, 2018-2029

Figure 83: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Australia, 2018-2029

Figure 84: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Southeast Asia, 2018-2029

Figure 85: Asia Pacific PEGylation Proteins Technology Market Forecast (USD Billion), by Rest of Asia Pacific, 2018-2029

Figure 86: Middle East & Africa PEGylation Proteins Technology Market Value Share (%), By Segment 1, 2022 & 2029

Figure 87: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 88: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 89: Middle East & Africa PEGylation Proteins Technology Market Value Share (%), By Segment 2, 2022 & 2029

Figure 90: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 91: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 92: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 93: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 94: Middle East & Africa PEGylation Proteins Technology Market Value Share (%), By Segment 3, 2022 & 2029

Figure 95: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 1, 2018-2029

Figure 96: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 2, 2018-2029

Figure 97: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Sub-Segment 3, 2018-2029

Figure 98: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Others, 2018-2029

Figure 99: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by GCC, 2018-2029

Figure 100: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by South Africa, 2018-2029

Figure 101: Middle East & Africa PEGylation Proteins Technology Market Forecast (USD Billion), by Rest of Middle East & Africa, 2018-2029

List of Tables

Table 1: Global PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 2: Global PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 3: Global PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 4: Global PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Region, 2018-2029

Table 5: North America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 6: North America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 7: North America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 8: North America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 9: Europe PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 10: Europe PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 11: Europe PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 12: Europe PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 13: Latin America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 14: Latin America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 15: Latin America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 16: Latin America PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 17: Asia Pacific PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 18: Asia Pacific PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 19: Asia Pacific PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 20: Asia Pacific PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Table 21: Middle East & Africa PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 1, 2018-2029

Table 22: Middle East & Africa PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 2, 2018-2029

Table 23: Middle East & Africa PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Segment 3, 2018-2029

Table 24: Middle East & Africa PEGylation Proteins Technology Market Revenue (USD Billion) Forecast, by Country, 2018-2029

Research Process

Data Library Research are conducted by industry experts who offer insight on

industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager

and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

![research-methodology1]()

Primary Research

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary Research

Secondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size Estimation

Both, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model

![research-methodology2]()