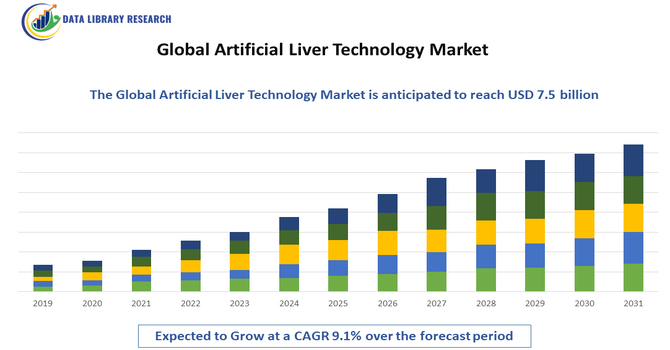

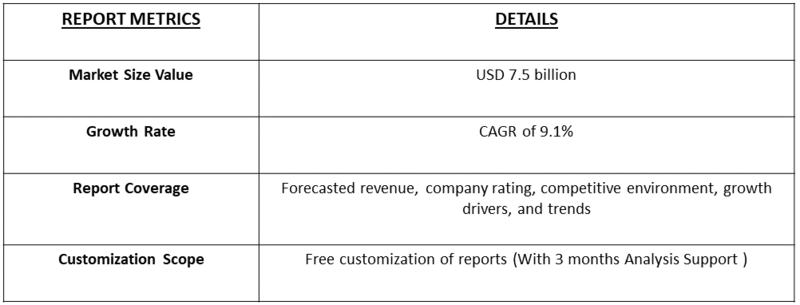

The Global Artificial Liver Technology Market size was valued at approximately $3.2 billion in 2023 and is projected to reach around $7.5 billion by 2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Artificial Liver Technology Market involves medical devices and bioengineered systems designed to support or replace liver functions in patients with liver failure. These technologies, including bioartificial liver devices, extracorporeal liver support systems, and cell-based therapies, help detoxify blood, maintain metabolic balance, and improve patient outcomes. Rising liver disease prevalence and technological advancements are driving market growth globally.

The Global Artificial Liver Technology Market is driven by the increasing prevalence of liver diseases, including hepatitis, cirrhosis, and liver failure, which have created a growing demand for effective treatment solutions. Technological advancements in bioartificial liver devices, cell-based therapies, and extracorporeal liver support systems have improved patient outcomes and expanded clinical applications. Additionally, rising healthcare awareness, government initiatives supporting organ failure treatments, and increased research and development investments have further fueled the adoption and growth of artificial liver technologies worldwide.

The Artificial Liver Technology market has witnessed significant trends, including the development of advanced bioartificial liver systems integrating hepatocyte-based therapies and biomaterials for improved liver function support. Increasing adoption of extracorporeal liver support systems in critical care settings and the integration of AI and sensor-based monitoring for real-time patient management are shaping the market. Additionally, collaborations between research institutes and biotech companies are accelerating innovation and commercialization globally.

Segmentation: The Global Artificial Liver Technology Market is segmented primarily by the Type of System (Bio-Artificial Liver (BAL) systems, and Non-Bio-Artificial Liver systems), Technology Type (Cell Based Technologies, Acellular Technologies, Bioreactor Technologies, and Regenerative Medicine Approaches), Source Type (Human Derived Sources, Animal Derived Sources, and Synthetic/Stem Cell Sources), Application (Acute Liver Failure Treatment, Chronic Liver Disease Management, Liver Transplantation Support, And Drug Metabolism & Toxicity Testing) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The most significant factor driving the market is the severe and growing worldwide shortage of compatible donor livers for transplantation. While liver failure cases are rising rapidly, primarily due to an escalating prevalence of conditions like non-alcoholic fatty liver disease (NAFLD), Hepatitis B and C, and alcohol-related liver damage, the supply of organs remains critically low. This disparity between the massive patient pool and the scarce availability of life-saving transplants creates an enormous unmet clinical need. Artificial liver support systems—both non-biological and bio-artificial—provide a critical, temporary lifeline to stabilize patients experiencing acute liver failure or acute-on-chronic failure, buying them precious time. This essential function in sustaining critically ill patients, when no other options exist, is compelling hospitals and healthcare systems globally to invest in these advanced supportive technologies.

Accelerating technological innovation, especially in Bio-Artificial Liver (BAL) systems, is a key market accelerator. Early systems focused primarily on detoxification, but newer generations are integrating living liver cells (hepatocytes) within advanced bioreactors. This allows the systems to not only filter toxins but also perform the liver's vital metabolic and synthetic functions, mimicking the human organ more closely. This enhanced functionality offers better patient outcomes, enabling the devices to serve as a reliable "bridge-to-recovery," giving the patient's native liver a chance to regenerate and avoid the need for a full transplant altogether. Continuous R&D into more efficient cell sources, improved bioreactor designs, and integrated diagnostics is consistently pushing the market forward by improving efficacy and reducing device size.

Market Restraint

The primary factor restraining the market growth is the prohibitively high cost associated with the development, manufacturing, and clinical deployment of artificial liver systems. Creating complex, functional bio-artificial systems requires expensive, specialized materials, sophisticated bioreactor technology, and extensive, highly specialized infrastructure. This results in substantial initial costs and high recurring operational expenses, limiting accessibility for many healthcare providers, especially in emerging economies. Furthermore, the technology is subject to extremely rigorous and lengthy regulatory approval processes (e.g., by the FDA and EMA) due to the use of biological components and its role as a life-support device, delaying market entry and commercial scaling.

Artificial liver technologies have positively impacted society by improving survival rates for patients with acute and chronic liver failure, reducing dependence on donor organs, and lowering healthcare costs associated with prolonged hospitalizations. These innovations enhance quality of life for patients and reduce the socioeconomic burden of liver diseases, particularly in regions with high prevalence and limited access to liver transplantation.

Artificial liver technologies have also contributed to broader socioeconomic benefits by enabling faster patient recovery and reducing the strain on intensive care units and transplant waiting lists. By offering alternative or bridging therapies, these technologies minimize long-term disability and associated productivity losses, allowing patients to return to work and normal life sooner. This, in turn, reduces the economic burden on families, healthcare systems, and national economies, particularly in regions with high liver disease prevalence.

Segmental Analysis:

The Bio-Artificial Liver (BAL) systems segment is expected to experience significant growth due to the rising prevalence of liver diseases, including acute and chronic liver failure. BAL systems combine biological components, such as hepatocytes, with mechanical devices to perform key liver functions, bridging patients to recovery or transplantation. Technological advancements in cell viability, scaffold materials, and biocompatible membranes have improved efficacy and patient outcomes. Increasing awareness among clinicians and patients, along with supportive regulatory frameworks and ongoing clinical trials demonstrating safety and effectiveness, are further driving adoption of BAL systems globally, positioning this segment as a crucial component in the artificial liver technology market.

The bioreactor technologies segment is projected to witness substantial growth due to their critical role in maintaining functional hepatocytes for artificial liver applications. Bioreactors provide controlled environments for cell culture, ensuring optimal oxygenation, nutrient supply, and waste removal, which are essential for sustaining liver-specific functions. Advancements in microfluidics, 3D scaffolding, and sensor integration have enhanced performance and reproducibility. Rising investments in research and development, growing demand for organ support devices, and increasing clinical applications in drug testing and transplantation support have further fueled market growth. The versatility of bioreactor systems across pharmaceutical, clinical, and research settings continues to drive their adoption globally.

The Synthetic/Stem-Cell Sources Segment is poised for significant growth during the forecast period due to its immense potential to create Bio-Artificial Liver (BAL) systems that truly mimic human liver functionality. Unlike systems relying on animal cells or simple mechanical filters, this segment leverages induced pluripotent stem cells (iPSCs) or other engineered cellular lines. These cells can be cultivated and differentiated into functional hepatocytes in vitro, offering a reproducible, scalable, and ethically sound cell source for BAL devices. This capability overcomes the traditional limitations of donor scarcity and immune rejection risks associated with using primary cells. As research successfully addresses challenges related to cell viability and functional maturity within bioreactors, the market will rapidly shift toward these advanced, synthetic cellular components to provide more effective and durable liver support solutions.

The chronic liver disease management segment is expected to experience notable growth owing to the increasing global burden of liver disorders such as cirrhosis, hepatitis, and non-alcoholic fatty liver disease. Artificial liver technologies, including BAL systems and extracorporeal liver support devices, provide critical therapeutic support for patients awaiting transplantation or ineligible for surgery. Growing awareness among healthcare providers about early intervention strategies and improved clinical outcomes has accelerated adoption. Additionally, the rise in healthcare expenditure, availability of advanced liver monitoring tools, and ongoing government initiatives to address liver disease management contribute to the expansion of this market segment worldwide.

The North American artificial liver technology market is expected to witness significant growth due to the high prevalence of liver diseases, advanced healthcare infrastructure, and strong adoption of innovative medical technologies. The presence of leading market players, substantial investments in research and development, and supportive regulatory frameworks have facilitated rapid commercialization of artificial liver devices. For instance, in June 2025, United Therapeutics Corporation and Intermountain Health conducted the world’s first clinical trial using miroliverELAP, a bioengineered external liver assist device, on a liver failure patient ineligible for transplantation. Developed by Miromatrix Medical Inc., the system used a decellularized porcine liver scaffold infused with human cells. This milestone demonstrated significant progress in organ bioengineering, enhancing North America’s leadership and innovation in the bioartificial liver therapeutic technology market.

Additionally, growing awareness about liver health, increasing liver transplantation rates, and the rising geriatric population have fueled demand for artificial liver systems. Collaborations between biotech firms, research institutes, and hospitals continue to advance technology development, making North America a dominant region in the global artificial liver technology market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the artificial liver technology market is characterized by strategic collaborations, mergers, and acquisitions among key players to expand product portfolios and global reach. Companies focus on innovation, regulatory approvals, and partnerships with hospitals and research institutes to strengthen market positioning. Leading players compete on technological advancements, product efficacy, and clinical support services, driving rapid market growth and adoption worldwide.

The major players for the above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The most significant driver is the alarming shortage of healthy donor livers available for transplantation, even as the global rate of acute and chronic liver failure continues to climb. Conditions like Hepatitis, non-alcoholic fatty liver disease (NAFLD), and alcohol-induced cirrhosis are increasing, creating a large patient pool in urgent need of temporary life support. Artificial liver technologies offer a crucial bridge-to-transplant solution, stabilizing patients until an organ becomes available, or even allowing the native liver time to recover, which is a massive demand driver.

Q2. What are the main restraining factors for this market?

The major hurdle is the extremely high cost associated with developing and manufacturing these complex systems, particularly Bio-Artificial Liver (BAL) devices. The technology itself is complex, demanding specialized infrastructure and highly trained personnel for operation. Additionally, the need for stringent regulatory approvals from bodies like the FDA, combined with the difficulty of conducting large-scale, definitive clinical trials for these life-saving, specialized devices, significantly slows down market entry and widespread adoption.

Q3. Which segment is expected to witness high growth?

The Bio-Artificial Liver (BAL) Systems segment is anticipated to witness the highest growth. Unlike purely mechanical detoxification systems, BAL systems incorporate living hepatocytes (liver cells), often derived from stem cells. This allows them to mimic the liver's crucial metabolic and synthetic functions, not just its clearance functions. Ongoing advancements in cell encapsulation and bioreactor design are rapidly improving the efficacy and lifespan of these functional models, attracting heavy research and commercial investment as the ultimate, most comprehensive solution.

Q4. Who are the top major players for this market?

The market is highly competitive and includes a mix of major medical device manufacturers and highly specialized biotech startups collaborating with academic research centers. Key commercial players include companies that specialize in blood purification and adsorption technologies, such as Asahi Kasei Medical Co., Ltd. (with its related products) and firms focused on liver dialysis like Baxter International Inc. through certain devices. Innovation is also heavily driven by institutions like Y-mAbs Therapeutics and numerous universities pioneering next-generation bio-artificial liver technology.

Q5. Which country is the largest player?

The United States is the largest market for artificial liver technology. This dominance is due to a very high prevalence of end-stage liver disease, a substantial healthcare budget, and a robust environment for biotech research and development. The country benefits from extensive funding from organizations like the National Institutes of Health (NIH) and a strong venture capital ecosystem that rapidly supports the commercialization and clinical testing of cutting-edge liver support systems and bio-artificial liver devices.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model