Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Self Collimator Market refers to the worldwide industry focused on the production, distribution, and sales of self-collimators—precision optical instruments used to measure alignment, angular displacement, and straightness in industrial and metrology applications. This market grows with demand from automotive, aerospace, electronics, and manufacturing sectors where accurate optical measurement is critical. The key drivers include rising quality standards, automation, and technological advancements in optical sensing.

The global self collimator market is evolving with strong growth driven by automation integration and technological innovation. Manufacturers increasingly embed self collimators into automated systems for improved precision and efficiency, while smart models with advanced sensors and data analytics are gaining traction. The key end-use sectors such as aerospace, automotive, medical technology, and manufacturing are pushing demand for high-precision alignment and calibration tools.

Segmentation: The Global Self Collimator Market is segmented by Type (Optical Self Collimators and Electronic Self Collimators), Technology (Manual, Semi-Automatic, and Fully Automatic Systems), Application (Angular Measurement, Straightness Measurement, Flatness Testing, Alignment, and Calibration), End-Use Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, Industrial Manufacturing, Optical & Metrology Labs, and Research Institutions), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing need for high-precision measurement and alignment across industries is a major driver of the global self-collimator market. Sectors such as aerospace, automotive, semiconductor manufacturing, and defense require extremely accurate angular and straightness measurements to meet strict quality and safety standards. Self-collimators enable non-contact, high-resolution measurements that reduce errors during production and assembly. As product tolerances become tighter and components more complex, manufacturers increasingly rely on advanced metrology tools. This demand is further amplified by regulatory compliance requirements and the global emphasis on improving manufacturing accuracy and reliability.

The rapid adoption of automation and Industry 4.0 practices is significantly driving the self collimator market. Modern manufacturing environments increasingly integrate digital and automated inspection systems to improve efficiency and reduce human intervention.

Electronic self-collimators with digital outputs, software integration, and real-time monitoring capabilities are well suited for smart factories. For instance, in 2024, Optikos released the ColliMeter measurement system, enabling precise setup and qualification of collimators. The system enhanced automation and smart manufacturing by improving accuracy, reducing manual intervention, and streamlining calibration processes. Its introduction strengthened the global self collimator market by supporting efficient, high-precision production and quality control in advanced industrial and manufacturing applications.

These systems support faster calibration, predictive maintenance, and data-driven decision-making. As manufacturers invest in automated production lines and quality control systems, the demand for precise, reliable, and automation-compatible alignment tools continues to rise, supporting sustained market growth globally.

Market Restraints:

High initial costs and technical complexity act as key restraints on the global self collimator market. Advanced electronic and automated self collimators require significant capital investment, making them less accessible for small and medium-sized enterprises. In addition, operation and maintenance often require skilled personnel, specialized training, and calibration expertise, increasing overall ownership costs. Limited awareness and lack of technical infrastructure in developing regions further restrict adoption. These factors can delay purchasing decisions and encourage users to opt for lower-cost conventional measurement tools, thereby slowing market penetration, especially in price-sensitive markets.

The self collimator market contributes to socioeconomic development by enhancing industrial productivity and quality control across critical sectors like aerospace, defense, automotive, and healthcare. Precision measurement tools help minimize manufacturing errors, reducing waste and improving product safety and reliability. Adoption of advanced self collimation technology supports workforce upskilling, as operators require specialized training, creating higher-skill jobs. Increased use in infrastructure and R&D promotes technological competitiveness and supports export-oriented industrial growth. Expanding markets in emerging economies also attract foreign investment and stimulate local supplier ecosystems. Thus, the market drives efficiency, technological advancement, and economic growth within precision-engineering industries.

Segmental Analysis:

The optical self collimators segment is expected to witness the highest growth over the forecast period due to its wide adoption in precision alignment and calibration applications. These instruments offer high accuracy, non-contact measurement, and reliability, making them ideal for metrology labs, aerospace assembly, and optical component testing. Optical self collimators are preferred for their robustness, long operational life, and suitability in environments where electronic interference must be minimized. Growing demand for ultra-precise optical systems, lenses, and mirrors, along with increased quality control requirements in advanced manufacturing, is further accelerating the growth of this segment globally.

The fully automatic systems segment is expected to witness the highest growth over the forecast period, driven by increasing automation across manufacturing industries. Fully automatic self collimators reduce manual intervention, improve measurement consistency, and enable faster inspection cycles. These systems integrate seamlessly with smart factories, digital quality control platforms, and Industry 4.0 frameworks. Real-time data processing, remote monitoring, and software-based analysis enhance productivity and reduce operational errors. As manufacturers prioritize efficiency, repeatability, and reduced downtime, investment in fully automatic alignment and measurement systems continues to rise, making this segment a key growth contributor to the global market.

The angular measurement segment is expected to witness the highest growth over the forecast period due to its critical role in precision engineering and alignment processes. Self collimators are extensively used for angular deviation measurement in machine tools, optical assemblies, and mechanical components. Increasing complexity of modern machinery and tighter tolerance requirements are driving demand for accurate angular measurement solutions. Industries such as aerospace, automotive, and semiconductor manufacturing rely heavily on precise angular alignment to ensure performance and safety. The ability of self collimators to deliver high-resolution, non-contact angular measurements positions this segment for strong and sustained growth.

The electronics and semiconductor segment is expected to witness the highest growth over the forecast period, supported by rapid advancements in microelectronics and chip manufacturing. Semiconductor fabrication requires extremely precise alignment and calibration to maintain product quality and yield. Self collimators play a vital role in lithography equipment alignment, optical inspection, and precision assembly processes. The growing demand for consumer electronics, electric vehicles, 5G infrastructure, and advanced computing technologies is driving increased semiconductor production worldwide. As fabs invest heavily in advanced metrology tools to meet shrinking node sizes, demand for high-precision self collimators continues to expand.

Europe is expected to witness the highest growth in the global self collimator market over the forecast period, driven by its strong industrial and technological base. The region is home to leading aerospace, automotive, optical, and precision engineering industries that require advanced alignment and measurement solutions.

Increased investment in automation, research and development, and high-end manufacturing supports market expansion. For instance, in 2024, Thorlabs and Infleqtion collaborated to commercialize an optical fiber collimator for quantum applications, originally developed under the UK-funded QT Assemble project. The solution provided high-performance, linearly polarized beams with integrated power monitoring, simplifying design and improving reliability. Its introduction strengthened Europe’s self collimator market by advancing precision optics for emerging quantum technologies, enhancing commercial readiness, and supporting wider adoption across high-tech industries.

Furthermore, the strict quality standards and regulatory compliance further encourage the adoption of advanced metrology tools. Additionally, the presence of key market players and growing focus on smart manufacturing and innovation position Europe as a major growth hub.

| Report Matrics | Details |

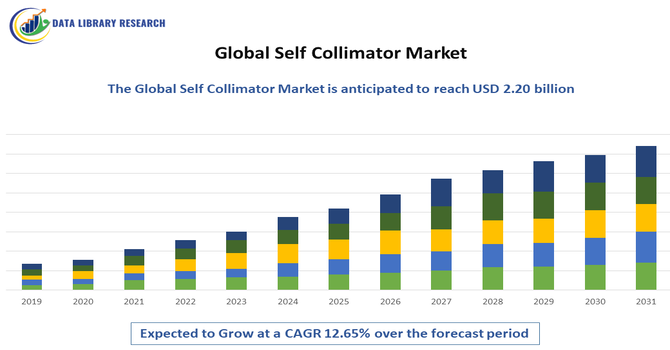

| Market Size Value | USD 0.54 billion |

| Growth Rate | CAGR of 12.65 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the global self collimator market is characterized by established optical and metrology instrument manufacturers offering diverse product portfolios. Key players focus on innovation, accuracy, and integration with digital systems to differentiate their offerings. Major companies include Siemens, KLA, Photonics Industrial, Thorlabs, IPG Photonics, LightPath Technologies, HGH Systèmes Infrarouges, TAYLOR HOBSON, Nikon Metrology, and TRIOPTICS, among others. Competition is centered on enhancing precision, expanding into emerging regional markets, and adopting automation-friendly features.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the rising demand for high-precision optical alignment in semiconductor manufacturing and aerospace engineering. As components shrink, the need for sub-arcsecond angular measurements grows. Additionally, the expansion of the automotive industry’s LIDAR systems and advanced driver-assistance technologies requires the extreme accuracy that modern electronic autocollimators provide.

Q2. What are the main restraining factors for this market?

The high cost of advanced electronic self-collimators remains a significant barrier for smaller laboratories and manufacturers. Furthermore, these instruments are highly sensitive to environmental vibrations and thermal fluctuations, requiring controlled settings for accurate results. The complexity of operation and the need for highly skilled technicians also limit broader market penetration.

Q3. Which segment is expected to witness high growth?

The Electronic/Digital Autocollimators segment is projected to experience the highest growth. Unlike visual models, electronic versions offer automated data collection, higher resolution, and integration with industrial software. This makes them ideal for high-speed production environments where real-time monitoring of machine tool alignment and angular stability is critical for quality.

Q4. Who are the top major players for this market?

The market is dominated by precision instrumentation specialists including Taylor Hobson (AMETEK), Nikon Metrology, and Möller-Wedel Optical. Other prominent contributors include Keisoku Giken, Davidson Optronics, Trioptics GmbH, and Thorlabs. These companies maintain leadership through specialized optical engineering and the development of dual-axis measurement systems for industrial use.

Q5. Which country is the largest player?

Germany stands as the largest player and hub for the self-collimator market. Its dominance is rooted in a world-class precision optics cluster and a robust high-end manufacturing sector. German companies lead in exporting high-accuracy metrology tools, supported by the country's stringent industrial standards and leadership in Industry 4.0 integration.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model