Get Complete Analysis Of The Report - Download Updated Free Sample PDF

This growth is propelled by the rising incidence of stomach cancer, which is influenced by factors such as dietary habits, Helicobacter pylori infections, smoking, and alcohol consumption. Advancements in drug development, increased investment in research and development (R&D), and the growing popularity of personalized medicine are further fueling market expansion. The Asia-Pacific region, particularly countries like China and Japan, holds a significant share of the market due to the high incidence rates of gastric cancer and the presence of key pharmaceutical players. The market is characterized by the development of innovative therapies, including targeted treatments and immunotherapies, which are enhancing the efficacy and specificity of gastric cancer treatments.

Recent market trends in gastric cancer treatment highlight significant advancements across multiple fronts. The integration of immunotherapy with traditional chemotherapy has become standard practice, especially for both HER2-positive and HER2-negative gastric cancers, leading to improved overall survival rates. Targeted therapies focusing on biomarkers like CLDN18.2 are gaining momentum, offering more precise attacks on cancer cells while sparing healthy tissue. Antibody-drug conjugates (ADCs) are showing promise by delivering potent cytotoxic agents directly to cancer cells, potentially enhancing efficacy and reducing side effects. Personalized medicine is advancing through next-generation sequencing, enabling tailored treatment plans based on individual genetic profiles. Additionally, CAR T-cell therapy, previously successful in blood cancers, is being explored for solid tumors such as gastric cancer, with early trials indicating extended survival benefits.

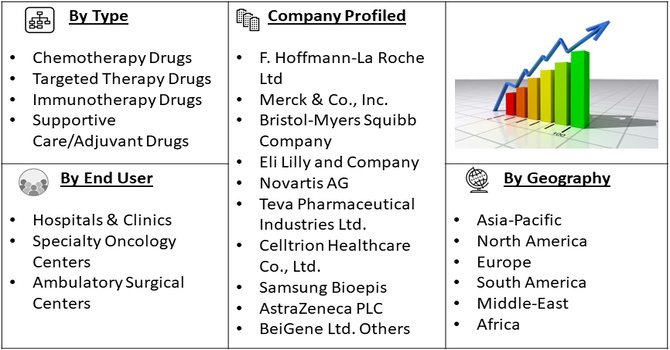

Segmentation: Global Stomach Cancer Drug Therapy Market is segmented by Drug Type (Chemotherapy Drugs, Targeted Therapy Drugs, Immunotherapy Drugs, and Supportive Care/Adjuvant Drugs), Therapy Type (Monotherapy, and Combination Therapy), End-User (Hospitals & Clinics, Specialty Oncology Centers, and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing incidence of gastric cancer worldwide is a primary driver for the market. Factors such as Helicobacter pylori infections, unhealthy dietary habits, smoking, alcohol consumption, and genetic predisposition contribute to the growing number of diagnosed cases.

In July 2025, Dana-Farber Cancer Institute experts reported a sharp rise in early-onset gastrointestinal cancers, with the youngest age groups experiencing the steepest increases. Between 2010 and 2019, new early-onset GI cancer cases rose by 14.8%, disproportionately affecting Black, Hispanic, Indigenous populations, and women. Individuals born in 1990 were found to be twice as likely to develop colon cancer and four times as likely to develop rectal cancer compared to those born in 1950. CDC data also showed colorectal cancer incidence more than tripled in ages 15–19 and nearly doubled in ages 20–24.

Similarly, in July 2025, WHO reported an estimated 15.6 million gastric cancer cases are projected to occur within current birth cohorts if existing control measures remain unchanged, with 76% potentially preventable due to their link to H. pylori infection. Asia is expected to account for two-thirds of these cases, followed by the Americas and Africa. While 58% of future cases are anticipated in traditionally high-incidence regions, 42% are projected in lower-incidence areas, driven by population growth and aging. Sub-Saharan Africa, in particular, is expected to see a dramatic rise, with future cases reaching up to six times the 2022 levels. This rising prevalence has led to an increased demand for effective drug therapies, including chemotherapy, targeted therapy, and immunotherapy, to improve patient outcomes and survival rates.

Continuous innovations in drug development, particularly in targeted therapies and immunotherapies, are fueling market growth. Targeted therapies allow for selective action against cancer cells with minimal damage to healthy tissues, while immunotherapies enhance the body’s immune response to fight tumors.

In JUly 2025, AstraZeneca’s supplemental Biologics License Application (sBLA) for Imfinzi was accepted and granted Priority Review by the FDA for treating resectable, early-stage to locally advanced gastric and GEJ cancers. The FDA granted Priority Review based on the potential for significant improvements over existing therapies. The regulatory decision was expected by the fourth quarter of 2025 under the Prescription Drug User Fee Act (PDUFA). The Priority Review for Imfinzi signaled strong regulatory momentum and could accelerate its entry into the stomach cancer drug therapy market. If approved, it may strengthen the role of immunotherapy in early-stage and locally advanced gastric and GEJ cancer treatment, expanding options beyond standard chemotherapy. These advancements have improved treatment efficacy, reduced side effects, and expanded therapeutic options, driving adoption among healthcare providers and patients globally.

Market Restraints:

High costs associated with advanced therapies, such as targeted treatments and immunotherapies, limit accessibility, particularly in low- and middle-income countries. Additionally, many drug therapies, especially chemotherapy, are linked with severe side effects like nausea, fatigue, and immunosuppression, which can reduce patient compliance and treatment effectiveness. Limited awareness about stomach cancer symptoms and insufficient screening programs in certain regions often result in late-stage diagnoses, further constraining market expansion. Moreover, stringent regulatory requirements and long approval timelines for new therapies slow down the introduction of innovative drugs, increasing development costs and delaying commercialization. These factors collectively act as significant challenges to the market’s growth.

The Stomach Cancer Drug Therapy market is fundamentally a humanitarian market with profound socio-economic consequences. Economically, the market involves massive R&D investment by pharmaceutical firms, supporting high-skill jobs and driving advancements in precision medicine, particularly in immunotherapy. Socially, the availability of innovative and effective therapies, especially in early detection and advanced stages, directly increases patient survival rates and quality of life. The challenge remains equitable access; high drug costs and uneven biomarker testing availability, particularly in developing nations, create significant health and economic inequity, underscoring the urgent need for inclusive global healthcare policies.

Segmental Analysis:

The targeted therapy drugs segment is expected to witness the highest growth in the drug type category. These therapies are designed to selectively target cancer-specific biomarkers, such as HER2 and CLDN18.2, allowing precise attack on tumor cells while minimizing damage to healthy tissue. The adoption of targeted therapies is increasing due to their improved efficacy, reduced side effects compared to conventional chemotherapy, and ability to be combined with other treatments like immunotherapy for enhanced outcomes.

Continuous R&D and clinical trials are expanding the indications and applications for these drugs, driving strong market demand. For instance, in 2023, An international Phase 3 trial with Weill Cornell Medicine found that zolbetuximab plus chemotherapy improved survival in advanced gastric or GEJ cancer patients overexpressing a specific biomarker. Published results from the GLOW and SPOTLIGHT studies led the FDA to grant priority review, targeting a decision by January 12, 2024. If approved, zolbetuximab would be the first targeted therapy in the U.S. for HER2-negative, CLDN 18.2-positive advanced gastric or GEJ cancer. The success of zolbetuximab could significantly expand the targeted therapy segment in gastric and GEJ cancer treatment. It introduces a novel option for HER2-negative, CLDN 18.2-positive patients, potentially reshaping treatment standards.

The combination therapy segment is gaining traction as it involves the use of multiple drugs, such as chemotherapy combined with targeted therapy or immunotherapy, to achieve better clinical outcomes. This approach is particularly effective in advanced-stage stomach cancer, where single-drug therapies may not be sufficient.

Combination therapies improve survival rates, reduce the risk of drug resistance, and provide personalized treatment options, making them a preferred choice among oncologists and healthcare providers. For instance, in 2021, the Food and Drug Administration approved nivolumab (Opdivo, Bristol-Myers Squibb Company) in combination with fluoropyrimidine- and platinum-containing chemotherapy for the treatment of advanced or metastatic gastric cancer, gastroesophageal junction cancer, and esophageal adenocarcinoma.

Specialty oncology centers are a key end-user segment, as they focus exclusively on cancer diagnosis and treatment, offering advanced therapies and personalized treatment plans. These centers are equipped with specialized infrastructure, trained personnel, and access to cutting-edge drugs, including targeted therapies and immunotherapies. The increasing number of specialty oncology centers globally is driving market growth, as they serve as hubs for adopting innovative treatment modalities and managing complex gastric cancer cases.

The North America region is projected to witness the highest growth in the Global Stomach Cancer Drug Therapy Market over the forecast period. In 2024, Canada was projected to see approximately 4,000 new stomach cancer cases, with an age-adjusted incidence rate of 5.07 per 100,000 people annually between 1992 and 2010. This growth is primarily driven by high number of stomach cancer cases in the region.

The region benefits from strong investments in research and development, the availability of targeted therapies and immunotherapies, and a well-established network of specialty oncology centers and hospitals. For instance, in 2025, Positive topline results from the DESTINY-Gastric04 Phase 3 trial demonstrated that ENHERTU (trastuzumab deruxtecan) significantly improved overall survival compared to ramucirumab and paclitaxel in second-line HER2-positive metastatic gastric or GEJ adenocarcinoma. The trial was unblinded early due to ENHERTU’s superior efficacy. These results confirmed the drug’s effectiveness in this patient population. The findings were shared with global regulatory authorities. The positive results from the DESTINY-Gastric04 trial strengthened ENHERTU’s position as a leading second-line treatment for HER2-positive metastatic stomach cancer in the US. This is expected to enhance treatment options and improve survival outcomes for patients, potentially reshaping the competitive landscape in the stomach cancer drug therapy market.

Additionally, rising government initiatives, insurance coverage for advanced treatments, and a high prevalence of gastric cancer in specific demographics contribute to the increasing demand for effective drug therapies in North America, making it a leading market globally.

| Report Matrics | Details |

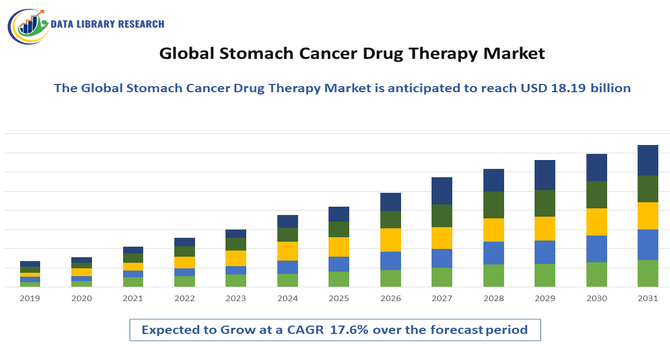

| Market Size Value | USD 18.19 billion |

| Growth Rate | CAGR of 17.6% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global stomach cancer drug therapy market is characterized by a competitive landscape comprising both established pharmaceutical giants and emerging biotech firms. These companies are engaged in the development, production, and commercialization of various therapies, including chemotherapy, targeted therapies, and immunotherapies, to address the growing prevalence of gastric cancer worldwide.

Key Players Global Stomach Cancer Drug Therapy Market:

Recent Development

Q1. What the main growth driving factors for this market?

The market is primarily driven by the rising global incidence and prevalence of stomach (gastric) cancer, fueled by factors like the increasing geriatric population, changes in lifestyle (such as smoking and unhealthy dietary habits), and the rise in obesity. Significant advancements in oncology research, particularly the development and acceptance of novel targeted therapies and immunotherapies like PD-1/PD-L1 inhibitors, are also key drivers. Furthermore, a robust pipeline of drugs and a growing focus on personalized medicine contribute substantially to market expansion.

Q2. What are the main restraining factors for this market?

Major restraining factors include the high cost associated with advanced cancer drug therapies, which can be a financial burden for patients, especially in regions with inadequate reimbursement policies. Additionally, the limited number of treatment options currently available for certain types and stages of gastric cancer, combined with the associated severe side effects of conventional treatments like chemotherapy, acts as a barrier to market growth. Stringent regulatory processes for new drug approvals and potential supply chain disruptions can also slow down market progress.

Q3. Which segment is expected to witness high growth?

The Immunotherapy segment is expected to witness the fastest growth rate, largely due to its innovative mechanism of action, which involves harnessing the body's own immune system to target and destroy cancer cells. Within drug classes, PD-1/PD-L1 inhibitors are projected for rapid expansion, driven by increasing regulatory approvals and growing adoption in treatment regimens for advanced stomach cancer. Furthermore, the oral route of administration is also anticipated to grow significantly due to its convenience and potential for at-home treatment.

Q4. Who are the top major players for this market?

The global stomach cancer drug therapy market is dominated by major multinational pharmaceutical and biotechnology companies with strong oncology portfolios. Key players include F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Bristol-Myers Squibb Company (BMS), Eli Lilly and Company, and Pfizer Inc. Other significant contributors known for innovative therapies and pipeline candidates include AstraZeneca PLC and Daiichi Sankyo Company, Limited, with an increasing focus on targeted therapies and immunotherapies.

Q5. Which country is the largest player?

North America, particularly the United States, is often cited as the largest market, driven by its well-established healthcare infrastructure, high adoption of advanced and high-cost novel therapies, and significant investments in pharmaceutical research and development.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model