Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Telehealth Franchise Market refers to the industry segment where telehealth services—such as virtual consultations, remote patient monitoring, and digital healthcare solutions—are offered through franchised business models. Franchises enable healthcare providers, entrepreneurs, and investors to operate under an established brand, leveraging standardized technology platforms, training, and operational support. The market growth is driven by rising healthcare digitization, increasing patient demand for convenient access to medical services, and a shortage of healthcare professionals in certain regions.

The global telehealth franchise market is witnessing rapid growth due to increasing adoption of digital healthcare solutions and virtual consultations. Key trends include integration of AI and IoT in patient monitoring, expansion of mobile health apps, and the use of cloud-based platforms for secure data sharing. Franchises are focusing on offering specialized services such as mental health, chronic disease management, and elderly care. Rising consumer preference for convenient, accessible, and cost-effective healthcare is driving innovation and franchise expansion worldwide.

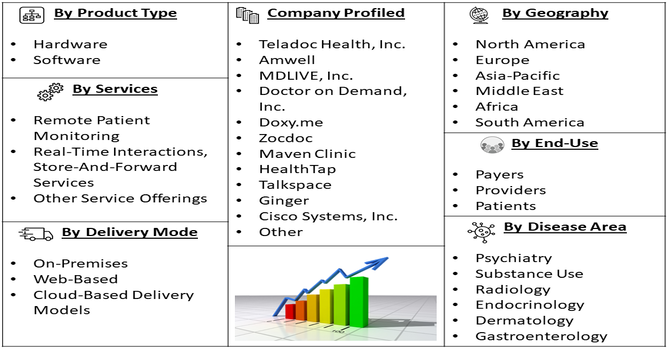

Segmentation: The Global Telehealth Franchise Market is Segmented by Product Outlook (Hardware (Monitors, Medical Peripheral Devices, Blood Pressure Meters, Blood Glucose Meters, Weighing Scales, Pulse Oximeters, Peak Flow Meters, ECG Monitors, and Other Devices), Software (Standalone Software and Integrated Software Solutions), and Services (Remote Patient Monitoring, Real-Time Interactions, Store-And-Forward Services, and Other Service Offerings), Delivery Mode (On-Premises, Web-Based, and Cloud-Based Delivery Models), Disease Area (Psychiatry, Substance Use, Radiology, Endocrinology, Dermatology, Gastroenterology, Mental Health and Counseling, Neurological Medicine, ENT, Cardiology, Oncology, Dental, Gynecology, General Medicine, and Other Disease Areas), End-Use Outlook (Payers, Providers, and Patients), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary driver for this market is the shifting consumer demand toward immediate, on-demand medical access that eliminates the traditional barriers of travel and waiting rooms. As digital literacy increases across all age groups, patients are seeking "home-first" care models that offer the same quality of consultation as in-person visits but with significantly higher convenience. This behavioral change is supported by the rapid expansion of 5G infrastructure and high-speed internet, which ensures that high-definition video consultations are seamless. Consequently, this technological reliability builds trust between patients and providers, encouraging long-term adoption of virtual care platforms globally.

Another significant driver is the increasing institutional support and financial viability of the telehealth business model for local entrepreneurs. Insurance providers are progressively expanding their reimbursement policies to cover virtual visits at the same rates as physical ones, removing the financial risk that previously hindered market growth.

In May 2024, Apollo Telehealth, in partnership with the Government of Manipur, launched a telemedicine-enabled primary health center (PHC) in Borobeka. The initiative leveraged telemedicine technology to improve primary healthcare access for the local community. For potential business owners, the franchise model provides a sophisticated "business-in-a-box" solution, offering specialized HIPAA-compliant software, established medical protocols, and recognized branding. This lowering of the entry barrier allows non-medical entrepreneurs to enter the healthcare space efficiently, fueling a surge in new telehealth clinics that can scale rapidly across different geographic regions.

Market Restraints:

The most significant restraint is the fragmented and highly complex landscape of international and regional medical regulations. Telehealth franchises must navigate a labyrinth of licensing laws, where practitioners are often required to be licensed in the exact location where the patient is physically situated during the call. These "practice of medicine" laws vary wildly between different states and countries, making it extremely difficult for a franchise to maintain a standardized operating model across borders. This regulatory friction not only increases legal and compliance costs but also slows down the speed at which a franchise can expand into new territories.

Telehealth franchises are transforming healthcare accessibility, particularly in underserved or remote areas, by bridging the gap between patients and medical professionals. They reduce travel costs, save time, and enhance continuity of care. Economically, these franchises create employment opportunities, stimulate technology adoption, and support small business ownership under established brands. By lowering healthcare costs and improving efficiency, they contribute to better population health outcomes. Increased adoption also supports public health initiatives and reduces strain on traditional healthcare infrastructure.

Segmental Analysis:

The blood pressure meters segment is projected to witness the highest growth over the forecast period due to increasing prevalence of hypertension and cardiovascular disorders globally. Rising awareness about early diagnosis, self-monitoring trends among patients, and the growing adoption of home healthcare devices are driving demand. Technological advancements such as wireless connectivity, integration with mobile applications, and improved accuracy further enhance the appeal of these devices. Moreover, supportive government initiatives and preventive healthcare programs aimed at monitoring blood pressure regularly are contributing to revenue growth. The segment’s expansion is expected across both developed and emerging markets.

The cloud-based delivery models segment is expected to experience the highest growth over the forecast period as healthcare organizations increasingly adopt cloud solutions for data storage, remote monitoring, and interoperability. Cloud platforms offer scalable, cost-effective, and secure solutions compared to traditional on-premises systems, enabling real-time access to patient data and analytics. The growing need for telehealth services, integration with wearable devices, and regulatory support for cloud adoption are accelerating growth. Additionally, the flexibility to update software, reduce infrastructure costs, and support large-scale remote operations makes cloud-based delivery models increasingly attractive to providers, payers, and patients worldwide.

The mental health and counseling segment is expected to witness the highest growth during the forecast period, driven by rising awareness of mental health issues and increasing demand for accessible care solutions. The COVID-19 pandemic has further emphasized the importance of mental wellness, encouraging adoption of tele-counseling and remote therapy platforms. Technological advancements, including mobile-based therapy apps, AI-assisted mental health monitoring, and virtual consultations, have facilitated easier patient engagement. Additionally, government initiatives, employer-supported wellness programs, and growing insurance coverage for mental health services are boosting adoption. The increasing prevalence of psychiatric disorders and substance use disorders globally supports strong long-term revenue growth in this segment.

The payers segment is projected to witness the highest growth over the forecast period due to increasing demand for cost-effective healthcare management solutions. Payers, including insurance companies and health maintenance organizations, are adopting remote monitoring, cloud-based systems, and integrated healthcare platforms to enhance efficiency and reduce operational costs. Rising emphasis on value-based care, predictive analytics, and patient-centric models is further driving adoption. Additionally, partnerships with digital health providers and increased coverage for telehealth services are expanding opportunities in this segment. The growing need to manage chronic diseases, control healthcare expenditures, and improve patient outcomes is expected to sustain robust growth in the payers segment.

North America is expected to witness the highest growth over the forecast period due to the presence of advanced healthcare infrastructure, high adoption of digital health technologies, and supportive government initiatives. The region benefits from widespread use of remote patient monitoring, telehealth services, and cloud-based platforms. For instance, in August 2023, Spark Biomedical launched telehealth services for Sparrow Ascent, enhancing access to opioid withdrawal treatment across North America. This initiative strengthened the region’s telehealth capabilities, expanded medication-assisted treatment (MAT) reach, and contributed to growth in the North American segment of the global telehealth franchise market.

Increasing prevalence of chronic diseases, rising demand for home healthcare devices, and growing awareness of preventive healthcare practices contribute to market expansion. Additionally, strong reimbursement frameworks, innovative product launches, and significant investment in research and development enhance growth prospects. North America’s favorable regulatory environment and technologically advanced medical ecosystem are key drivers of sustained revenue growth.

| Report Matrics | Details |

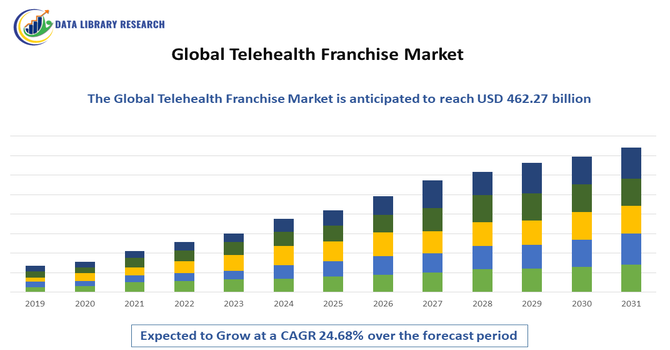

| Market Size Value | USD 462.27 billion |

| Growth Rate | CAGR of 24.68 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global telehealth franchise market is highly competitive, with key players leveraging brand recognition, technology platforms, and service quality to expand their presence. Major franchises focus on strategic partnerships, acquisitions, and geographic expansion to capture market share. Differentiation is achieved through specialized telehealth services, proprietary software, and comprehensive training for franchisees. New entrants are adopting innovative models, including subscription-based services and AI-driven care solutions, intensifying competition. Consolidation and technological advancement are expected to shape the market landscape in the coming years.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is growing because patients want convenient, on-demand medical care without leaving their homes. For entrepreneurs, the franchise model offers a proven business structure and brand recognition in a complex medical field. Additionally, improvements in 5G technology and the increasing acceptance of digital prescriptions by insurance companies make remote clinics more profitable.

Q2. What are the main restraining factors for this market?

Growth is limited by complex and varying medical regulations across different states and countries. Ensuring consistent quality of care across many different franchise locations can also be difficult. Furthermore, high initial franchise fees and the ongoing costs of maintaining secure, HIPAA-compliant software can be a barrier for new business owners.

Q3. Which segment is expected to witness high growth?

The Mental Health and Counseling segment is expected to see the highest growth. There is a massive global demand for therapy services that can be accessed privately and comfortably from home. Because behavioral health often requires regular talking sessions rather than physical exams, it is perfectly suited for a scalable franchise model.

Q4. Who are the top major players for this market?

The market is led by companies that combine medical expertise with scalable business platforms. Key players include Doctor on Demand, Teladoc Health, BetterHelp, and specialized franchise brands like The Joint Chiropractic (expanding into digital) or MD-Now. These organizations provide the technology and legal frameworks that individual franchisees need to operate safely.

Q5. Which country is the largest player?

The United States is the largest player in the telehealth franchise market. This is due to its large, private-sector healthcare system and a strong culture of franchising. The U.S. has a high demand for efficient healthcare alternatives and a legal environment that increasingly supports the reimbursement of virtual visits by both government and private insurance.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model