Get Complete Analysis Of The Report - Download Updated Free Sample PDF

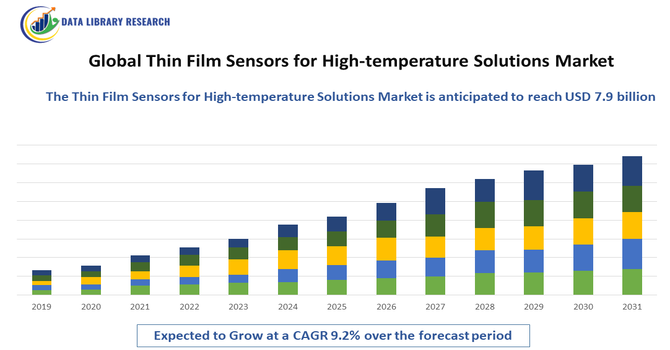

The growth of the Global Thin-Film Sensors for High-Temperature Market is primarily driven by rising demand for reliable and precise sensing solutions in extreme industrial environments such as aerospace engines, gas turbines, metal processing plants, and advanced power systems. Increasing adoption of high-efficiency industrial furnaces, expanding aerospace and defense programs, and stringent safety and performance standards across oil & gas, chemical processing, and energy sectors are accelerating market expansion. Additionally, advancements in thin-film coating technologies, micro-fabrication techniques, and high-temperature-resistant materials are enabling improved durability and accuracy, boosting adoption. The growing shift toward smart manufacturing, predictive maintenance, and Industry 4.0 also supports demand, as industries increasingly integrate high-temperature sensors for real-time monitoring, operational optimization, and early failure detection.

The Global Thin Film Sensors for High-Temperature Market is witnessing a surge in innovation as industries demand highly durable, precise, and compact sensing solutions for extreme operating environments. A key trend is the rapid development of advanced thin-film materials and substrates—such as platinum, metal-oxide coatings, and silicon carbide—that enable sensors to withstand temperatures exceeding 800°C to 1,000°C while maintaining stability and accuracy. Flexible and conformal thin-film sensor designs are also gaining traction, enabling direct integration on curved engine components, turbine blades, and industrial furnace surfaces, supporting next-generation aerospace, power generation, and high-temperature semiconductor equipment. Additionally, miniaturization and integration with IoT and Industry 4.0 platforms are accelerating adoption, as real-time monitoring and predictive maintenance become central to industrial digitalization.

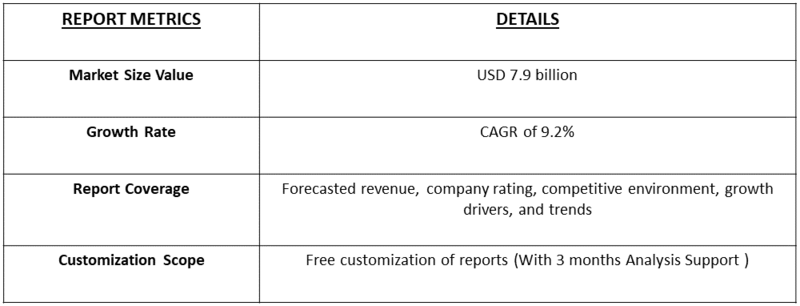

Segmentation: Global Thin Film Sensors for High-temperature Market is segmented By Sensor Type (Thin-Film Temperature Sensors, Thin-Film Pressure Sensors, Thin-Film Strain & Stress Sensors), Material Platinum Thin-Film Sensors, Nickel-Based Thin-Film Sensors, Metal-Oxide Thin-Film Sensors), Technology (Sputtering Deposition Sensors, Chemical Vapor Deposition (CVD) Sensors, Physical Vapor Deposition (PVD) Sensors), Application (Gas Turbines & Jet Engines, Industrial Furnaces & Kilns, Power Generation, Automotive & Motorsport Engines, Oil & Gas & Petrochemical Processes), End-Use Industry (Aerospace & Defense, Energy & Power, Oil & Gas), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Industries such as aerospace, power generation, metal processing, and oil & gas increasingly require precise and durable sensors capable of operating in harsh, high-temperature environments. Thin-film sensors provide superior thermal stability, fast response times, and long service life, making them ideal for gas turbines, jet engines, industrial furnaces, and high-performance automotive engines. As these sectors push for higher efficiency, safety, and performance, the need for robust sensing technology continues to accelerate, directly boosting market growth.

Continuous innovations in high-temperature-resistant materials—such as platinum thin films, ceramic composites, and silicon carbide—along with advanced deposition techniques like sputtering, PVD, and CVD, are significantly improving sensor accuracy, temperature tolerance, and reliability. These technological advancements are enabling the deployment of thin-film sensors in next-generation aircraft propulsion, nuclear and concentrated solar power systems, hydrogen combustion platforms, and industrial IoT ecosystems.

In November 2025, Researchers at Queen Mary University of London engineered a new “self-tuning” ferroelectric thin film that demonstrated exceptional responsiveness and efficiency, achieving about 74% tunability at microwave frequencies with minimal voltage. This breakthrough overcame the traditional trade-off between tunability and energy efficiency, making the material ideal for applications in 5G, 6G, radar, and medical imaging. The innovation positively impacted the global thin film sensors for high-temperature market by enabling more energy-efficient, high-performance sensors capable of reliable operation in extreme environments. As manufacturing techniques evolve and costs gradually decline, adoption of thin-film sensors across high-tech and energy-intensive applications is rapidly expanding.

Market Restraints:

One major restraint is the high cost of advanced thin-film materials and fabrication processes, particularly platinum-based and ceramic-based films, which increases overall production expenses and limits adoption in cost-sensitive industries. Additionally, the technical complexity involved in manufacturing sensors that can sustain extreme temperatures, thermal cycling, and harsh chemical environments often requires specialized equipment and expertise, creating barriers for new entrants and smaller manufacturers. Another significant challenge is ensuring long-term stability and accuracy at temperatures above 800–1,000°C, as material degradation, diffusion, oxidation, and calibration drift can impact sensor performance over time. Furthermore, limited standardization and testing protocols for ultra-high-temperature sensing technologies reduce user confidence in emerging solutions, slowing commercialization. Collectively, these factors create cost, durability, and reliability challenges that can hinder widespread adoption despite rising industrial demand.

The global thin film sensors for high-temperature market has significant socioeconomic implications, driven by its critical role in aerospace, automotive, energy, and industrial applications. These sensors enable precise monitoring and control in extreme environments, enhancing operational safety, efficiency, and product reliability. Their adoption supports technological innovation and fuels growth in advanced manufacturing, creating high-skilled employment opportunities in engineering, materials science, and sensor design. Additionally, they contribute to energy efficiency and reduced emissions, aligning with global sustainability goals. However, high production costs and limited access to advanced fabrication technologies can restrict market penetration in developing economies. Thus, the market promotes industrial modernization, fosters sustainable innovation, and strengthens economic competitiveness across key high-tech and energy-intensive sectors worldwide.

Segmental Analysis

Thin-film temperature sensors are expected to lead growth as industries demand ultra-precise thermal monitoring in extreme environments such as jet engines, gas turbines, industrial furnaces, and nuclear systems. These sensors offer rapid response, high accuracy, and superior thermal cycling endurance compared to conventional thermocouples, making them indispensable for next-generation aerospace propulsion, advanced automotive engines, and high-efficiency energy systems.

Platinum-based thin-film sensors will dominate due to their exceptional thermal stability, chemical resistance, and accuracy at temperatures exceeding 800°C. Their strength under oxidation and corrosive conditions supports usage in defense aviation, petrochemical reactors, and metal smelting operations. Growing advancements in platinum micro-coating and adhesion technologies further enhance performance, driving wider industrial adoption.

The gas turbine and aerospace engine sector represents a major growth driver as manufacturers push toward higher combustion temperatures for efficiency and reduced emissions. Thin-film sensors are increasingly embedded on turbine blades and combustion chambers for real-time temperature and strain monitoring, enabling predictive maintenance, fuel optimization, and ensuring structural integrity under extreme heat loads.

Aerospace & defense is poised for the fastest adoption due to the critical need for ultra-reliable high-temperature sensing in hypersonic vehicles, missile propulsion, aircraft engines, and space systems. Continuous defense modernization and space missions are boosting demand for thin-film sensor technologies capable of surviving extreme thermal stress, vibration, radiation, and corrosive exhaust environments.

North America will witness the highest regional growth supported by major aerospace R&D programs, advanced gas turbine manufacturers, and strong investments in clean energy and next-gen propulsion technologies. The region’s leadership in aviation innovation, defense spending, and industrial digitization accel.

In November 2025, Quantum Computing Inc. secured a contract from the National Institute of Standards and Technology (NIST) to design and fabricate thin-film lithium niobate (TFLN) photonic integrated circuits (PICs) and received a chip order from a Fortune 500 technology company serving defense, intelligence, and commercial markets. These developments advanced U.S. capabilities in high-precision photonics and thin-film technologies, positively impacting the country’s thin film sensors for high-temperature market by driving innovation, enhancing sensor performance, and supporting applications in extreme and mission-critical environments.

Similarly, in October 2025, MetaOptics Ltd, expanding its presence in semiconductor optics and metalens technology. This move strengthened cross-border collaborations in integrated photonics, nanophotonics, and semiconductor manufacturing. By extending its metalens design and production expertise to North American clients in 5G, data communications, AI semiconductors, and consumer electronics, MetaOptics advanced innovation in precision optical components. The expansion positively impacted the U.S. thin film sensors for high-temperature market by enabling the development of more compact, efficient, and high-performance sensors for extreme and high-frequency applications.

To Learn More About This Report - Request a Free Sample Copy

The Global Thin-Film Sensors for High-Temperature market is competitive and fragmented, with specialist thin-film and high-temperature sensor firms competing alongside large, diversified sensor and industrial-instrumentation corporations. Key competitive factors include materials expertise (e.g., platinum, SiC, ceramic films), micro-fabrication and deposition capabilities, high-temperature qualification (thermal cycling, oxidation resistance), system-level integration for Industry 4.0, and regional manufacturing/service footprints. Niche suppliers that focus on thin-film RTDs/thermocouples and heat-flux/pressure thin-film devices coexist with major sensor OEMs that bundle sensors into broader instrumentation and control solutions.

Key Players:

Recent Development

Q1. What are the main growth driving factors for this market?

The market is primarily driven by the increasing demand for precise and reliable monitoring in extremely harsh industrial environments, particularly in aerospace, gas turbines, and advanced manufacturing. The continuous global push towards industrial automation (Industry 4.0) and the rise of electric vehicles (EVs) require high-accuracy sensors for thermal management. Thin film technology is favored as it offers a superior combination of stability, miniaturization, and faster response times in critical, high-temperature applications.

Q2. What are the main restraining factors for this market?

Major restraining factors include the high complexity and specialized capital investment required for the precision deposition technologies (like sputtering) used in manufacturing these sensors. A key technical challenge is the coupling of temperature and strain signals at extreme temperatures, which can compromise measurement accuracy. Furthermore, long-term material degradation, oxidation, and resistance drift of the thin films under prolonged high-heat exposure remain significant hurdles that limit their lifetime and widespread adoption.

Q3. Which segment is expected to witness high growth?

The Automotive application segment is expected to witness the highest growth, specifically driven by the electrification trend. Thin film sensors are essential for the accurate thermal management and diagnostic monitoring of high-voltage battery packs and power electronics in EVs, where temperatures are critical for safety and efficiency. By sensor type, the Thin-Film Platinum Resistance Temperature Detector (RTD) segment is projected to dominate due to its recognized stability and high accuracy in industrial and demanding temperature ranges.

Q4. Who are the top major players for this market?

The market is led by companies specializing in high-performance sensing technology and industrial automation. Top major players include Heraeus Sensor Technology, Honeywell International Inc., TE Connectivity, and Innovative Sensor Technology (IST AG). These companies maintain their leadership by investing heavily in specialized thin-film deposition techniques, creating highly durable platinum and metal-alloy sensors, and integrating them into smart, predictive maintenance solutions for high-value industrial and aerospace systems.

Q5. Which country is the largest player?

North America, specifically the United States, is generally the largest market player by revenue share. This is attributed to the presence of large aerospace and defense contractors, high R&D spending on advanced propulsion systems, and a mature industrial base requiring high-precision sensors. However, the Asia Pacific region, particularly China, is strongly positioned to be the fastest-growing market due to massive investments in electronics manufacturing, rapid expansion of the domestic EV sector, and increasing automation in its industrial base.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model