Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Vein Visualization System Market encompasses advanced medical devices designed to assist healthcare professionals in locating veins for procedures such as blood draws, intravenous (IV) therapy, and injections. These systems use technologies like near-infrared (NIR) imaging and ultrasound to improve accuracy, reduce patient discomfort, and minimize procedural errors. Growing demand in hospitals, clinics, and home healthcare, coupled with technological advancements, has driven market expansion globally, improving efficiency in vascular access procedures.

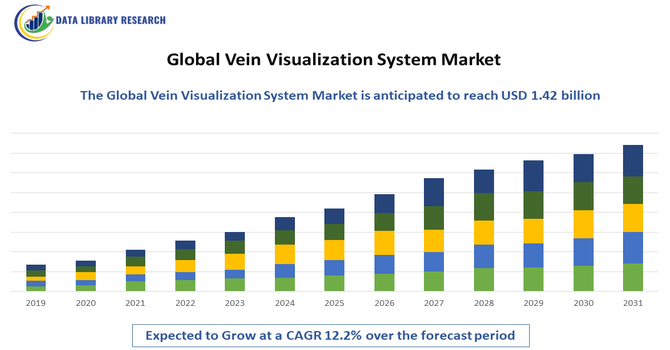

The Global Vein Visualization System Market is experiencing robust growth, driven by the increasing demand for advanced medical imaging technologies that enhance vascular access accuracy and patient safety. The rising prevalence of chronic diseases requiring frequent intravenous procedures, such as diabetes, cancer, and cardiovascular disorders, is significantly contributing to market expansion. Additionally, the growing adoption of minimally invasive procedures, coupled with technological advancements in near-infrared (NIR), ultrasound, and augmented reality-based vein visualization systems, is improving success rates in venipuncture and reducing patient discomfort.

The Global Vein Visualization System Market is witnessing several emerging trends driven by rapid technological innovation and the growing emphasis on precision healthcare. One key trend is the integration of near-infrared (NIR) and ultrasound imaging technologies to enhance vein detection accuracy, particularly in patients with difficult venous access. The adoption of wearable and handheld vein visualization devices is increasing, offering portability and ease of use in both hospital and point-of-care settings. Additionally, the incorporation of augmented reality (AR) and artificial intelligence (AI) is transforming vascular imaging by enabling real-time vein mapping and predictive analytics for improved clinical outcomes.

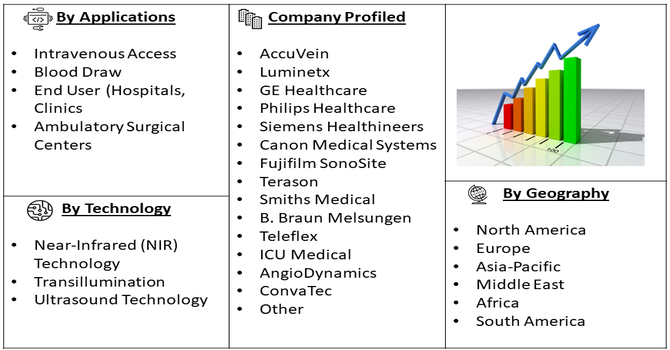

Segmentation: Global Vein Visualization System Market is segmented By Technology (Near-Infrared (NIR) Technology, Transillumination and Ultrasound Technology), Application (Intravenous Access, and Blood Draw), End User (Hospitals, Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

One of the primary drivers of the Global Vein Visualization System Market is the growing prevalence of chronic and lifestyle-related diseases that require frequent intravenous interventions. Conditions such as diabetes, cancer, cardiovascular disorders, and renal diseases often necessitate repeated venipuncture for drug administration, chemotherapy, or blood sampling. This has led to a significant increase in the demand for accurate and efficient vein access solutions. Vein visualization systems, particularly those using near-infrared (NIR) and ultrasound technologies, assist healthcare professionals in locating veins quickly and precisely, reducing the number of failed attempts and improving patient comfort. The growing geriatric population, which often presents challenges in vascular access due to fragile or invisible veins, further amplifies the need for these advanced systems. Consequently, the adoption of vein visualization devices is expanding rapidly across hospitals, emergency departments, and long-term care facilities to improve procedural efficiency and patient safety.

Continuous advancements in imaging technologies have been a key catalyst for the growth of the vein visualization system market. The development of near-infrared (NIR) imaging, augmented reality (AR), and portable ultrasound-based systems has transformed the way clinicians perform venipuncture and vascular access procedures. Modern devices offer real-time, high-resolution visualization of subcutaneous veins, enabling healthcare providers to make more precise punctures even in patients with difficult venous access. Moreover, the integration of artificial intelligence (AI) and machine learning (ML) algorithms in newer systems is enhancing image clarity, vein pattern recognition, and procedural guidance. The trend toward handheld, wireless, and battery-powered devices is further driving adoption across diverse healthcare settings, including emergency care, home healthcare, and ambulatory centers. These technological innovations not only improve accuracy and workflow efficiency but also contribute to cost savings by minimizing procedural failures and reducing the need for repeated venipuncture attempts.

Market Restraints

The major restraints hampering the growth of the Global Vein Visualization System Market is the high cost associated with advanced imaging devices. Vein visualization systems, particularly those based on near-infrared (NIR) and ultrasound technologies, require substantial investment in equipment, maintenance, and staff training. This poses a financial burden for small and medium-sized healthcare facilities, especially in developing countries where hospital budgets are constrained. Additionally, reimbursement policies for these devices are often inadequate or non-existent in emerging markets, further discouraging adoption. As a result, despite their clinical benefits, many healthcare providers in low- and middle-income regions continue to rely on traditional vein-finding techniques, which limits the market’s overall penetration.

The Global Vein Visualization System Market has a significant socioeconomic impact by directly improving healthcare efficiency and patient safety. By dramatically reducing the rate of failed venipunctures, these systems save valuable clinical time and decrease the waste of supplies, leading to substantial cost savings for hospitals and healthcare systems. More importantly, they enhance the patient experience by minimizing pain, anxiety, and the risk of complications like bruising and infection, particularly for vulnerable populations such as children and the elderly. This improvement in clinical effectiveness and patient satisfaction contributes to higher quality of care and better overall hospital performance metrics.

Segmental Analysis:

The Near-Infrared (NIR) Technology segment dominates the market due to its high accuracy, non-invasive nature, and superior visualization of veins located deep under the skin. NIR-based systems are increasingly adopted in hospitals and clinics as they reduce failed venipuncture attempts, enhance patient comfort, and improve procedural efficiency. The growing integration of NIR technology with portable and handheld devices further supports its widespread use, particularly in pediatric, geriatric, and obese patient populations.

The Intravenous Access segment accounts for the largest market share, driven by the rising demand for accurate vein detection during IV therapy, fluid administration, and blood sampling procedures. With the increasing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders that require regular IV interventions, the adoption of visualization systems to improve accuracy and minimize patient discomfort has grown significantly.

The Hospitals segment holds the leading position owing to the high patient volume, frequent need for intravenous therapies, and continuous technological upgrades in healthcare facilities. Hospitals are increasingly investing in vein visualization systems to enhance clinical outcomes, reduce procedural complications, and optimize workflow efficiency.

The North America region is expected to witness the highest growth over the forecast period in the Global Vein Visualization System Market. This growth is driven by the presence of a highly developed healthcare infrastructure, increasing adoption of advanced medical imaging technologies, and growing emphasis on patient safety and comfort during venipuncture procedures. For instance, in April 2025, Boston Scientific Corporation reported positive 12-month primary endpoint results from the second phase of the ADVANTAGE AF clinical trial, evaluating the FARAPULSE Pulsed Field Ablation (PFA) System and FARAPOINT PFA Catheter in patients with persistent atrial fibrillation. The key findings were presented at the PFA Live Case Summit in San Diego and published in Circulation. This advancement demonstrated improved procedural accuracy and safety, positively impacting the adoption of vein visualization and cardiac imaging technologies globally.

The region’s strong focus on reducing procedural errors, coupled with high healthcare spending and supportive government initiatives for technological innovation in hospitals and clinics, further supports market expansion. Additionally, the rising prevalence of chronic diseases requiring frequent intravenous access, along with the growing geriatric population, is fueling the demand for vein visualization systems across the United States and Canada.

To Learn More About This Report - Request a Free Sample Copy

The Global Vein Visualization System Market is competitive and comprises a mix of specialized vein-imaging device manufacturers and large medical-imaging and vascular-access companies. Market players compete on imaging accuracy, portability, ease of use, integration with clinical workflows, and after-sales support, while pursuing product innovation, strategic partnerships, and regional expansion to capture growing demand across hospitals, clinics, and ambulatory settings.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the increasing difficulty of successful venipuncture (starting an IV or drawing blood), especially in certain patient groups like pediatric, geriatric, obese, or chronically ill patients who have challenging veins. Repeated, failed attempts cause pain and anxiety for patients and lead to wasted time and resources for clinicians. Vein visualization systems address this by using near-infrared light to display a real-time map of the vasculature on the skin surface. This ability to significantly reduce first-stick failure rates and prevent complications like hematomas is accelerating adoption in emergency rooms and hospitals globally.

Q2. What are the main restraining factors for this market?

The biggest constraint on the market is the high initial cost of advanced vein visualization devices, particularly the capital expenditure required for sophisticated infrared projectors and portable units. For smaller clinics or healthcare facilities in developing regions, this upfront investment can be difficult to justify, limiting widespread adoption. Additionally, while the technology is effective, there can be a steep learning curve for staff to integrate the device seamlessly into their workflow. In some settings, lack of proper training or skepticism about its value can also slow down the utilization and purchase of new systems.

Q3. Which segment is expected to witness high growth?

The Portable Devices Segment is projected to witness the highest growth rate. While traditional fixed or cart-mounted systems are common, portable, handheld devices offer unparalleled versatility and ease of use. They can be quickly moved between different clinical settings, such as different patient rooms, outpatient clinics, or even ambulances, without complex setup. This mobility makes them ideal for emergency situations and departments with high patient turnover. Furthermore, continuous improvements in battery life and image clarity in compact units make the portable option increasingly attractive to healthcare providers focused on efficiency.

Q4. Who are the top major players for this market?

The Global Vein Visualization System Market features several major international players specializing in medical imaging and diagnostics. Key companies dominating this space include Christie Medical Holdings (with its VeinViewer product), AccuVein (famous for its handheld device), Vyaire Medical (through its acquired assets), and Infrared Imaging Systems. These top players focus on continuous innovation, such as integrating features like image capture and network connectivity. Their strong distribution networks, existing relationships with major hospitals, and robust intellectual property portfolios solidify their market leadership.

Q5. Which country is the largest player?

North America, particularly the United States, is the largest and most dominant regional player in the Vein Visualization System Market. This dominance stems from the region's high healthcare spending, early adoption of advanced medical technology, and a well-established infrastructure for reimbursement. Furthermore, a high awareness among both clinicians and patients about the benefits of improved venipuncture success—especially in complex patient care settings like oncology and emergency medicine—drives strong demand. The presence of major market headquarters in the U.S. also contributes to its market leadership.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model