Get Complete Analysis Of The Report - Download Updated Free Sample PDF

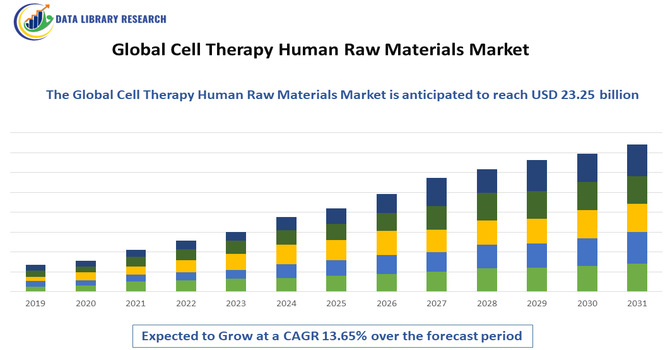

The Global Cell Therapy Human Raw Materials Market comprises biological and ancillary inputs required for manufacturing and developing cell based therapeutic products. These raw materials include GMP grade cell culture media, growth factors, human serum, leukopaks, extracellular matrices, reagents, and ancillary supplies used in clinical trials and commercial production of cell therapies like CAR T, stem cell, and regenerative medicine products. Increasing clinical pipelines, rising investment in cell therapy infrastructure, and expanding regenerative medicine applications have driven demand for high quality, traceable materials that meet stringent regulatory standards. This market is critical in ensuring the safety, efficacy, and scalability of advanced therapeutic modalities worldwide.

Emerging trends in the cell therapy human raw materials market include the shift toward chemically defined and synthetic alternatives to reduce reliance on donor derived inputs and improve consistency. Adoption of advanced bioreactor systems and automated cell culture technologies has increased demand for specialized raw materials tailored to scalable manufacturing platforms. Strategic partnerships between raw material suppliers and biopharmaceutical developers enhance supply reliability and innovation in media formulations. Additionally, integration of AI and machine learning is beginning to optimize raw material sourcing and formulation design, while regional production localization helps reduce supply chain bottlenecks and improve responsiveness to global demand across clinical and commercial ecosystems.

Segmentation: The Global Cell Therapy Human Raw Materials Market is segmented by Product Type (Cell Culture Media, Growth Factors & Cytokines, Serum & Serum Substitutes, Buffers & Reagents, GMP Grade Ancillary Materials, Biomaterials & Scaffolds, Cryoprotectants & Storage Solutions and Other Consumables), Source (Human Derived Materials, Animal Derived Materials, Synthetic & Chemically Defined Materials and Recombinant Materials), Application (CAR T Cell Therapy, Stem Cell Therapy, Regenerative Medicine, Gene Therapy, Immunotherapy and Other Cell Based Therapeutics), End User (Biopharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutions, Hospitals & Clinical Laboratories, Cell Banks & Biorepositories and Government & Regulatory Agencies), Quality/Grade (GMP (Good Manufacturing Practice) Grade, Clinical Research Grade and Research Grade Materials), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

To Learn More About This Report - Request a Free Sample Copy

Market Drivers:

A primary driver of the global cell therapy human raw materials market is the rapid expansion of cell therapy clinical pipelines worldwide. Increasing numbers of clinical trials—spanning CAR T, regenerative, and gene therapies—generate sustained demand for high quality raw materials like GMP grade media, growth factors, human serum, and ancillary consumables. For instance, in June 2025, Multus Biotechnology launched Proliferum® P, the first AI-optimized, animal component-free serum replacement for porcine adipose-derived stem cells. The product accelerated development efficiency, enhanced culture performance, and expanded high-quality raw material options, driving innovation and strengthening growth in the Global Cell Therapy Human Raw Materials Market.

As therapies advance from early stage research to late stage and regulatory review, material requirements scale significantly, necessitating reliable supply chains. Regulatory programs that expedite review and approval have further intensified raw material consumption. This growth in clinical activity fuels investment and accelerates infrastructure development for manufacturing and distribution of essential inputs.

Rising investment in regenerative medicine and cell therapy manufacturing infrastructure has been a key growth driver in the cell therapy human raw materials market. Expanded funding for cleanroom facilities, specialized media production, and automated bioprocess systems enhances capacity for raw material manufacturing and distribution.

Government initiatives support biotech infrastructure expansion, while private sector capital bolsters scale up capabilities for GMP compliant supplies. For instance, in February 2026, Indian Union Minister, Dr Jitendra Singh announced the first national call for the BIRAC–RDI Fund under India’s INR 1 lakh crore RDI initiative. The move accelerated government support for biotech infrastructure, fostered innovation in high-impact biotechnology, and strengthened growth and investment in the Global Cell Therapy Human Raw Materials Market. This investment also enables supply diversification, reducing dependency on limited suppliers and enhancing global availability. As biopharmaceutical companies and contract manufacturers grow capacity to meet clinical and commercial demands, the associated increase in raw material procurement drives broader market expansion.

Market Restraints:

A significant restraint on market growth is the complexity of regulatory and quality requirements for human derived raw materials. GMP compliance, donor eligibility documentation, and traceability standards create high barriers for suppliers and increase production costs. Disparate regional regulatory frameworks complicate material validation and cross border supply, requiring redundant testing and segmented supply chains. Documentation demands and traceability obligations add operational complexity. Additionally, stringent safety and quality demands—mandated by authorities such as the FDA and EMA—heighten cost structures for specialized inputs. These regulatory hurdles can slow market entry for emerging suppliers and impede supply flexibility, limiting the speed at which cell therapy manufacturing can scale.

The global cell therapy human raw materials market has significant socioeconomic implications by enabling the development and commercialization of advanced therapies that address cancer, autoimmune diseases, and genetic disorders. Reliable raw material supplies support research institutions and biotech firms, accelerating clinical progress and healthcare innovations. As cell therapies increasingly enter mainstream use, the market contributes to job creation in manufacturing, quality assurance, and supply chain sectors. Improved access to standardized raw materials reduces production risk and costs, potentially lowering therapy prices and expanding patient access. Investments in regional production infrastructure also promote biotechnology ecosystem growth in developing markets, boosting local economic development and scientific capacity.

Segmental Analysis:

The Cell Culture Media segment was expected to witness the highest growth over the forecast period due to its critical role in supporting cell proliferation, differentiation, and viability in cell therapy manufacturing. Increasing demand for CAR T therapies, stem cell therapies, and regenerative medicine applications has fueled the need for high-quality, GMP-grade media. Advances in chemically defined, serum-free, and xeno-free formulations have improved safety, reproducibility, and regulatory compliance. Biopharmaceutical manufacturers and CDMOs prefer standardized, scalable media to reduce batch variability and enhance therapeutic efficacy. The growing number of clinical trials and commercialization of cell therapies globally further accelerated adoption and market expansion.

The Animal-Derived Materials segment was projected to record the highest growth due to its widespread use in traditional and specialized cell culture applications. Materials such as fetal bovine serum (FBS), bovine serum albumin, and growth supplements are essential for certain stem cell, regenerative, and immunotherapy processes. Despite the growing shift toward synthetic alternatives, animal-derived inputs remain critical for established protocols and clinical trials requiring proven performance. High reliability, consistent supply, and regulatory acceptance have sustained demand. Emerging markets, increasing production of advanced cell therapies, and ongoing R&D in both clinical and preclinical settings further supported the rapid expansion of this segment globally.

The Stem Cell Therapy segment was expected to witness the fastest growth due to rising applications in regenerative medicine, hematology, and tissue engineering. Increasing prevalence of chronic diseases, organ failure, and degenerative disorders has driven clinical adoption of stem cell–based interventions. Both autologous and allogeneic stem cell therapies require high-quality human raw materials, creating robust demand for specialized culture media, cytokines, and cryoprotectants. Regulatory approvals of advanced stem cell products and expansion of manufacturing facilities by biopharmaceutical companies and CDMOs have further accelerated growth. The ongoing investment in research and commercialization of stem cell therapies globally continues to drive this segment.

The Biopharmaceutical & Biotechnology Companies segment was anticipated to record the highest growth owing to the increasing number of organizations developing CAR T, stem cell, and gene therapies. These companies rely heavily on high-quality human raw materials for research, preclinical development, and commercial manufacturing. Expansion of GMP-compliant production facilities and outsourcing partnerships with CDMOs has further increased material procurement. Strategic collaborations, mergers, and investments by biopharmaceutical firms also drive bulk demand. The focus on pipeline acceleration, regulatory compliance, and scalable manufacturing of novel cell therapies ensures that biopharmaceutical and biotechnology companies remain the dominant consumers in the global human raw materials market.

The GMP (Good Manufacturing Practice) Grade segment was projected to witness the highest growth due to increasing regulatory requirements for cell therapy manufacturing. GMP-grade raw materials, including media, growth factors, and sera, ensure product safety, traceability, and reproducibility. As clinical trials advance to late-stage phases and commercial-scale production rises, manufacturers prioritize GMP-certified inputs to meet FDA, EMA, and other regulatory standards. Adoption of GMP-grade materials reduces risks of contamination, batch variability, and supply chain disruptions. The emphasis on quality assurance, standardization, and compliance in cell therapy pipelines globally has accelerated demand and strengthened this segment’s market growth.

The North American region was expected to witness the highest growth due to the presence of advanced healthcare infrastructure, strong research capabilities, and early adoption of cell therapies. The United States and Canada host leading biopharmaceutical companies, CDMOs, and clinical trial networks, driving high demand for human raw materials.

Favourable regulatory frameworks, government funding for regenerative medicine, and growing investments in CAR-T and stem cell therapy development further accelerated market expansion. For instance, the recent approval of Omisirge (omidubicel-onlv) in December 2025, by the U.S. Food and Drug Administration marks a pivotal advancement in the treatment landscape for severe aplastic anemia (SAA) and hematologic malignancies. As the first hematopoietic stem cell transplant (HSCT) therapy approved for SAA patients as young as six years old who lack a compatible donor, this decision significantly broadens access to potentially life-saving treatment.

Technological innovation, widespread GMP-compliant manufacturing facilities, and strategic collaborations strengthened supply chains. The combination of advanced infrastructure, robust R&D, and regulatory support positioned North America as the fastest-growing regional market globally.

The competitive landscape is moderately consolidated, featuring global life science and biotech supply leaders alongside specialized raw material innovators. Major players emphasize portfolio diversification, GMP compliant production, and strategic collaborations to meet complex cell therapy requirements. Companies like Thermo Fisher Scientific, Merck KGaA, Lonza Group, Sartorius AG, and Miltenyi Biotec leverage extensive product offerings and manufacturing capabilities to serve clinical stage and commercial clients. Smaller niche suppliers focus on specialized biomaterials and reagents to differentiate offerings. Regional production facilities and localized supply chains are increasingly used to reduce lead times and support regional demand. Overall competition is driven by quality, regulatory compliance, integrated solutions, and global distribution capacity.

The major players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

Market growth is primarily driven by the rising volume of clinical trials and commercial approvals for CAR-T and stem cell therapies. The increasing global prevalence of chronic diseases like cancer and autoimmune disorders necessitates advanced treatments. Furthermore, a strategic shift toward chemically defined and xeno-free materials is enhancing production safety and scalability.

Q2. What are the main restraining factors for this market?

Growth is hindered by stringent regulatory requirements and complex compliance standards for sourcing donor-derived biological materials. The high cost of R&D and specialized manufacturing infrastructure limits entry for smaller firms. Additionally, global supply chain vulnerabilities and a shortage of GMP-grade raw materials create bottlenecks in large-scale commercial production.

Q3. Which segment is expected to witness high growth?

The Cell Culture Media segment is expected to witness the highest growth. This is due to its critical role in maintaining cell viability and the industry-wide move toward specialized, serum-free formulations. Geographically, the Asia-Pacific region is emerging as the fastest-growing market, driven by expanding biotech infrastructure in China and India.

Q4. Who are the top major players for this market?

The market is dominated by global life sciences leaders, including Thermo Fisher Scientific, Merck KGaA, and Danaher Corporation (Cytiva). Other influential players include Lonza, Sartorius AG, Miltenyi Biotec, and STEMCELL Technologies. These companies lead through extensive distribution networks, regulatory expertise, and advanced product portfolios covering media, reagents, and supplements.

Q5. Which country is the largest player?

The United States is the largest player, accounting for over 40% of the global market share. Its dominance is supported by a massive concentration of biopharmaceutical companies, robust government funding for regenerative medicine, and a well-established regulatory framework (FDA) that encourages the rapid commercialization of advanced cell-based therapies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model