Get Complete Analysis Of The Report - Download Updated Free Sample PDF

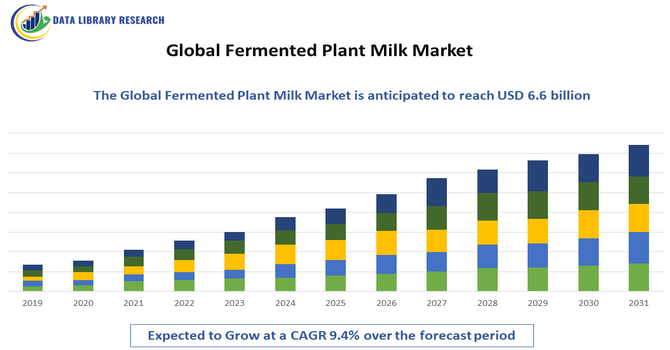

The Global Fermented Plant Milk Market encompasses production and distribution of fermented, plant based milk products created through microbial fermentation of plant milks derived from oats, soy, almond, coconut, rice, and other botanical sources. These products include yogurt style cultured beverages, kefir like drinks, and spoonable fermented milks that deliver probiotic and digestive health benefits without dairy ingredients. Growth is driven by shifting consumer preferences toward vegan, lactose free, and functional foods, along with sustainability and environmental concerns. Fermented plant milk combines the nutritional appeal of traditional fermented dairy with plant based attributes, offering enhanced taste profiles, improved gut health, and eco friendly positioning in global retail and foodservice.

Current trends in the fermented plant milk market include clean label formulations, improved texture and flavor improvements, and expansion of product formats such as drinkable yogurts and kefir style cultured beverages. Innovations in fermentation technology have enhanced probiotic viability and sensory qualities, increasing consumer acceptance. Environmental sustainability and health consciousness continue to motivate purchases, while major food companies and startups alike introduce premium and fortified variants. Retailers also broaden placement across mainstream grocery and online channels. Rising popularity of hybrid products (mixing plant bases with functional ingredients, like prebiotics) and partnerships between fermentation tech firms and plant based brands further reinforce expansion momentum.

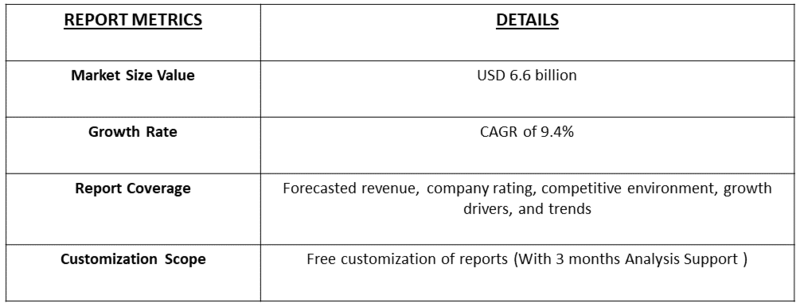

Segmentation: The Global Fermented Plant Milk Market is segmented by Product Type (Drinkable Fermented Plant Milk, Spoonable Fermented Plant Milk, and Other Products), Raw Material (Soy, Oat, Almond, Coconut, Rice and Others), Application (Retail, Foodservice and Online / E-commerce), Distribution Channel (Supermarkets, Specialty Stores, Convenience Stores, Online Channels and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver of the fermented plant milk market has been consumer demand for health oriented and functional foods. Increasing awareness of gut health and probiotics has led consumers to seek fermented products that support digestion and overall wellness without dairy ingredients. Fermented plant milk offers both plant based and probiotic benefits, appealing to lactose intolerant, vegan, and health conscious segments. This demand amplifies with growing interest in natural and minimally processed foods, encouraging both established brands and startups to innovate with cultured plant based formats such as kefir style drinks and spoonable yogurts. The broader functional foods trend is a strong long term growth catalyst.

Environmental sustainability has strongly driven the fermented plant milk market. Plant derived milks generally have lower greenhouse gas emissions, water usage, and land requirements compared to dairy, resonating with eco conscious consumers and younger demographics.

Fermented variants extend this appeal by offering enhanced nutrition, creating a compelling alternative to traditional dairy cultures. For instance, in Febarury 2026, Blue Diamond Growers launched Blue Diamond Almondmilk in four varieties, emphasizing quality, authenticity, and sustainable almond sourcing. The line, featuring simple, creamy, and protein-rich options, highlighted environmentally conscious production and ingredient transparency. This launch reinforced consumer awareness of sustainable plant-based choices and positively influenced growth in the global fermented plant milk market.

Sustainability narratives influence purchasing behavior, prompting food manufacturers to expand fermented plant offerings and align with broader corporate environmental, social, and governance (ESG) goals. Retailers, foodservice companies, and investors increasingly back plant based fermentation innovations, bolstering market expansion across North America, Europe, and Asia Pacific.

Market Restraints:

A key restraint for the fermented plant milk market is production complexity and shelf life stability challenges. Plant based substrates often behave differently than dairy during fermentation, requiring specialized cultures and process controls to ensure desirable texture, flavor, and probiotic viability, which increases production costs and technical barriers. Additionally, many fermented plant milk products require cold chain logistics to maintain quality from production through retail, limiting distribution in regions with underdeveloped refrigeration infrastructure and increasing operational expenses. Variability in taste and texture across brands also reduces adoption among traditional dairy consumers. These factors constrain market expansion, particularly for smaller producers without strong cold chain capabilities.

The fermented plant milk market has positively shaped socioeconomic dynamics by creating new value chains for plant agriculture, supporting jobs in food tech, production, and distribution infrastructure. Consumer demand for plant based probiotics has expanded opportunities for small and medium enterprises, especially those focusing on local ingredient sourcing and artisanal fermentation. By offering alternatives to dairy products, the market also addresses lactose intolerance and dietary restrictions, improving accessibility to nutritious fermented foods. On a broader economic scale, investment from multinational food companies has increased R&D funding and cross border trade of specialty plant fermented products. Additionally, the sustainability narrative appeals to environmentally conscious consumers and supports more climate friendly food systems.

Segmental Analysis:

The spoonable fermented plant milk segment experienced the highest growth over the forecast period due to rising consumer demand for yogurt-style, probiotic-rich products. Its versatility, texture, and flavor appeal made it popular among health-conscious and vegan consumers seeking functional foods. Product innovations, including plant-based spoonable yogurts fortified with vitamins and prebiotics, expanded market penetration. Major brands launched premium, organic, and flavored variants to cater to diverse tastes. Additionally, retail expansion, sampling campaigns, and e-commerce availability strengthened adoption, positioning spoonable fermented plant milk as a leading growth driver in the overall fermented plant milk market.

The almond-based fermented plant milk segment witnessed the highest growth over the forecast period due to its mild taste, nutritional profile, and popularity as a dairy alternative. Almond milk offered a low-calorie, plant-based base suitable for probiotic fermentation, attracting vegan and lactose-intolerant consumers. Flavor innovations and fortified formulations increased adoption in spoonable and drinkable products. Growing awareness of heart-healthy benefits and sustainable almond sourcing further supported market expansion. Both global brands and regional producers leveraged almond-based fermentation to diversify product portfolios, meeting rising consumer demand for functional, plant-based fermented alternatives in retail, foodservice, and online channels.

The retail distribution segment recorded the highest growth during the forecast period as supermarkets, hypermarkets, and specialty stores expanded plant-based product offerings. Fermented plant milk benefited from prominent shelf placement, promotions, and consumer accessibility, boosting sales and awareness. Retailers increasingly stocked diverse product formats, flavors, and plant bases to cater to health-conscious, vegan, and functional-food consumers. Direct engagement through in-store sampling, promotions, and branding strengthened adoption. E-commerce channels complemented physical retail, but retail outlets remained the primary revenue contributor. This segment’s growth reflected rising consumer willingness to explore plant-based fermented alternatives as part of daily diets across developed and emerging markets.

The supermarkets distribution segment experienced the highest growth over the forecast period due to its ability to reach mass-market consumers efficiently. Supermarkets offered broad visibility, diverse product placement, and promotional campaigns that increased awareness of fermented plant milk. Large-format stores provided space for premium, flavored, and fortified plant-based fermented options, appealing to families and health-conscious buyers. Strategic partnerships between brands and supermarket chains improved product availability and shelf rotation. Frequent promotions, discounts, and loyalty programs further accelerated adoption. Supermarkets emerged as the dominant distribution channel, driving growth across regions and playing a key role in introducing fermented plant milk to new consumers.

The North American region witnessed the highest growth over the forecast period due to early adoption of plant-based, functional, and probiotic foods. Rising health awareness, lactose intolerance, and veganism drove strong demand for fermented plant milk products.

Innovation in spoonable yogurts, drinkable kefir-style beverages, and fortified options supported market expansion. For instance, Remilk partnered with Gad Dairies to launch the precision-fermented “New Milk” in Israel, offering animal-free milk identical in taste and function to traditional dairy. With regulatory approvals from the US FDA and other authorities, this launch advanced innovation and consumer acceptance, positively impacting the growth of North America’s fermented plant milk market.

Similarly, in 2025, Premier Protein expanded its ready-to-drink lineup by launching Almondmilk Non-Dairy Protein Shakes in North America. Made with real almond milk, the shakes delivered 20 g of protein, low sugar, and reduced calories while maintaining taste. This introduction boosted consumer adoption of plant-based beverages and supported growth in the North American fermented plant milk market.

Well-established retail networks, e-commerce platforms, and strong cold-chain infrastructure facilitated product distribution and accessibility. Major brands and startups launched region-specific flavors and fortified products to cater to diverse consumer preferences. Combined with government support for sustainable food systems and environmental awareness, North America emerged as a leading growth market.

To Learn More About This Report - Request a Free Sample Copy

The global fermented plant milk market is moderately consolidated, with both established multinational food companies and innovative niche brands competing across innovation, distribution, and branding. Major food manufacturers deploy extensive R&D capabilities and large distribution networks to launch new plant based fermented lines, while smaller firms often differentiate through organic, artisanal, or regional product offerings. Strategic activities include product diversification, brand partnerships, and expansion into emerging retail channels like e commerce. Collaboration with fermentation technology providers and investments in sensory quality improvements are key competitive strategies. Competitive pressures also stem from traditional dairy and plant non fermented milk producers entering cultured segments to capture probiotic oriented consumers.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary drivers include the rising global prevalence of lactose intolerance and a significant shift toward veganism for ethical and environmental reasons. Additionally, growing consumer awareness regarding gut health has spurred demand for probiotic-rich fermented products. Innovations in flavor profiles and improved nutritional fortification are making plant-based milks more appealing.

Q2. What are the main restraining factors for this market?

The high cost of premium raw materials and specialized fermentation processes often results in higher retail prices compared to traditional dairy. Furthermore, achieving a texture and taste profile that mimics dairy remains a technical challenge. Limited availability in emerging markets and strict labeling regulations for "milk" products also hinder expansion.

Q3. Which segment is expected to witness high growth?

The almond segment was expected to witness the highest growth over the forecast period due to its mild flavor, nutritional benefits, and popularity as a dairy alternative. Almond-based fermented plant milk appealed to vegan, lactose-intolerant, and health-conscious consumers, while product innovations and fortified formulations further accelerated adoption across retail and foodservice channels.

Q4. Who are the top major players for this market?

Key industry leaders include Danone (through brands like Alpro and Silk), Oatly, and Chobani, which has expanded into non-dairy fermentation. Other significant players include General Mills, Blue Diamond Growers, and Califia Farms. These companies are aggressively investing in R&D to enhance the probiotic count and shelf-life of their products.

Q5. Which country is the largest player?

The United States is currently the largest player in the fermented plant milk market. This dominance is attributed to a highly developed retail infrastructure, high consumer spending on health-conscious products, and a robust startup ecosystem. Large-scale adoption of dairy alternatives in American food service sectors further cements its leading market position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model