Get Complete Analysis Of The Report - Download Updated Free Sample PDF

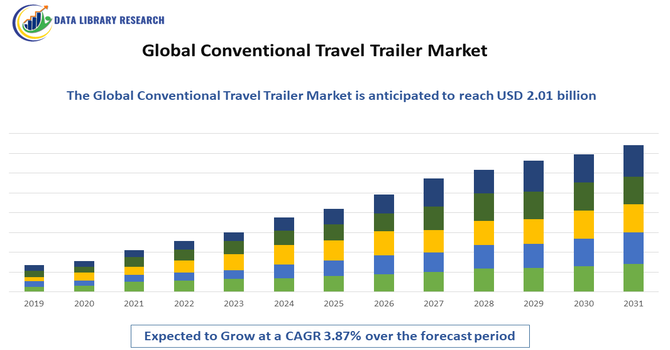

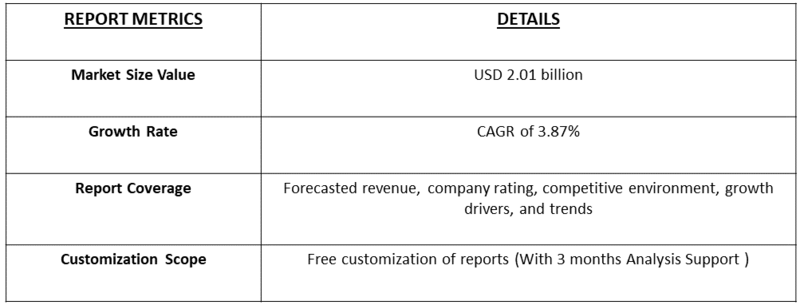

The Conventional Travel Trailer Market refers to the global industry for towable recreational vehicles that are hitched to a separate tow vehicle, offering living space and amenities for road travel and outdoor recreation. These trailers vary in size, design, and features, catering to families, adventure travelers, and outdoor enthusiasts seeking flexible vacation options without the expense of motorized RVs. Driven by increasing demand for domestic tourism, outdoor experiences, and leisure travel, the market includes lightweight, mid size, and luxury travel trailers. Manufacturers are innovating with smart technology, sustainable materials, and customizable interiors to enhance comfort, convenience, and energy efficiency for consumers worldwide.

The current market trends in the conventional travel trailer industry highlight increased demand for lightweight and smart feature equipped trailers, appealing especially to first time buyers and tech savvy travelers. Lightweight models under 6,000 lbs have grown popular, allowing SUVs and crossover vehicles to tow them easily. Sustainability is gaining traction, with more manufacturers incorporating eco friendly materials, solar panels, and energy efficient systems. Customizable interiors, modular layouts, and enhanced comfort features are also shaping product offerings. Additionally, digital rental and peer to peer sharing platforms have expanded access to travel trailers, especially among younger demographics, broadening overall market participation and travel experiences.

Segmentation: The Conventional Travel Trailer Market is segmented by Product Type (Lightweight Travel Trailers, Mid Size Travel Trailers and Luxury Travel Trailers), Size (Up to 20 feet, 21–30 feet and Over 30 feet), Tow Vehicle Compatibility (SUV Towable Models, Pickup Truck Towable Models and Van Towable Models), Construction Material (Aluminum Frame, Fiberglass Exterior and Composite Material Construction), End Use (Recreational Travelers & Families, Adventure & Outdoor Enthusiasts, Commercial & Rental Fleets and Tourism & Hospitality Services), Distribution Channel (Direct Sales (Manufacturer Dealerships), Third Party Dealers & Retailers and Online Platforms & Rentals), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A key driver for the conventional travel trailer market is the increasing demand for outdoor recreation and domestic tourism. Post-pandemic travel preferences have shifted toward flexible, self-contained travel options that offer both safety and freedom, strengthening interest in trailers as a preferred solution.

Millennials and younger travelers are particularly inclined toward weekend getaways, camping, and road trips, boosting trailer adoption. For instance, in 2026, Trip.com Group reported that the company is seeing over 34% year-on-year increase in bookings for short trips of four days or less, with growth especially prominent in Europe. Working adults, primarily those aged 25 to 49 years old, are the main drivers of this trend, accounting for more than half of the bookings for short trips of four days or less. Government investments in RV parks and outdoor infrastructure also support this trend by enhancing accessibility for travelers. Additionally, the rising RV community and culture contribute to sustained demand, making travel trailers a popular choice for those seeking adventure without relying on traditional hotel stays.

Another significant driver for market growth is technological innovation and customization within conventional travel trailers.

Manufacturers are integrating advanced features such as smart home systems, solar energy solutions, energy-efficient appliances, and IoT connectivity, enhancing convenience and sustainability. For instance, in January 2026, The Nitte Institute of Hospitality Services (NIHS) hosted the NIHS International Research Forum on Hospitality & Tourism (NIRFHT 2026), highlighting “Future Scape 2026 – Empowering Hospitality through AI and Smart Tech.” Insights on AI and smart technologies inspired innovations in travel trailer design, boosting technological customization and advancing the global conventional travel trailer market.

Customizable interiors and modular layouts allow buyers to tailor trailers to their preferences, supporting diverse travel needs and lifestyle choices. Lightweight materials and aerodynamic designs also improve fuel efficiency and towing ease. These technological advancements appeal to both first time buyers and experienced RV enthusiasts, expanding the market’s demographic reach. Enhanced performance, comfort, and eco friendly designs continue to elevate consumer interest and profitability.

Market Restraints:

A major restraint for the conventional travel trailer market is the high upfront purchase and long term ownership costs. Trailer prices vary widely—from affordable entry level models to premium luxury units—but even mid range trailers represent a significant investment for many consumers. Additional expenses include insurance, maintenance, storage, towing equipment, and accessories, which can add considerable cost over time. High material and fuel costs further increase ownership expenses, particularly during economic downturns when discretionary spending tightens. In developing markets with limited RV infrastructure, these cost barriers are even more pronounced, limiting broader adoption and slowing market penetration despite rising interest in outdoor travel.

The conventional travel trailer market has significant socioeconomic influence, particularly in tourism and leisure economies. It supports job creation in manufacturing, sales, RV parks, maintenance services, and aftermarket support, contributing to local and regional economies. Growth in RV ownership has boosted spending on outdoor recreation, campgrounds, travel services, and tow vehicles. Increased participation in domestic travel stimulates hospitality and related sectors, particularly in rural and scenic destinations. The market also encourages a culture of flexible, nature based travel, reducing reliance on traditional lodging and promoting experiential tourism. Rising disposable incomes and changing work life preferences have further sustained demand, enhancing the sector’s economic footprint.

Segmental Analysis

The mid-size travel trailers segment is projected to witness the highest growth over the forecast period due to their optimal balance between space, comfort, and towing requirements. These trailers are highly popular among families and recreational travelers seeking flexibility without the complexities of larger trailers. They accommodate essential living amenities while remaining manageable for towing by mid-sized SUVs and pickup trucks. Rising demand for family-oriented outdoor adventures, weekend getaways, and affordable vacation options is driving adoption. Additionally, manufacturers are enhancing mid-size models with modern interiors, energy-efficient appliances, and modular layouts, making them increasingly attractive to both first-time buyers and experienced RV enthusiasts.

The 21–30 feet segment is expected to witness the highest growth over the forecast period, as it offers the perfect combination of living space, maneuverability, and towing convenience. This size range appeals to families and recreational travelers who require sufficient interior amenities while still being compatible with a wide variety of tow vehicles. The segment’s popularity is also supported by increasing adoption of smart and lightweight designs that reduce fuel consumption and improve road handling. Campgrounds, RV parks, and outdoor tourism infrastructure are increasingly catering to this segment, further boosting market demand and sustaining long-term growth globally.

The composite material construction segment is expected to witness the highest growth, driven by the demand for lightweight, durable, and weather-resistant travel trailers. Composite materials offer superior strength, corrosion resistance, and lower maintenance compared with traditional aluminum or wood-based frames, enhancing trailer longevity. Additionally, the material allows for energy-efficient and aerodynamically optimized designs, reducing towing fuel costs. Manufacturers are increasingly incorporating composites into mid-size and luxury trailers to improve performance and passenger comfort. Consumer preference for eco-friendly, durable, and low-maintenance trailers is expanding adoption, making composite construction a critical growth driver across residential, recreational, and rental markets worldwide.

The recreational travelers & families segment is projected to experience the highest growth, driven by the rising popularity of domestic tourism, weekend getaways, and family-oriented vacations. Families seek convenient, self-contained travel options that provide both safety and flexibility, making conventional travel trailers an ideal choice. Increasing disposable incomes, flexible work arrangements, and growing interest in outdoor leisure activities have further fueled market demand. Manufacturers are responding by offering spacious interiors, modular layouts, and smart appliances that cater specifically to families. Additionally, RV rental services targeting family travelers are expanding, enabling access to travel trailers without the commitment of full ownership.

The third-party dealers & retailers segment is expected to witness the highest growth, as these channels provide widespread accessibility and localized customer support for travel trailer buyers. Third-party networks enable consumers to explore multiple brands and models, receive financing options, and access after-sales service and maintenance. This distribution model is particularly important for first-time buyers seeking guidance in trailer selection and towing compatibility. Growth in dealerships and retail networks in North America and Europe has increased market penetration, especially in suburban and rural regions. Enhanced marketing, demo experiences, and warranty programs offered by retailers further encourage adoption of conventional travel trailers.

The North American region is expected to witness the highest growth over the forecast period due to the continent’s mature recreational vehicle culture, robust infrastructure, and growing interest in domestic travel.

The United States, in particular, has witnessed increased adoption of conventional travel trailers driven by rising disposable incomes, outdoor lifestyle trends, and strong RV park and campground networks. For instance, AAA projected that 122.4 million Americans would travel at least 50 miles during the 13-day year-end holiday period, marking a 2.2% increase over 2024 and surpassing the previous record of 119.7 million. This surge in road travel boosted demand for conventional travel trailers, reinforcing North America’s market growth and adoption trends.

Similarly, Canada’s travel and tourism sector is projected to contribute USD 183 billion to the economy in 2025 and support 1.8 million jobs, setting new records. This robust growth and increased domestic travel demand positively impacted North America’s conventional travel trailer market, driving higher adoption for family vacations, road trips, and recreational travel.

Manufacturers continue to innovate with mid-size, lightweight, and technologically advanced models tailored to North American consumers. Additionally, regulatory support, fuel-efficient designs, and rental services have made travel trailers more accessible, reinforcing North America’s position as the leading market in terms of demand, sales, and adoption.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the conventional travel trailer market is marked by both major global manufacturers and niche producers. Industry leaders like Thor Industries and Forest River dominate through extensive product portfolios, strong distribution networks, and brand recognition. Established players invest in R&D, smart features, and sustainability to differentiate offerings, while expanding dealerships and service networks. Emerging manufacturers focus on niche segments such as ultra lightweight, off grid capable, or luxury custom trailers to compete effectively. Strategic partnerships, mergers, and geographic expansion help firms maintain market presence. Competitive pressures also drive enhancements in after sales service, warranty support, and consumer engagement to build brand loyalty.

The main players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The surge in outdoor recreation and "revenge travel" following the pandemic has significantly boosted demand. Millennials and Gen Z are increasingly adopting the nomadic lifestyle, driven by the rise of remote work. Additionally, improvements in lightweight materials and aerodynamic designs allow smaller SUVs to tow trailers, expanding the potential customer base.

Q2. What are the main restraining factors for this market?

High interest rates and rising inflation have increased the total cost of ownership, deterring budget-conscious buyers. Fluctuating fuel prices also impact the appeal of long-distance towing. Furthermore, supply chain disruptions for specialized components and a shortage of developed campsite infrastructure in certain regions can limit the market's immediate expansion potential.

Q3. Which segment is expected to witness high growth?

The Recreational Travelers & Families segment is expected to witness the highest growth over the forecast period, driven by rising domestic tourism, weekend getaways, and family-oriented vacations. Increased disposable incomes, outdoor lifestyle trends, and demand for self-contained, flexible travel options have boosted adoption of conventional travel trailers in this segment.

Q4. Who are the top major players for this market?

Thor Industries (parent of Airstream and Jayco) and Forest River dominate the landscape, holding a massive share of the North American market. Other key players include Winnebago Industries, Grand Design RV, and Gulf Stream Coach. These companies stay competitive through frequent floorplan innovations and strategic acquisitions of boutique manufacturers.

Q5. Which country is the largest player?

The United States is the undisputed leader in the conventional travel trailer market. A deep-rooted culture of road-tripping, an extensive network of national parks, and a robust manufacturing hub in Indiana drive this dominance. While Europe and Australia have significant markets, the sheer volume and scale of U.S. operations remain unparalleled.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model