Get Complete Analysis Of The Report - Download Updated Free Sample PDF

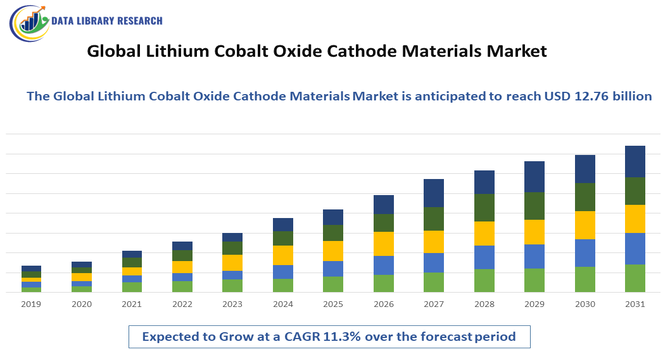

The Global Lithium Cobalt Oxide (LCO) Cathode Materials Market refers to the manufacturing, supply, and application of lithium cobalt oxide, a key cathode component in lithium ion batteries. LCO offers high energy density and stable voltage output, making it widely used in portable electronics such as smartphones, laptops, tablets, and wearables. It also plays a role in electric and hybrid vehicles as well as small scale energy storage systems. The market’s size was valued in the billions of USD in recent years and is projected to grow significantly through the next decade as demand for rechargeable battery applications increases globally, especially in consumer electronics and EV segments.

The Global Lithium Cobalt Oxide (LCO) Cathode Materials Market has been shaped by major trends in battery technology and consumer demand. Asia Pacific, especially China, dominates production and consumption due to extensive electronics manufacturing and strong EV supply chains. Innovation in surface coated LCO cathodes and hybrid cathode chemistries has improved energy density and cycle life. Manufacturers are expanding recycling and cobalt recovery efforts to mitigate ethical and supply chain concerns. At the same time, LCO’s overall share among cathode types has declined due to the rise of alternative chemistries like LFP and NMC, which offer lower cobalt usage and cost advantages.

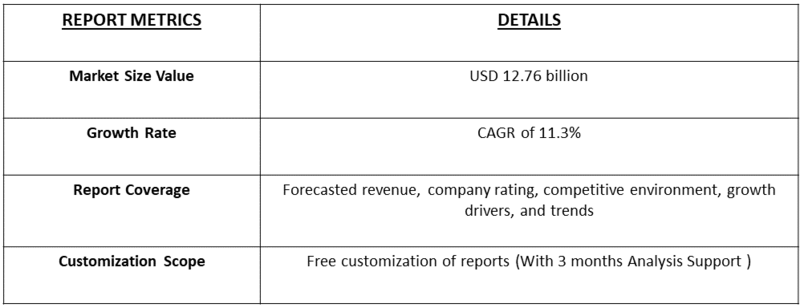

Segmentation: The Global Lithium Cobalt Oxide (LCO) Cathode Materials Market is segmented by Product Type (4.35V LCO Materials, 4.40V LCO Materials, Battery Grade LCO and Industrial Grade LCO), Application (Smartphones & Mobile Devices, Laptops & Tablets, Electric Vehicles (EVs), Energy Storage Systems (ESS) and Medical & Aerospace Devices), Purity Level (High Purity LCO, Medium Purity LCO and Low Purity LCO), End Use Industry (Consumer Electronics Manufacturing, Automotive Industry (EV/HEV), Grid & Industrial Storage and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A major driver for the LCO cathode materials market has been surging demand for portable consumer electronics that require high energy density batteries. LCO chemistry has historically been favored in smartphones, laptops, and wearables for its superior energy density relative to weight and compact form factors.

In November 2023, Toshiba Corporation developed a cobalt-free 5V-class high-potential cathode, reducing performance-degrading gas formation in lithium-ion batteries. This innovation supported higher energy density and safety, meeting rising consumer electronics demand and positively impacting growth and technological advancement in the Global Lithium Cobalt Oxide Cathode Materials Market. With global smartphone penetration high and replacement cycles continuing, demand for LCO based batteries remains strong. This demand is further bolstered by premium device segments and expansion of laptop and tablet usage worldwide. Manufacturers have responded with coated cathode materials and hybrid formulations to improve performance, sustaining market growth despite competition from alternative chemistries.

Another key driver has been expanding applications in electric and hybrid vehicles and energy storage systems. While LCO is less dominant in EVs compared to other cathode chemistries, it is still deployed in certain hybrid electric vehicles and specialized battery packs where energy density is prioritized. The broader push toward electrification and grid storage has increased overall lithium ion battery production, indirectly supporting LCO material growth. Institutional support for EV adoption and renewable energy storage has stimulated investments in battery manufacturing capacity. Partnerships between battery materials producers and automotive OEMs have further strengthened supply chains for LCO cathodes.

Market Restraints:

A significant restraint on the LCO cathode materials market has been the rise of alternative cathode chemistries that reduce reliance on cobalt due to cost, supply risk, and ethical concerns. Lithium iron phosphate (LFP) and high nickel NMC variants (nickel manganese cobalt) offer comparable performance with lower cobalt content, making them increasingly preferred for EVs and large scale storage. The LCO share of total cobalt demand has declined sharply over recent years as manufacturers balance performance with sustainability and cost. This shift has pressured LCO market growth, particularly in segments that prioritize price and scale over the highest energy density.

The LCO cathode materials market has significant socioeconomic implications due to its role in powering consumer electronics, EVs, and energy storage systems. High demand for portable devices and electric mobility fuels economic activity across manufacturing, logistics, and R&D sectors. Expansion of battery supply chains supports job creation and technological investment in major production hubs, particularly in Asia. However, heavy reliance on critical minerals like cobalt has raised social and ethical concerns about mining practices, particularly in the Democratic Republic of Congo, prompting initiatives for more responsible sourcing and recycling. Growth in LCO production also contributes to broader digitalization and renewable energy adoption globally.

Segmental Analysis:

The battery-grade LCO segment was expected to witness the highest growth over the forecast period due to its critical role in high-performance lithium-ion batteries. These materials provide superior energy density, stable voltage output, and long cycle life, making them ideal for premium consumer electronics and niche EV applications. Increasing demand for reliable, high-capacity batteries in smartphones, laptops, and portable medical devices drove manufacturers to invest in battery-grade LCO production. Technological advancements, including surface coatings and enhanced particle uniformity, improved performance and safety. Strategic partnerships between LCO producers and battery manufacturers also expanded supply chains, reinforcing this segment’s dominance and accelerating global market growth.

The smartphones and mobile devices segment was expected to witness the highest growth over the forecast period as LCO cathodes continued to dominate high-energy-density applications. The proliferation of smartphones, tablets, and wearable devices globally increased reliance on LCO batteries due to their compact size and long-lasting power. Premium and flagship device launches, particularly in Asia-Pacific and North America, fueled consistent demand. Manufacturers prioritized battery performance, cycle stability, and thermal safety, driving innovation in cathode coatings and hybrid LCO blends. The segment also benefited from rapid device replacement cycles and growing 5G adoption, ensuring steady demand for LCO cathode materials and contributing significantly to overall market expansion.

The high-purity LCO segment was expected to witness the highest growth over the forecast period due to the demand for precision-engineered batteries in electronics and specialized applications. High-purity LCO offers improved energy density, voltage stability, and cycle life, which is critical for premium consumer devices, aerospace electronics, and medical equipment. Manufacturers invested in advanced refining and quality control processes to meet stringent purity standards. Rising adoption of high-performance portable electronics and niche EV applications further accelerated demand. Additionally, research into surface coatings and particle optimization enhanced thermal stability and safety. These factors positioned high-purity LCO as a preferred material for critical battery applications globally.

The automotive industry (EV/HEV) segment was expected to witness the highest growth over the forecast period due to the global push toward electrification. While LCO is less used than NMC or LFP in large EV batteries, it remains critical for hybrid electric vehicles and high-energy-density battery modules. Demand for lightweight, efficient, and reliable batteries in compact EVs and plug-in hybrids fueled growth. Collaborations between battery material suppliers and automotive OEMs ensured consistent LCO supply for advanced powertrains. Regulatory incentives for electric mobility and increasing consumer adoption of EVs worldwide further drove production. These trends reinforced LCO’s role in the automotive battery sector and the global cathode materials market.

The Asia-Pacific region was expected to witness the highest growth over the forecast period as the hub of LCO production and consumption.

China, Japan, and South Korea dominated both raw material supply and battery manufacturing for consumer electronics, EVs, and energy storage systems. For instance, in November 2025, POSCO Future M’s Cathode Material Development Group successfully developed lithium manganese-rich (LMR) cathode materials in Korea, enhancing battery energy density and performance. This advancement strengthened regional technological leadership, attracted industry attention, and positively influenced the growth and innovation of the Asia-Pacific Lithium Cobalt Oxide Cathode Materials Market.

Rapid urbanization, rising disposable incomes, and technological adoption fueled demand for smartphones, laptops, and hybrid vehicles. Government initiatives to promote electric mobility and renewable energy storage further strengthened market growth. For instance, In June 2023, UC Irvine’s scientists announced the development of cobalt-free lithium-ion batteries. This discovery has the potential to address ethical concerns associated with cobalt mining, such as child labor, and reduce reliance on this mineral. Led by Professor Huolin Xin, the research team has devised a method that utilizes nickel as an alternative to cobalt in lithium-ion batteries.

Major LCO manufacturers invested in capacity expansion, R&D, and recycling facilities in the region. These factors collectively positioned Asia-Pacific as the fastest-growing and most influential market for lithium cobalt oxide cathode materials globally.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the LCO cathode materials market is marked by a mix of large multinational chemical and battery material companies and specialized regional producers. Key players compete on product quality, production capacity, and access to raw cobalt feedstock. Strategic initiatives include capacity expansion, partnerships with battery manufacturers, and investment in new technologies to improve energy density and sustainability. Asia Pacific firms, especially in China, hold dominant positions due to integrated supply chains and large consumer electronics sectors. Companies also pursue recycling initiatives to recover valuable cobalt. Technological differentiation and supply chain resilience are critical competitive factors as alternative cathode chemistries emerge.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the relentless demand for high-end consumer electronics, including smartphones, laptops, and tablets. Lithium Cobalt Oxide (LCO) remains the preferred cathode material for these devices due to its high energy density and superior discharge voltage, which are essential for maintaining long battery life in compact, portable hardware.

Q2. What are the main restraining factors for this market?

The market faces significant pressure from the high and volatile cost of cobalt, alongside ethical concerns regarding its mining. Furthermore, the automotive sector's shift toward Lithium Iron Phosphate (LFP) and Nickel Manganese Cobalt (NMC) chemistries limits LCO’s expansion, as these alternatives offer better thermal stability and lower costs.

Q3. Which segment is expected to witness high growth?

The High Purity LCO segment was expected to witness the highest growth over the forecast period due to increasing demand for premium lithium-ion batteries in consumer electronics, EVs, and specialized applications. Superior energy density, voltage stability, and long cycle life drove adoption, reinforcing its dominance in the global lithium cobalt oxide cathode market.

Q4. Who are the top major players for this market?

The market is dominated by major Asian chemical and battery material specialists. Key players include Shanshan Technology, Umicore, L&F Co., Ltd., and Xiamen Tungsten. These companies lead through advanced manufacturing processes, strategic vertical integration within the lithium supply chain, and long-term supply agreements with global tier-one battery cell manufacturers.

Q5. Which country is the largest player?

China is the largest player in the LCO cathode market, accounting for a massive share of both production and consumption. The country benefits from a robust domestic supply chain, the world’s largest consumer electronics manufacturing hub, and significant investments in cathode processing infrastructure, maintaining its status as the global leader.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model