Get Complete Analysis Of The Report - Download Updated Free Sample PDF

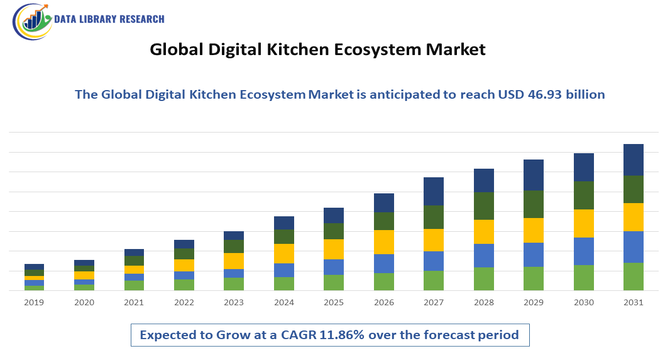

The Global Digital Kitchen Ecosystem Market refers to the integrated network of smart appliances, connected devices, software platforms, and cloud-based solutions that digitize and automate kitchen operations across residential and commercial environments. It includes IoT-enabled appliances, smart cooking systems, inventory management software, AI-powered recipe platforms, voice assistants, and food delivery integrations. The ecosystem enhances efficiency, convenience, personalization, and energy management through connectivity and data analytics. Growth is driven by smart home adoption, cloud kitchens, foodservice automation, and consumer demand for seamless digital experiences. This market bridges hardware, software, and services to create interconnected, intelligent kitchen environments globally.

The Global Digital Kitchen Ecosystem Market is witnessing rapid adoption of IoT-enabled appliances, AI-driven cooking assistants, and cloud-based kitchen management platforms. Integration with voice assistants and smart home ecosystems is becoming standard, enabling hands-free control and automation. Commercial kitchens are increasingly deploying digital order management, predictive inventory analytics, and robotics to improve operational efficiency. The rise of cloud kitchens and food delivery platforms is accelerating software-driven kitchen workflows. Sustainability trends are encouraging energy-efficient smart appliances with real-time monitoring capabilities. Additionally, data-driven personalization—such as tailored recipes and nutrition tracking—is reshaping consumer engagement, positioning digital kitchens as central components of modern connected living environments.

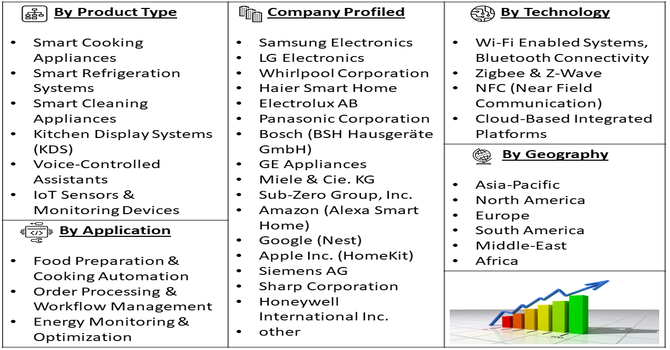

Segmentation: The Global Digital Kitchen Ecosystem Market is segmented by Component (Hardware (Smart Refrigerators, Smart Ovens & Cooktops, Smart Dishwashers, Connected Coffee Makers & Small Appliances and Kitchen Robotics & Automation Systems), Software (Kitchen Management Systems (KMS), Inventory & Order Management Software, Recipe & Nutrition Platforms and AI & Analytics Solutions), and Services (Installation & Integration, Maintenance & Support and Cloud & Subscription Services)), Product Type (Smart Cooking Appliances, Smart Refrigeration Systems, Smart Cleaning Appliances, Kitchen Display Systems (KDS), Voice-Controlled Assistants and IoT Sensors & Monitoring Devices), Connectivity Technology (Wi-Fi Enabled Systems, Bluetooth Connectivity, Zigbee & Z-Wave, NFC (Near Field Communication) and Cloud-Based Integrated Platforms), Application (Food Preparation & Cooking Automation, Order Processing & Workflow Management, Energy Monitoring & Optimization, Inventory & Supply Chain Management, Nutrition & Diet Management and Remote Monitoring & Predictive Maintenance), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing adoption of smart home technologies is a major driver of the Digital Kitchen Ecosystem Market. Consumers increasingly invest in connected appliances that integrate with centralized home automation systems. Smart refrigerators, ovens, dishwashers, and voice-controlled assistants enhance convenience, remote monitoring, and energy efficiency.

As internet penetration and smartphone usage expand globally, demand for interconnected kitchen devices rises. Manufacturers are embedding AI-powered features, predictive maintenance, and personalized cooking recommendations to enhance user engagement. For instance, in 2025 Samsung launched its Bespoke AI Refrigerator series in India, featuring advanced AI Energy Mode, Smart Forward integration, and enhanced freshness technologies. The launch accelerated smart appliance adoption, strengthened AI-driven kitchen ecosystems, and supported expansion of connected refrigeration solutions within the Global Digital Kitchen Ecosystem Market.

The shift toward connected living environments encourages ecosystem-based solutions rather than standalone products, fueling innovation and sustained growth in both developed and emerging markets.

The rapid expansion of cloud kitchens and online food delivery platforms significantly drives demand for digital kitchen ecosystems.

Commercial kitchens increasingly rely on integrated software for order processing, inventory management, analytics, and kitchen display systems to handle high-volume, multi-brand operations. For instance, in February 2025, Big Bowl launched its 200th cloud kitchen in Hyderabad under Lenexis Foodworks and expanded operations across 35 cities, targeting Tier II and Tier III markets. The expansion accelerated cloud kitchen growth, increased reliance on digital order management systems, and strengthened demand within the Global Digital Kitchen Ecosystem Market.

Automation reduces preparation errors and improves turnaround time, directly enhancing profitability. Data-driven insights enable operators to optimize menus, pricing, and supply chains. As urbanization accelerates and consumer preference shifts toward convenience dining, restaurants adopt digital systems to remain competitive. This transformation positions digital kitchen platforms as essential infrastructure for modern foodservice operations worldwide.

Market Restraints:

High implementation costs and cybersecurity concerns present significant restraints for the Digital Kitchen Ecosystem Market. Smart appliances and integrated management systems require substantial upfront investment, limiting adoption among small restaurants and price-sensitive households. Additionally, connected kitchens rely on cloud platforms and IoT networks, raising concerns about data privacy, hacking risks, and operational disruptions. Ensuring secure communication between devices and compliance with data protection regulations increases development costs for manufacturers. Interoperability challenges among different brands and ecosystems further complicate integration. These financial and technical barriers may slow widespread adoption, particularly in developing economies with limited digital infrastructure.

The Digital Kitchen Ecosystem Market significantly influences socioeconomic development by promoting automation, productivity, and digital transformation in households and foodservice industries. Smart kitchen technologies reduce food waste, optimize energy usage, and improve operational efficiency, contributing to sustainability goals. In commercial sectors, digital solutions create demand for skilled labor in software development, IoT engineering, and data analytics. Cloud kitchens and digital food platforms generate new entrepreneurial opportunities and employment in urban areas. Consumers benefit from convenience, time savings, and improved nutrition tracking. However, affordability gaps and digital literacy disparities may limit adoption in developing regions, creating uneven access to smart kitchen advancements.

Segmental Analysis:

The Smart Ovens & Cooktops segment is expected to witness the highest growth in the Global Digital Kitchen Ecosystem Market due to rising consumer demand for connected, energy-efficient, and automated cooking solutions. These appliances integrate Wi-Fi, AI-based temperature control, voice assistant compatibility, and remote monitoring through smartphone applications. Advanced features such as guided cooking, automatic shut-off, precision heating, and integration with smart home ecosystems enhance convenience and safety. Growing adoption of modular kitchens and premium appliances in urban households further drives demand. Additionally, commercial kitchens are increasingly investing in programmable smart cooking equipment to improve consistency, reduce labor costs, and enhance operational efficiency.

The Smart Cooking Appliances segment is projected to experience the highest growth due to increasing consumer preference for connected kitchen ecosystems and automated meal preparation. Products such as smart air fryers, pressure cookers, coffee machines, and multi-cookers are gaining traction for their convenience, app-based control, and personalized cooking settings. Integration with AI and cloud-based platforms enables recipe recommendations, nutritional tracking, and performance optimization. Busy lifestyles and rising disposable incomes encourage adoption of time-saving kitchen technologies. In commercial settings, programmable smart appliances enhance consistency and productivity. Continuous innovation in compact, multifunctional appliances further strengthens this segment’s rapid expansion globally.

The Bluetooth Connectivity segment is expected to witness the highest growth owing to its cost-effectiveness, ease of integration, and low power consumption compared to other connectivity technologies. Bluetooth-enabled kitchen devices allow seamless pairing with smartphones and tablets, enabling remote control, monitoring, and firmware updates without complex infrastructure. It is particularly suitable for small appliances and compact kitchens where stable, short-range communication is sufficient. Manufacturers favor Bluetooth for entry-level smart appliances targeting price-sensitive consumers. The growing popularity of app-controlled cooking tools and portable devices further accelerates adoption. Its compatibility with diverse smart home ecosystems supports steady growth during the forecast period.

The Food Preparation & Cooking Automation segment is anticipated to register the highest growth as automation transforms both residential and commercial kitchens. AI-driven cooking assistants, robotic chefs, automated ingredient dispensers, and precision cooking systems are increasingly adopted to reduce manual intervention and improve efficiency. Restaurants and cloud kitchens rely on automation to maintain consistency, minimize waste, and optimize turnaround times. In households, consumers seek smart systems that simplify meal planning and execution. Integration with voice commands, recipe databases, and inventory tracking further enhances functionality. Rising labor costs in the foodservice industry also encourage investment in automated cooking technologies globally.

The North American region is expected to witness the highest growth in the Global Digital Kitchen Ecosystem Market due to high smart home penetration, strong consumer purchasing power, and rapid adoption of connected appliances.

The presence of major technology providers and appliance manufacturers accelerates innovation and ecosystem integration. For instance, in January 2026, Aniai, a New York-based kitchen robotics company, developed automated grilling equipment for modern restaurants and commercial kitchens. Its solutions addressed labor shortages, improved cooking consistency, and increased throughput. The innovation accelerated kitchen automation adoption and supported efficiency-driven growth in the Global Digital Kitchen Ecosystem Market.

Growing popularity of cloud kitchens, online food delivery services, and AI-powered restaurant management systems further fuels demand. Consumers in the United States and Canada increasingly prioritize energy efficiency, convenience, and personalized cooking experiences. Supportive digital infrastructure and early adoption of IoT technologies position North America as a leading growth region globally.

To Learn More About This Report - Request a Free Sample Copy

The Global Digital Kitchen Ecosystem Market is highly competitive, featuring appliance manufacturers, technology companies, software developers, and food delivery platforms. Major smart appliance brands compete by integrating AI, IoT, and cloud connectivity into premium kitchen products. Technology giants expand ecosystems through voice assistants and smart home platforms. Software firms focus on digital kitchen management systems for restaurants and cloud kitchens. Strategic partnerships between hardware and software providers are common to ensure seamless interoperability. Mergers, acquisitions, and innovation in automation and robotics further intensify competition. Differentiation centers on connectivity, user experience, cybersecurity, sustainability features, and cross-platform compatibility within integrated smart environments.

The main players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

The primary growth driver is the global push for decarbonization, with governments tightening emission norms and increasing biofuel blending mandates (e.g., US RFS, EU RED III, Brazil's Future Fuel Law). This is accelerating investments in renewable diesel and sustainable aviation fuel production, which rely heavily on efficient catalysts. Additionally, technological advancements in second-generation biofuels and the rising demand for sustainable aviation fuel are fueling market expansion.

Q2. What are the main restraining factors for this market?

A key restraint is the high cost of catalyst materials, particularly precious metals like platinum and palladium, which impacts the economic viability of biofuels compared to fossil fuels. Catalyst deactivation due to impurities in feedstocks also leads to frequent replacements and increased operational costs. Furthermore, inconsistent regulatory frameworks across regions and supply chain constraints for raw materials create market uncertainty.

Q3. Which segment is expected to witness high growth?

The Smart Ovens & Cooktops segment is expected to witness the highest growth due to rising demand for connected, energy-efficient, and automated cooking solutions. Features such as remote control, AI-based temperature precision, voice assistant integration, and guided cooking enhance convenience, safety, and efficiency in both residential and commercial kitchens.

Q4. Who are the top major players for this market?

The global biofuels catalysts market is moderately fragmented with key players including global chemical and technology leaders. Major companies consistently identified include BASF SE, Evonik Industries, W.R. Grace, Honeywell, Solvay S.A., Clariant, DuPont, and Sinopec. These companies focus on developing high-performance catalysts for diverse feedstocks and applications to maintain competitive advantage.

Q5. Which country is the largest player?

The United States is identified as the leading country in the biofuel’s catalysts market, holding a significant share. North America, as a region, is the largest and fastest-growing market, driven by the EPA's Renewable Fuel Standard quotas and strong investments in advanced biofuel capacity. The Asia-Pacific region, particularly China, is also expected to see substantial growth.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model