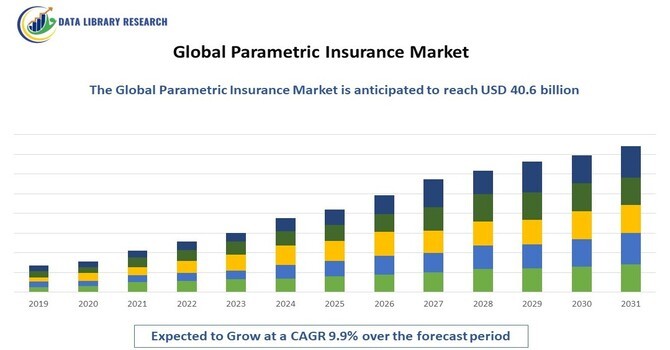

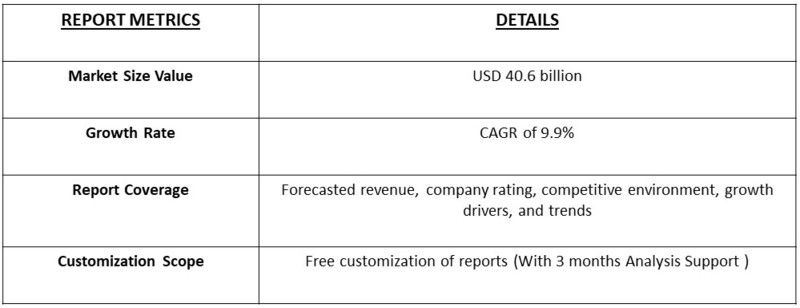

The global parametric insurance market was valued at approximately $15.8 billion in 2023 and is projected to reach $40.6 billion by 2033, growing at a compound annual growth rate (CAGR) of 9.9% over the forecast period.

Get Complete Analysis Of The Report - Download Free Sample PDF

The parametric insurance market provides coverage based on predefined triggers or parameters, such as specific weather conditions, natural disasters, or other measurable events, rather than traditional claims assessments. This type of insurance is gaining popularity in industries like agriculture, energy, and tourism due to its ability to offer rapid payouts and reduce administrative costs. Unlike conventional policies, parametric insurance uses data-driven indexes to determine compensation, making it highly efficient for scenarios involving climate risk and disaster recovery. The market's growth is fueled by increasing demand for faster, automated payout mechanisms and the rising frequency of catastrophic events.

One of the key drivers of the parametric insurance market is the increasing frequency and severity of natural disasters and climate-related events. These incidents have made traditional insurance models less efficient due to lengthy claim processes, prompting a shift towards parametric insurance for faster payouts. Additionally, technological advancements in data collection, such as satellite monitoring and IoT devices, enable precise measurement of triggers, enhancing the reliability of parametric models. The growing demand from sectors like agriculture, energy, and tourism, which face high exposure to climate risks, also supports market expansion. As businesses seek quicker financial recovery and operational resilience, the adoption of parametric insurance continues to accelerate.

The parametric insurance market include the growing use of advanced technologies like satellite imaging, AI, and blockchain to enhance data accuracy and streamline the claims process. These innovations enable insurers to offer more customizable, real-time policies with faster payouts. The market is also seeing increased demand from sectors like agriculture, construction, and energy, where climate risks are rising. Additionally, partnerships between insurers and technology firms are expanding to improve risk modeling and trigger mechanisms. As climate-related disasters intensify globally, the demand for parametric insurance is expected to continue growing, particularly in regions with high exposure to natural catastrophes.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Segmentation

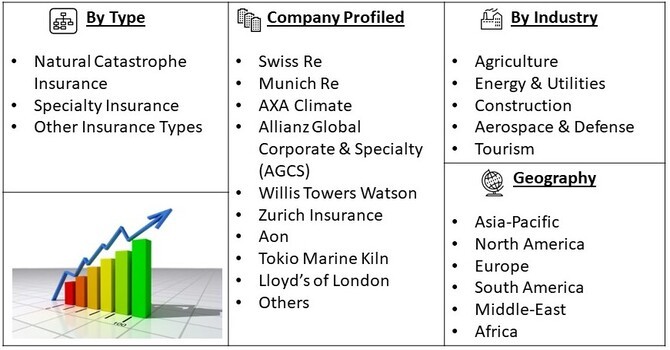

The Global parametric insurance market is segmented by type (Natural Catastrophe Insurance, Specialty Insurance, Other Insurance Types) By Industry Vertical (Agriculture, Energy & Utilities, Construction, Aerospace & Defense, Tourism) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

Market Drivers

The rising frequency and severity of climate-related events, such as floods, hurricanes, and wildfires, are major drivers for the parametric insurance market. According to real-time data, 2023 saw record-breaking heat waves and natural disasters, particularly in regions like North America and Asia-Pacific, pushing businesses and governments to seek quicker and more reliable payout solutions. Traditional insurance models, which often involve lengthy claims processes, have been inadequate in addressing the urgent needs of affected regions. Parametric insurance, with its predefined triggers and faster payouts, is becoming the preferred choice for industries like agriculture and energy that are heavily impacted by climate change. As governments push for greater climate resilience, especially in vulnerable areas, the demand for parametric insurance will continue to grow.

Advances in data collection technologies, such as satellite imaging, IoT sensors, and artificial intelligence, are accelerating the growth of the parametric insurance market. These technologies enable real-time monitoring of triggers like weather conditions, commodity prices, and seismic activity, allowing for highly accurate and transparent risk assessments. For instance, companies in the renewable energy sector are increasingly using parametric insurance to hedge against risks related to fluctuating wind speeds or solar irradiance. The use of these advanced technologies is also driving the adoption of parametric solutions across sectors such as agriculture, where precision data on rainfall or drought can determine rapid payouts. This has been particularly relevant in 2023, as technology-driven insurance models help reduce uncertainty and increase trust among policyholders.

Market Restraints

One of the major restraints for the parametric insurance market is the high cost of premiums, which can deter potential clients, especially in emerging markets. Parametric policies require substantial investment in advanced technologies such as satellite imaging and real-time data monitoring, which increases the overall cost of the insurance product. Furthermore, despite the clear benefits, there is still limited awareness and understanding of parametric insurance in certain industries and regions. For instance, small and medium-sized enterprises (SMEs) in Latin America and Africa often lack the financial resources and technical expertise to adopt these insurance solutions, which hampers market penetration. Additionally, regulatory frameworks in many regions are not yet fully adapted to support the rapid adoption of parametric insurance, further slowing down its growth.

The COVID-19 pandemic had a mixed impact on the parametric insurance market. On one hand, it slowed down the adoption of new policies in sectors like travel and tourism, which were heavily affected by the lockdowns and economic downturns. On the other hand, the pandemic highlighted the need for faster and more efficient insurance solutions, driving increased interest in parametric insurance for industries like agriculture and energy. The need for rapid financial recovery from pandemic-related disruptions prompted companies to explore parametric solutions, which offer quicker payouts compared to traditional models. The shift towards digitalization during the pandemic also accelerated the use of advanced technologies in parametric insurance, further boosting its appeal post-COVID.

Segmental Analysis

The agriculture insurance sub-segment in the parametric insurance market is seeing significant growth due to the increasing frequency of climate-related events like droughts, floods, and extreme temperatures. Real-time insights from 2023 show that many countries, especially in Asia-Pacific and Latin America, have faced crop failures due to unpredictable weather patterns, prompting farmers and governments to seek faster recovery solutions through parametric insurance. For instance, in India and Kenya, parametric policies tied to rainfall indexes have provided rapid payouts, helping farmers manage the risk of drought. The driving factors for this sub-segment include the rising need for food security, the impact of climate change on farming, and government initiatives to promote crop insurance. Technological advancements like satellite monitoring and IoT-enabled weather stations are also enhancing the accuracy and reliability of these parametric policies, making them more appealing to the agricultural sector.

Energy and utilities companies are increasingly adopting parametric insurance to mitigate risks associated with weather fluctuations that affect renewable energy generation, such as solar and wind. In 2023, several European renewable energy firms used parametric solutions to hedge against reduced energy output caused by lower-than-expected wind speeds. The demand in this sub-segment is driven by the global shift towards renewable energy and the increasing volatility in weather patterns due to climate change. Additionally, governments' focus on sustainable energy policies has led to a surge in renewable energy projects, amplifying the need for insurance products that can provide quick payouts based on weather-related triggers. The energy and utilities sector is also benefiting from technological advancements in weather forecasting and data analytics, which are improving the accuracy of parametric insurance models, making them a vital tool for managing operational risks.

The Asia-Pacific region is projected to witness significant growth in the parametric insurance market over the forecast period due to several factors. The region's high exposure to climate risks such as typhoons, floods, and earthquakes makes parametric insurance an attractive solution for faster recovery from natural disasters. Countries like China, Japan, India, and the Philippines are particularly vulnerable, and governments and businesses are increasingly adopting parametric insurance to mitigate these risks. The agricultural sector, a major contributor to the region’s economy, is also driving demand, as farmers look for ways to hedge against unpredictable weather patterns. Furthermore, advancements in satellite and data analytics technologies are making parametric insurance more accessible and reliable across the region. The Asia-Pacific market is expected to expand as insurers and technology firms collaborate to offer tailored products that meet the region’s unique needs.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the parametric insurance market is becoming increasingly dynamic as key players invest in technological innovations and expand their product portfolios. Leading insurers are focusing on developing data-driven solutions to enhance the accuracy and reliability of their parametric offerings.

Major players in this market include

Recent Development

Q1. What are the driving factors for the Global Parametric Insurance Market?

The global parametric insurance market is primarily driven by the increasing need for faster and more efficient claims processing. Traditional insurance models often involve lengthy assessments and negotiations, whereas parametric insurance pays out predefined amounts based on specific triggering events, such as natural disasters or weather conditions. This quick payout mechanism is appealing to businesses and individuals seeking immediate financial relief after an event. Additionally, the rising frequency and severity of climate-related disasters are prompting more organizations to seek innovative risk management solutions. The growing awareness of parametric insurance products among businesses, especially in agriculture, travel, and energy sectors, is further boosting market demand. As technology advances, the integration of big data and analytics is enhancing the precision of risk assessment and product offerings, making parametric insurance an increasingly attractive option.

Q2. What are the restraining factors for the Global Parametric Insurance market?

Despite its potential, the global parametric insurance market faces several restraining factors. One significant challenge is the limited understanding of parametric insurance products among consumers and businesses, leading to hesitancy in adoption. Many potential clients may prefer traditional insurance models due to their familiarity, even if parametric options offer faster payouts. Additionally, the market's reliance on accurate data for trigger events can create issues in terms of transparency and reliability. Inadequate data availability or inaccuracies can lead to disputes over payouts, undermining trust in the product. Regulatory challenges and varying acceptance across different jurisdictions can also pose hurdles for market growth. Lastly, competition from traditional insurance products, which may be perceived as more comprehensive, can limit the expansion of parametric insurance solutions.

Q3. Which segment is projected to hold the largest share of the Global Parametric Insurance market?

The agriculture segment is projected to hold the largest share of the global parametric insurance market. This is primarily due to the sector's vulnerability to climate risks, such as droughts, floods, and extreme weather conditions. Parametric insurance provides farmers with a safety net by offering payouts based on predefined weather indices, ensuring they receive timely financial support when adverse conditions occur. As agricultural practices become increasingly reliant on technology and data analytics, the accuracy and reliability of parametric insurance products in assessing risks are improving, further encouraging adoption. Moreover, governments and organizations are increasingly promoting parametric insurance solutions as a way to stabilize rural economies and support sustainable agricultural practices. This strong alignment with the agricultural sector's needs positions it as a key driver of growth in the parametric insurance market.

Q4. Which region holds the largest share of the Global Parametric Insurance market?

North America is expected to hold the largest share of the global parametric insurance market. The region benefits from a well-developed insurance infrastructure and a high level of awareness regarding innovative insurance solutions. The increasing frequency of natural disasters, such as hurricanes and wildfires, has heightened demand for parametric insurance as a quick and efficient risk management tool. Additionally, the presence of leading insurance companies and startups focusing on parametric products fosters a competitive environment that encourages innovation and market expansion. The agricultural sector in the U.S. and Canada also contributes significantly to the region's parametric insurance market, as farmers seek solutions to mitigate climate-related risks. With ongoing advancements in technology and data analytics, North America is well-positioned to maintain its dominance in the parametric insurance landscape.

Q5. Which are the prominent players in the Global Parametric Insurance market?

The global parametric insurance market features several prominent players known for their innovative approaches and market leadership. Swiss Re is a key player, offering a range of parametric insurance products tailored to various sectors, including agriculture and natural disaster coverage. Aon and Marsh & McLennan are also significant players, providing consulting and risk management services that incorporate parametric solutions for businesses. AXA and Zurich Insurance Group are recognized for their commitment to integrating parametric insurance into their product offerings, particularly in response to climate risks. Additionally, insurtech companies like Haven Life and Zego are disrupting the market with digital-first parametric solutions, appealing to a tech-savvy clientele. Through strategic partnerships and a focus on customer-centric products, these key players are shaping the future of the parametric insurance market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model