Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Respiratory DME Market encompasses long term medical equipment designed to support respiratory function in patients with chronic breathing disorders such as COPD (chronic obstructive pulmonary disease), asthma, sleep apnea, and respiratory failure. These devices include oxygen concentrators, ventilators, CPAP and BiPAP machines, nebulizers, masks, and other supportive respiratory tools used in hospitals, home care, and ambulatory settings. Demand is rising due to increasing prevalence of respiratory diseases, aging populations, and expanded home healthcare models. The market integrates technological advancements like smart connected devices and IoT capability that improve patient outcomes and enable remote monitoring.

The market trends include increased adoption of connected and smart respiratory devices featuring remote monitoring and telehealth integration that enhance patient adherence and provider oversight. The shift toward home based care continues as patients prefer non institutional treatment models, strengthened by lightweight portable oxygen concentrators and user friendly ventilators. IoT and cloud platforms are enabling real time data tracking for chronic respiratory conditions, improving clinical decisions and outcomes. Additionally, growing investments in healthcare infrastructure, reimbursement support in developed regions, and rising awareness of respiratory diseases drive adoption.

Segmentation: The Global Respiratory Durable Medical Equipment (DME) Market is segmented by Product Type (Oxygen Concentrators, Ventilators, Positive Airway Pressure (PAP) Devices, Nebulizers and Other Respiratory Equipment), Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep related Breathing Disorders (e.g., OSA), Acute Respiratory Failure and Other Respiratory Conditions), End User (Hospitals & Clinics, Home Healthcare, Ambulatory & Alternative Care Facilities and Sleep Labs & Diagnostic Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary drivers of this market is the increasing incidence of chronic respiratory diseases like COPD, asthma, and sleep apnea worldwide. For instance, WHO reported that in 2021, an estimated 260 million people globally suffered from asthma, a chronic respiratory condition affecting both children and adults. Similarly, in November 2025, Sanofi reported that Chronic obstructive pulmonary disease (COPD) is a devastating yet overlooked global health crisis, affected over 400 million people worldwide.

Aging populations, environmental pollution, smoking prevalence, and lifestyle changes contribute to rising disease burden, increasing demand for long term respiratory support equipment. Healthcare systems emphasize early diagnosis and sustained therapy to reduce hospitalizations and manage symptoms, translating to higher device utilization. Enhanced screening and patient awareness further boost demand. Therapeutic and monitoring devices such as oxygen concentrators, ventilators, and PAP systems remain critical components of chronic care strategies in both developed and emerging economies.

A significant market driver is the shift toward home based healthcare delivery and telemedicine, which encourages the use of respiratory DME outside traditional clinical environments. For instance, in November 2023, Pediatric Home Respiratory Services (PHS) acquired Apple Homecare Medical Supply, expanding its presence in Texas’ pediatric home medical equipment market. The acquisition strengthened home-based respiratory care delivery, enhanced access to pediatric DME, and supported the broader shift toward telemedicine and home healthcare adoption in the Respiratory Durable Medical Equipment market.

Patients with chronic respiratory conditions increasingly prefer at home treatment due to convenience, reduced costs, and enhanced quality of life. Digital integration with remote monitoring platforms enables clinicians to track adherence and adjust therapies without frequent in person visits, expanding home care adoption. Telehealth growth, especially accelerated by the COVID 19 pandemic, has emphasized remote disease management, fuelling demand for connected respiratory devices that support continuous monitoring, predictive analytics, and patient–provider communication.

Market Restraints:

A key restraint for the Respiratory DME Market is the high cost of advanced respiratory devices and inconsistent reimbursement frameworks across regions. Premium equipment like ventilators, oxygen concentrators, and advanced PAP systems can be expensive, limiting accessibility for patients in low and middle income countries. Complex and varying insurance reimbursement policies often require rigorous documentation and approvals, delaying patient access to necessary equipment. Limited reimbursement coverage may force patients to cover significant out of pocket costs, reducing adoption rates. These financial barriers also constrain manufacturer revenue potential and deter investment in innovative product development, especially for smaller companies seeking to enter the market.

The respiratory DME market has significant socioeconomic implications: it improves quality of life and independence for patients with chronic respiratory illnesses while reducing the burden on acute healthcare systems. Home use of respiratory support devices can decrease hospital admissions and long term care costs, contributing to cost effective healthcare delivery. By enabling early and sustained management of conditions such as COPD and sleep apnea, DME reduces complications and enhances workforce productivity. However, high device costs and variable reimbursement policies can limit access, especially in low and middle income areas, creating disparities in care. Investments in training, distribution, and affordability are needed to maximize health and economic benefits globally.

Segmental Analysis:

The oxygen concentrators segment is projected to experience the highest growth over the forecast period due to the rising prevalence of chronic respiratory conditions such as COPD, asthma, and pulmonary fibrosis. Portable and stationary concentrators provide continuous oxygen therapy, improving patient outcomes and enabling home-based care. Technological advancements like lightweight, energy-efficient, and battery-powered devices have increased patient mobility and comfort, boosting adoption. Enhanced reimbursement policies and growing awareness of oxygen therapy benefits further support market expansion. Both developed and emerging regions are witnessing rising demand as healthcare providers and patients prioritize long-term, non-invasive respiratory support solutions, driving consistent growth in the oxygen concentrators segment.

The COPD segment is anticipated to witness the highest growth due to the increasing global burden of the disease, fueled by aging populations, smoking, and environmental pollution. COPD patients require long-term respiratory support, including oxygen therapy, ventilators, and nebulizers, driving DME adoption. Improved diagnosis and screening programs have facilitated early intervention, increasing demand for home-based respiratory equipment. Healthcare providers are emphasizing disease management to reduce hospitalizations and improve quality of life, promoting consistent use of DME. Technological advancements in connected devices and remote monitoring also enhance therapy adherence. Consequently, the COPD segment remains a key growth driver in the global respiratory DME market.

The hospitals and clinics segment is expected to see the highest growth as these institutions remain the primary users of respiratory DME for acute and chronic care management. Hospitals rely on ventilators, PAP devices, oxygen concentrators, and nebulizers to treat respiratory failure, sleep apnea, and COPD. Growing patient volumes, rising prevalence of respiratory diseases, and technological upgrades in hospital equipment further fuel demand. Additionally, hospitals serve as distribution hubs for training patients and initiating home-based therapies. Increased government investments in healthcare infrastructure, particularly in developed regions, have enhanced accessibility and adoption, reinforcing hospitals and clinics as a dominant end-user segment.

North America is expected to lead the global respiratory DME market due to advanced healthcare infrastructure, high prevalence of chronic respiratory diseases, and strong patient awareness. Widespread insurance coverage and reimbursement policies facilitate access to oxygen concentrators, ventilators, PAP devices, and other DME.

Moreover, the technological innovations, such as smart connected devices and telemonitoring platforms, further drive adoption in home and clinical settings. For instance, in April 2024, Viemed Healthcare finalized a strategic partnership with East Alabama Health, acquiring controlling interest in East Alabama HomeMed. This expansion strengthened Viemed’s home medical equipment services, enhanced regional access to respiratory DME, and supported growth in North America’s home-based respiratory care market, boosting adoption and market penetration across eastern Alabama.

Also, the aging populations, rising obesity, and lifestyle-related respiratory risks contribute to sustained demand. Additionally, government initiatives, clinical guidelines, and large-scale home healthcare programs support market expansion. Collectively, these factors position North America as the highest growth region for respiratory DME over the forecast period.

| Report Matrics | Details |

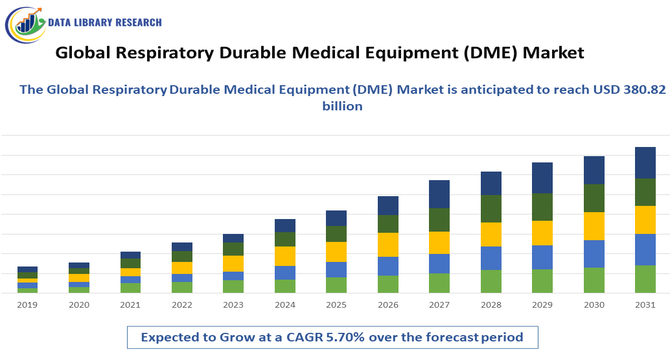

| Market Size Value | USD 380.82 billion |

| Growth Rate | CAGR of 5.70% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Respiratory DME Market is moderately consolidated, dominated by global manufacturers focusing on innovation, technology integration, and geographical expansion. Leading players emphasize R&D to improve connectivity, usability, and performance of respiratory equipment. Strategic alliances, acquisitions, and partnerships with healthcare providers and distributors strengthen market positioning and expand product portfolios. Established brands benefit from extensive distribution networks, regulatory compliance expertise, and strong brand equity, making them key suppliers to hospitals and home care providers. Competitive differentiation increasingly centers on value added services like remote monitoring, telehealth integration, and service support, while regional players offer cost competitive solutions, especially in emerging markets.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Market expansion is fuelled by the rising global incidence of chronic respiratory diseases, such as COPD and asthma, alongside an aging population. Technological leaps in portable and smart devices—like compact oxygen concentrators and AI-enabled monitoring—are increasing patient independence. Additionally, the growing preference for home-based healthcare significantly boosts equipment demand.

Q2. What are the main restraining factors for this market?

Growth is primarily limited by the high cost of advanced respiratory equipment and inconsistencies in healthcare reimbursement across different regions. Regulatory hurdles and lengthy approval processes can delay the introduction of innovative products. Furthermore, a global shortage of specialized technicians to maintain and calibrate complex DME can hinder market penetration.

Q3. Which segment is expected to witness high growth?

The Home Healthcare segment is witnessing the highest growth as patients shift from hospitals to home settings for long-term care. Product-wise, Portable Oxygen Concentrators (POCs) and smart nebulizers are expanding rapidly. Geographically, the Asia-Pacific region is the fastest-growing market due to increasing pollution levels and healthcare infrastructure investments.

Q4. Who are the top major players for this market?

The market is dominated by global leaders in respiratory technology, including ResMed, Koninklijke Philips N.V., and Medtronic. Other key participants driving the industry through innovation and extensive distribution networks include Fisher & Paykel Healthcare, Invacare Corporation, Drive DeVilbiss Healthcare, and GE HealthCare.

Q5. Which country is the largest player?

The United States is the largest player, commanding the highest share of global revenue. Its dominance is supported by a high prevalence of respiratory conditions, a mature Medicare and Medicaid reimbursement system, and early adoption of "connected" medical technology. The presence of major industry headquarters further cements its leading position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model