Get Complete Analysis Of The Report - Download Updated Free Sample PDF

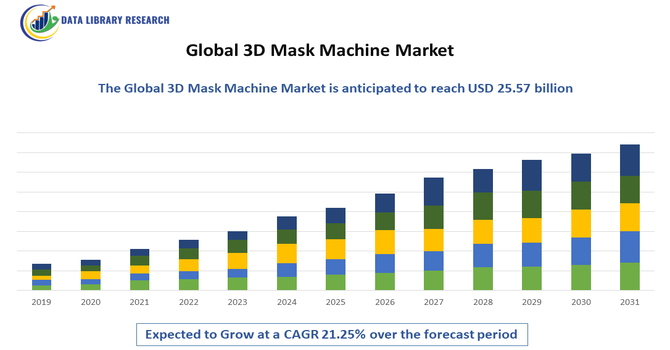

The Global 3D Mask Machine Market refers to the international industry involved in the production, development, and distribution of automated machinery designed to manufacture three-dimensional (3D) face masks, often used in medical, industrial, and consumer applications. These machines are equipped with advanced technologies like ultrasonic welding, high-speed cutting, and automated folding to create ergonomically shaped masks that fit the contours of the human face more effectively than traditional flat masks. The market is driven by rising demand for high-efficiency protective masks due to increasing health awareness, air pollution concerns, and pandemic preparedness, with significant growth observed across regions such as Asia-Pacific, North America, and Europe.

The 3D mask machine market is seeing strong momentum driven by heightened health & safety awareness post COVID, which fuels demand for better protective equipment and personalized fit. Automation and advanced manufacturing technologies—such as 3D printing, additive production, machine vision, and AI enabled design—are becoming more integrated, enabling higher throughput, precision, and lower wastage. Sustainability is emerging as a major trend, with manufacturers seeking eco friendly, biodegradable, or reusable materials, and optimizing production to reduce environmental impact.

Segmentation: The Global 3D Mask Machine Market can be segmented by Product (Below ~100 masks per minute machines, 100 200 masks/min machines, 200 300 masks/min machines and Others (higher capacity, custom), Application (Medical / Healthcare Products, Labor, Consumer and Other Applications), Technology (Fully Automatic 3D Mask Machines, Semi Automatic 3D Mask Machines, Manual or less automated variants and Other Technologies), Material (Thermoplastic polymers, Elastomers or flexible materials and Biodegradable / eco friendly materials), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The strongest drivers of the 3D mask machine market is the increasing need for high-quality, comfortable face masks, especially in healthcare and industrial settings. Unlike flat surgical masks, 3D masks offer a better fit, improved filtration, and reduced leakage—making them ideal for doctors, nurses, factory workers, and people in high-risk environments. The COVID-19 pandemic made everyone more aware of the importance of effective protective equipment, and that awareness hasn’t faded. Hospitals, manufacturing units, and even consumers now want masks that provide better protection and long-term comfort. As a result, demand for machines that can mass-produce these advanced, form-fitting masks has grown significantly across both developed and developing regions.

Technological progress in automation and smart manufacturing is significantly boosting the 3D mask machine market. Today’s machines are no longer just mechanical—they’re equipped with AI, robotics, and computer vision systems to improve speed, accuracy, and consistency. This makes it easier and more cost-effective for manufacturers to produce large volumes of masks without compromising on quality. Features like automatic material feeding, ultrasonic welding, and real-time defect detection have become common, reducing human error and labor costs. These innovations make it possible for both large and small businesses to enter the mask production space, creating more demand for smart 3D mask machines. In short, better tech is making mask production faster, easier, and more profitable.

Market Restraints:

A major restraint for the Global 3D Mask Machine Market is the high upfront cost and technical complexity involved in purchasing and operating these machines. Fully automated 3D mask machines can be expensive, often requiring significant capital investment—not just for the equipment itself, but also for setting up supporting infrastructure like clean rooms, skilled labor, and quality control systems. Additionally, many small and medium enterprises (SMEs) lack the technical know-how to operate or maintain these machines, which often integrate advanced technologies like ultrasonic welding and programmable logic controllers (PLCs). This creates a barrier to entry, especially in developing economies where budget constraints and limited access to skilled technicians can slow market adoption and expansion.

The Global 3D Mask Machine Market exerts a significant socio-economic impact, primarily by boosting public health resilience and democratizing the manufacturing of essential personal protective equipment (PPE). Economically, the market drives innovation in additive manufacturing, creating high-skilled jobs in design, operation, and maintenance, while potentially shortening global supply chains by enabling decentralized, on-demand, and localized production. This speed and flexibility were critical during public health crises, allowing communities and hospitals to rapidly produce customized masks and components, thereby mitigating supply shortages and reducing the strain on conventional manufacturing and logistics. Socially, the technology enhances healthcare access by providing quicker and more tailored protective gear, though its high initial cost and the need for standardized quality certification present challenges to widespread adoption, particularly in developing economies.

Segmental Analysis:

The 100–200 masks per minute segment is projected to experience strong growth due to its ideal balance between production speed and operational efficiency. These machines are well-suited for mid-sized manufacturers looking to scale their output without investing in ultra-high-speed models, which often come with much higher costs and maintenance demands. As demand for 3D masks grows steadily in both medical and consumer sectors, this segment offers a flexible and cost-effective option. Additionally, these machines often come with semi-automatic or partially automated features, making them easier to operate in regions with moderate technical expertise. Their ability to deliver high output while maintaining reasonable energy and labor requirements makes them increasingly attractive in emerging markets across Asia-Pacific and Latin America.

The medical and healthcare products segment is expected to lead the growth in the 3D mask machine market due to the increasing demand for high-protection and ergonomic face masks in hospitals, clinics, and other care settings. Post-COVID, there has been a global shift toward higher safety standards and more effective personal protective equipment (PPE), especially for frontline workers. 3D masks are preferred in healthcare environments because they provide a closer facial fit and superior filtration efficiency, minimizing leakage and exposure risks. With many hospitals and medical device companies seeking to produce their own masks for better quality control and supply stability, the demand for advanced 3D mask machines tailored to medical standards is rising rapidly, particularly in North America, Europe, and parts of Asia.

Semi-automatic 3D mask machines are gaining popularity, especially among small and medium enterprises (SMEs) and startups, due to their lower capital requirements and operational flexibility. These machines strike a practical balance between manual and fully automated production, allowing operators to manage part of the process while still benefiting from automation in critical steps like ultrasonic welding and shaping. As more businesses enter the protective mask market—especially in developing regions—semi-automatic machines offer an accessible way to start production without needing a large, skilled workforce. Their relatively easy maintenance and lower energy consumption also make them suitable for regions with limited industrial infrastructure. The segment’s growth is supported by rising local manufacturing initiatives and government support for PPE production capacity building.

The North American region is projected to experience significant growth in the 3D mask machine market due to strong healthcare infrastructure, rising demand for high-quality PPE, and increasing investment in domestic manufacturing. The COVID-19 pandemic exposed the vulnerabilities of global supply chains, prompting the U.S. and Canada to prioritize local production of essential medical supplies, including face masks.

Government initiatives and funding for PPE manufacturing, along with stricter workplace safety regulations, are driving demand for advanced 3D mask machines across healthcare, industrial, and commercial sectors. For instance, in July 2025, an article titled, “A comparative anthropometric analysis of U.S. female firefighters versus the general female population” reported that that female firefighters in the U.S. have distinct body measurements compared to the general female population, highlighting the need for specialized PPE sizing. For the U.S. 3D mask machine market, this drives demand for customized, well-fitting protective gear. Using 3D scanning and precise anthropometric data enables manufacturers to produce better-fitting masks, boosting market growth through tailored 3D mask solutions.

Additionally, the region’s focus on automation and adoption of smart manufacturing technologies aligns well with the latest features offered by modern mask machines, making North America a key growth hub over the forecast period. For instance, in June 2024, Rockwell Automation, Inc., released its 10th annual "State of Smart Manufacturing Report: Life Sciences Edition," based on insights from 143 industry leaders across 15 top manufacturing countries. This development underscores North America's strong emphasis on automation and smart manufacturing technologies, which perfectly complements the advanced capabilities of modern mask machines. As a result, North America is well-positioned to become a major growth hub for the 3D mask machine market throughout the forecast period, driven by the integration of cutting-edge automation and digital innovations in manufacturing processes.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global 3D Mask Machine Market is characterized by the presence of a mix of established machinery manufacturers and emerging players, primarily concentrated in Asia-Pacific, especially China, South Korea, and Japan. Key players compete on factors such as machine speed, automation level, pricing, customization, and after-sales service. Companies are increasingly focusing on innovation—integrating technologies like AI, IoT, and computer vision to enhance machine precision and efficiency. Strategic partnerships, expansion into new geographies, and investment in R&D are common approaches to gaining market share. Additionally, with rising global demand, many regional players are scaling up production and enhancing export capabilities to meet international standards, intensifying competition in both price-sensitive and premium market segments.

The 20 major players for above market are:

Recent Development:

Q1. What the main growth driving factors for this market?

The main growth driving factors for the 3D Mask Machine Market include the unprecedented surge in global demand for Personal Protective Equipment (PPE) like face masks, particularly following the COVID-19 pandemic. This is coupled with ongoing advancements in additive manufacturing technologies, such as improved speed, materials, and automation, which enable the efficient, high-volume production of masks. Furthermore, the increasing adoption of 3D printing across various industries, especially healthcare, and growing governmental support for decentralized and customized PPE production significantly propel the market forward.

Q2. What are the main restraining factors for this market?

Key restraining factors primarily revolve around cost and standardization challenges. The relatively high manufacturing cost of 3D-printed masks, especially the raw materials, can hinder widespread adoption among smaller enterprises. Additionally, there has been a documented lack of standardized testing methods and regulatory clarity for 3D-printed medical masks, which raises serious concerns regarding their protective capacity and effectiveness compared to traditional, certified PPE, thereby limiting their acceptance.

Q3. Which segment is expected to witness high growth?

Within the broader 3D mask production landscape, the segment for N95/KN95/FFP2 Mask Production Equipment is expected to witness significantly high growth. This is driven by the sustained demand for high-filtration respirators in both medical and industrial settings to protect against airborne diseases and particles. Furthermore, the increasing need for high-volume, automated production to ensure supply chain resilience and meet rising industrial safety mandates will continue to boost this specialized machine segment.

Q4. Who are the top major players for this market?

The top major players in this market are often leading companies from the broader 3D printing and industrial automation sectors who manufacture the specialized equipment. Key players include large, established firms like Stratasys, 3D Systems, EOS, HP, and General Electric (GE Additive). These companies leverage their expertise in additive manufacturing technology, materials science, and industrial-scale production systems to offer solutions for fabricating both customized and high-volume protective mask components.

Q5. Which country is the largest player?

The Asia-Pacific region, primarily driven by countries like China, Japan, and South Korea, holds the largest share in the related overall face mask and 3D printing markets and is a dominant manufacturing hub for 3D mask machines. This dominance is due to rapid industrialization, the strong presence of major electronics and semiconductor manufacturing, and significant investment in adopting advanced additive manufacturing technologies to boost their healthcare and industrial production capacity.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model