Get Complete Analysis Of The Report - Download Updated Free Sample PDF

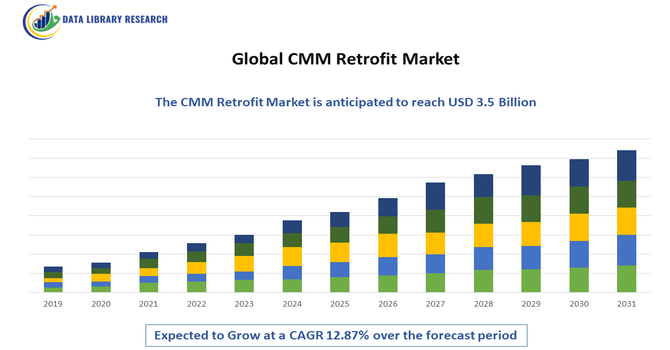

The Global Coordinate Measuring Machine (CMM) Retrofit Market is experiencing steady growth as industries increasingly shift toward modernizing legacy inspection systems rather than replacing them with new, high-cost machines. CMM retrofitting involves upgrading existing CMMs with advanced controllers, sensors, probes, and software to enhance accuracy, automation capabilities, and connectivity. This approach aligns with Industry 4.0 initiatives, where smart metrology, real-time data analytics, and digital twins are becoming essential for precision manufacturing. The market is driven primarily by the rising demand for improved dimensional inspection performance across sectors such as automotive, aerospace, medical devices, electronics, and heavy machinery, where quality assurance is mission-critical.

The Global CMM Retrofit Market is witnessing notable advancements driven by digital transformation and the rising adoption of Industry 4.0 practices across manufacturing environments. One of the most significant trends is the integration of IoT-enabled controllers and smart interfaces that allow retrofitted CMMs to seamlessly communicate with factory automation systems, cloud platforms, and predictive maintenance tools. Another growing trend is the shift toward multisensor and non-contact metrology solutions, including laser scanners and optical probes, which enable upgraded machines to perform faster, more complex, and high-resolution measurements suitable for advanced materials and complex geometries.

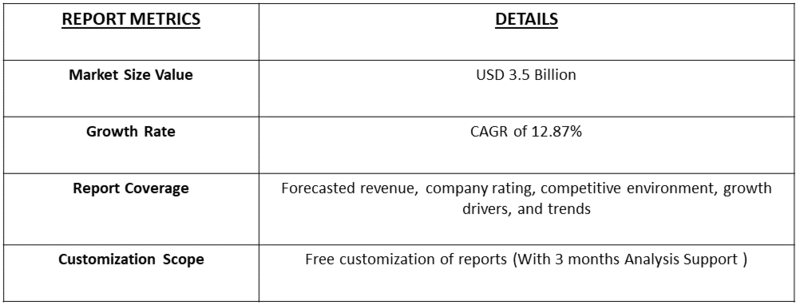

Segmentation: Global CMM Retrofit Market is segmented By Component (Controller Upgrades, Probing Systems, Optical & Laser Scanner Retrofits, Software Upgrades, Encoder Replacements, Measurement Sensors), Type of CMM (Bridge CMM, Gantry CMM, Horizontal Arm CMM, Cantilever CMM), Offering (Hardware Retrofit Solutions, Software Retrofit Solutions, Calibration & Verification Services, Training & Technical Support), Application (Dimensional Inspection, CAD-to-Part Validation, Reverse Engineering, Automated Inline), End-User Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, Medical Devices, Industrial Machinery & Heavy Engineering), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

One of the primary drivers of the Global CMM Retrofit Market is the rising global emphasis on precision manufacturing and stringent quality assurance standards across key industries such as automotive, aerospace, medical devices, and semiconductor fabrication.

As manufacturing tolerances become increasingly tighter due to the complexity of modern engineered components—such as EV drivetrain parts, turbine blades, implants, and microelectronics—existing legacy CMMs often lack the accuracy, speed, and measurement flexibility required to meet updated GD&T frameworks and regulatory compliance demands. Retrofitting provides a cost-effective pathway to upgrade older CMMs with advanced scanning systems, multisensor capabilities, updated metrology software, and automated workflows that support higher repeatability and measurement consistency.

Another significant growth driver is the increasing focus on cost optimization and sustainability, motivating industries to extend the operational life of existing CMMs instead of replacing them entirely. Thousands of CMMs installed globally over the past decades remain mechanically sound but technologically outdated.

Retrofitting allows organizations to modernize these machines with next-generation hardware, controllers, laser scanners, and software platforms at a fraction of the cost of new equipment—often between 30–50% of the replacement price. In addition to cost savings, retrofits reduce downtime, streamline maintenance, and enhance compatibility with Industry 4.0-enabled data systems, enabling manufacturers to transition toward smart metrology ecosystems without operational disruptions. This retrofit-first strategy aligns with CAPEX reduction initiatives and circular manufacturing trends, making it a preferred upgrade path for small to large-scale manufacturers.

Market Restraints:

The one major restraint is the technical complexity and compatibility challenges associated with retrofitting older CMMs, especially those with obsolete mechanical structures, proprietary control systems, or limited integration support for modern scanning or software solutions. In many cases, retrofitting may require extensive customization or redesign efforts, which can increase project time and cost, making new CMM purchases more appealing for some manufacturers. Additionally, variability in legacy system conditions—such as worn mechanical guides, outdated air bearings, or poor machine calibration—can reduce retrofit feasibility or measurement reliability, thereby affecting end-user confidence.

The global CMM (Coordinate Measuring Machine) retrofit market has a notable socioeconomic impact by helping manufacturers extend the life and improve the accuracy of existing measurement equipment. By upgrading older CMMs with modern software and sensors, companies reduce costs, minimize waste, and enhance product quality, which boosts industrial productivity and competitiveness. This retrofitting also creates demand for skilled technicians and engineers, supporting employment and workforce development. Additionally, by enabling more precise manufacturing and quality control, the market contributes to safer products, sustainable production practices, and economic growth across multiple industries worldwide.

Segmental Analysis:

The component segment, controller upgrades account for a major share due to the growing need to replace outdated control units that lack compatibility with modern scanning probes, advanced metrology software, and automated inspection workflows. Upgraded controllers significantly improve system response time, measurement precision, and data communication capabilities, making them a key focus for industries aiming to integrate their legacy CMMs into Industry 4.0-enabled production lines.

The types of CMMs, bridge CMM systems dominate the retrofit market as they represent the largest installed base worldwide in sectors such as automotive and aerospace manufacturing. Their stable structure and long operational lifespan make them highly suitable for retrofit upgrades, enabling manufacturers to achieve improved inspection capability and extended equipment life without the cost burden of purchasing new machines.

Dimensional inspection holds the largest share due to its critical role in quality assurance, manufacturing validation, and regulatory compliance. Retrofitted CMMs support higher accuracy, automation, and repeatability in inspection processes, which is essential for precision-driven industries where deviations from tolerances directly affect product performance and safety.

The automotive industry represents the largest end-user segment driven by high-volume precision measurement requirements for powertrain systems, EV components, metal stamping, molds, and assemblies. Increasing model complexity, shorter design cycles, and demand for automated inspection systems continue to accelerate retrofit adoption across automotive manufacturing and supplier networks.

The North America region is expected to witness the highest growth over the forecast period, driven by the strong presence of advanced manufacturing industries, rapid adoption of Industry 4.0 technologies, and the increasing need to modernize legacy metrology infrastructure. The region’s automotive, aerospace, defense, and medical device sectors are placing greater emphasis on precision inspection, automation, and digital quality control systems, which is accelerating investment in CMM retrofit solutions.

Additionally, the availability of leading retrofit technology providers, strong regulatory compliance frameworks, and growing focus on cost optimization and operational efficiency are further supporting market expansion in North America. For instance, in June 2025, Capvidia, announced full integration support for the latest Siemens NX software release. This advancement enhanced the implementation of Model-Based Characteristics (MBC) through the QIF standard, strengthening the digital thread from design to quality and manufacturing across OEMs and global supply chains. It positively impacted the U.S. CMM retrofit market by promoting seamless modernization, improving measurement accuracy, and facilitating efficient digital workflows for manufacturing and inspection processes.

Thus, such factors together are driving this market’s growth in this region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global CMM Retrofit Market is moderately consolidated, with leading metrology OEMs and specialized retrofit service providers competing on technology capability, software compatibility, and service reliability. Companies focus on offering advanced retrofit solutions featuring laser scanning, multisensor systems, and Industry 4.0 connectivity to modernize legacy CMMs. Competitive advantages are driven by strong aftermarket service networks, calibration and training support, and cost-efficient upgrade packages. As demand grows across manufacturing industries, partnerships and technology innovation continue to shape market competition.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the significant cost advantage of upgrading an existing Coordinate Measuring Machine (CMM) over purchasing a brand new unit. This cost-effectiveness appeals strongly to manufacturers. Furthermore, the global push toward industrial automation and Industry 4.0 demands higher measurement accuracy and faster inspection times, making retrofitting with modern controllers and advanced probes a pragmatic solution for improved quality assurance.

Q2. What are the main restraining factors for this market?

The main restraints are related to complexity and investment. Although retrofitting is cheaper than buying new, the systems still require significant capital outlay for advanced hardware and software components. A second major challenge is the lack of a sufficient skilled workforce. Operating and maintaining these sophisticated machines requires specialized metrology expertise, creating a bottleneck for widespread adoption across all manufacturing facilities.

Q3. Which segment is expected to witness high growth?

The Asia Pacific (APAC) region is projected to witness the highest future growth potential, driven by rapid and massive industrialization, especially in countries like China and India. This regional expansion is fueled by increasing foreign investment and government initiatives that prioritize quality control and the adoption of smart manufacturing principles across critical sectors like automotive and electronics.

Q4. Who are the top major players for this market?

The CMM retrofit market is dominated by a few key global companies that specialize in high-precision metrology solutions. The top major players include Hexagon AB, which often holds the leading market share, the ZEISS Group, FARO Technologies, and Mitutoyo Corporation. These dominant providers supply the comprehensive hardware and software upgrades needed to modernize and enhance the performance of older CMMs.

Q5. Which country is the largest player?

The United States, acting as the major economic engine within the North America region, is considered the largest established market for CMM retrofitting services by current revenue share. This dominance stems from its highly mature and technologically advanced manufacturing base, particularly in regulated industries like aerospace and defense, which mandate the highest levels of measurement precision and quality control.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model