Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global fanless industrial control computer market covers rugged, passively cooled computing systems designed for harsh environments. These compact, reliable units support automation, monitoring, and real-time control across manufacturing, energy, transportation, and IoT applications, emphasizing durability, low maintenance, thermal efficiency, and consistent performance in challenging industrial conditions around the world.

Growth of the global fanless industrial control computer market is driven by rising automation across manufacturing and process industries, increasing demand for rugged, maintenance-free systems, expanding use of IoT and edge computing, stricter reliability and safety requirements, growth in smart factories, and the need for energy-efficient, thermally stable computing in harsh industrial environments.

The global fanless industrial control computer market is witnessing strong growth due to rising industrial automation and the widespread adoption of Industry 4.0 technologies. Manufacturers are shifting toward rugged, compact, and maintenance-free systems that perform reliably in harsh environments with dust, vibration, and extreme temperatures. The expansion of IIoT and edge computing is increasing demand for fanless units that can process data locally and support real-time decision-making.

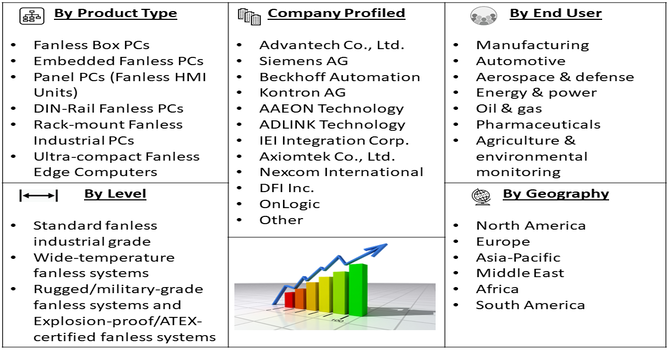

Segmentation: The Global Fanless Industrial Control Computer Market is segmented by Type (Fanless Box PCs, Embedded Fanless PCs, Panel PCs (Fanless HMI Units), DIN-Rail Fanless PCs, Rack-mount Fanless Industrial PCs, Ultra-compact Fanless Edge Computers), Processor Type (x86-based (Intel, AMD), ARM-based, and RISC-based industrial processors), Cooling & Ruggedization Level (Standard fanless industrial grade, Wide-temperature fanless systems, Rugged/military-grade fanless systems and Explosion-proof/ATEX-certified fanless systems), Storage Type (SSD-based fanless systems, eMMC/embedded storage and Hybrid storage systems), End-Use Industry (Manufacturing, Automotive, Aerospace & defense, Energy & power, Oil & gas, Pharmaceuticals, Agriculture & environmental monitoring and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global fanless industrial control computer market is significantly driven by rapid industrial automation and the widespread implementation of Industry 4.0 technologies. As factories transition to smart manufacturing, demand increases for rugged, reliable, and maintenance-free computing solutions that support continuous operation.

Fanless systems offer high durability in environments with dust, shock, vibration, and extreme temperatures, making them ideal for automation equipment, robotics, and real-time monitoring. Their ability to integrate with sensors, PLCs, and industrial networks enables seamless data flow and operational efficiency. This accelerating shift toward digitized and intelligent production processes continues to propel strong market growth worldwide.

Another major growth driver is the expanding use of Industrial Internet of Things (IIoT) devices and the rising adoption of edge computing across industrial sectors. Fanless industrial computers provide localized data processing, reduced latency, and real-time analytics, which are essential for predictive maintenance, quality control, and smart asset management.

In March 2025, ASUS IoT partnered with ACTE to launch the Configure-to-Order Service (CTOS) in the Nordics, enabling tailored industrial computing solutions. This enhanced flexibility supported edge computing and IIoT adoption, driving growth in industrial automation, healthcare, retail, transportation, and the fanless control computer market. As organizations seek to enhance efficiency by moving computation closer to the source, fanless edge devices become critical for decentralized control architectures. This trend is especially strong in manufacturing, energy, transportation, and remote operations.

Market Restraints:

Despite strong demand, the market faces restraints related to the high upfront cost of fanless industrial control systems and the complexities involved in integrating them into existing infrastructure. Ruggedized components, wide-temperature hardware, and industrial-grade certifications increase production costs, making these systems more expensive than conventional PCs. Additionally, many industries operate with legacy equipment and communication protocols, requiring customization, engineering resources, or additional interface modules. This can lengthen deployment timelines and raise implementation costs. For small and mid-size enterprises, these financial and technical barriers can slow adoption, despite long-term benefits in reliability, maintenance reduction, and operational efficiency.

The adoption of fanless industrial control computers contributes to higher productivity, improved operational safety, and more efficient resource utilization across industries. By enabling automation and real-time monitoring, these systems help reduce downtime, enhance product quality, and lower operating costs, strengthening industrial competitiveness. While automation may shift certain manual roles, it also creates new opportunities in technical fields such as systems integration, robotics, and data analytics. Energy-efficient, low-maintenance designs support sustainability goals by reducing power consumption and waste.

Segmental Analysis:

Panel PCs with fanless HMI capabilities are expected to witness the highest growth due to increasing adoption of interactive, touchscreen-based interfaces across industrial environments. These systems combine display, processing, and control functions in a sealed, rugged design ideal for dusty or moisture-prone settings. As factories modernize, operators require intuitive HMIs for real-time visualization, equipment control, and data access on production floors. The demand for hygienic, easy-to-clean units is rising in food, pharmaceuticals, and electronics manufacturing. Additionally, integration with automation software, IIoT platforms, and edge computing solutions positions fanless Panel PCs as essential components of next-generation smart factory infrastructures.

The ARM-based segment is expected to grow rapidly due to increasing interest in energy-efficient, compact, and cost-effective industrial computing architectures. ARM processors offer low heat generation, making them ideal for fanless designs that operate reliably in constrained or harsh environments. Their expanding ecosystem, improved performance, and compatibility with Linux-based industrial operating systems enhance their appeal for edge computing, IoT applications, and embedded automation tasks. Industries increasingly seek lightweight systems that support real-time control while minimizing power consumption. With ARM architectures advancing into higher-performance tiers and supporting AI workloads, their adoption in industrial control is accelerating, driving strong segment growth.

SSD-based fanless systems are projected to experience the highest growth as industries prioritize reliability, speed, and resilience in mission-critical operations. Solid-state drives offer superior durability compared to HDDs, with no moving parts, reduced vibration sensitivity, and longer operational life—qualities essential for industrial environments. Their faster boot times, improved data throughput, and lower power consumption support real-time monitoring, analytics, and edge computing functions. As data volumes increase and industrial networks expand, SSD-based storage ensures stable performance and minimal downtime. The rising adoption of predictive maintenance and high-speed control applications further strengthens demand for SSD-equipped fanless systems across sectors.

The manufacturing sector is expected to see the highest growth as global industries accelerate digital transformation, automation, and smart factory initiatives. Fanless industrial computers support robotics, machine vision, quality inspection, predictive maintenance, and real-time production monitoring, making them central to modern manufacturing workflows. Their rugged, maintenance-free design ensures uninterrupted operation in environments exposed to dust, vibration, and temperature fluctuations. As manufacturers adopt IIoT devices, edge analytics, and human-machine interfaces, demand for reliable computing platforms increases significantly. The shift toward mass customization, flexible production lines, and energy-efficient operations further drives the adoption of fanless control systems across diverse manufacturing sub-sectors.

The Asia-Pacific region is expected to witness the highest growth due to rapid industrialization, strong manufacturing bases, and expanding investments in automation technologies. Countries like China, Japan, South Korea, and India are adopting smart manufacturing, robotics, and IIoT solutions at a fast pace, driving demand for rugged fanless control computers.

The region’s growth in electronics, automotive, semiconductors, and energy sectors further boosts adoption. For instance, in September 2025, BIOSTAR launched the EdgeComp MU-N150, a compact 0.6L fanless industrial PC with Intel N150 “Twin Lake” SoC, offering industrial-grade durability. It supported edge computing, automation, and HMI applications, boosting IIoT adoption and driving fanless industrial PC growth in Asia-Pacific.

Furthermore, the government initiatives promoting digital transformation, industrial modernization, and local production of automation equipment enhance market momentum. Additionally, the proliferation of small and medium enterprises adopting cost-effective automation solutions positions Asia-Pacific as the fastest-expanding regional market.

| Report Matrics | Details |

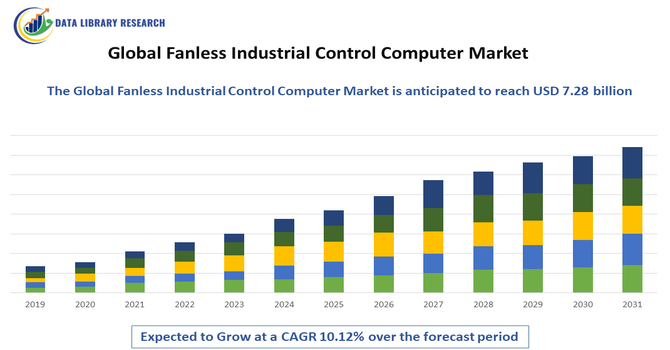

| Market Size Value | USD 7.28 billion |

| Growth Rate | CAGR of 13.5% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape is characterized by a mix of global industrial computer manufacturers and specialized solution providers offering a wide range of fanless systems tailored for demanding environments. Companies compete on durability, thermal efficiency, customization options, and support for advanced functions such as AI processing, wireless connectivity, and edge analytics. Product innovation focuses on modular designs, broader temperature tolerance, improved compatibility with automation platforms, and enhanced cybersecurity. Price competitiveness and after-sales support also play significant roles in market differentiation.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The biggest driver is the widespread push for Industry 4.0 and factory automation, requiring rugged computing at the machine level. Fanless industrial computers are ideal because they resist dust, vibration, and temperature extremes without overheating. Their reliability and low maintenance requirements make them essential for real-time data processing and control in harsh industrial settings.

Q2. What are the main restraining factors for this market?

The main limitation is the higher cost compared to traditional fan-cooled PCs, due to the specialized heat dissipation hardware required. Furthermore, fanless systems often offer slightly lower peak processing power, as they rely on passive cooling, which can be a restraint for extremely complex or computationally demanding industrial applications.

Q3. Which segment is expected to witness high growth?

The Manufacturing segment is poised for the highest growth, driven by aggressive adoption of Industry 4.0 and smart factory initiatives. This transition requires rugged fanless control computers to manage robotics, vision systems, and IoT data directly on the shop floor. Their durability and resistance to dust and heat ensure maximized production uptime and efficiency in automation processes.

Q4. Who are the top major players for this market?

The Fanless Industrial Control Computer market is led by companies specializing in industrial automation hardware. Key players include large global manufacturers like Advantech, Siemens, Beckhoff Automation, Kontron, and DFI. These companies compete by offering robust, certified systems designed for specific vertical industrial sectors.

Q5. Which country is the largest player?

China and the Asia Pacific region as a whole collectively hold the largest market share. This dominance is driven by massive investment in manufacturing capacity, widespread government support for rapid industrialization, and the massive consumer electronics and semiconductor production base located in the region.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model