Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global IGBT Hybrid Modules Market refers to the worldwide industry focused on the production, distribution, and application of Insulated Gate Bipolar Transistor (IGBT) hybrid modules, which combine IGBT chips with other power semiconductor components (such as diodes or drivers) in a single package. These modules are widely used in high-efficiency power conversion systems across sectors such as automotive (especially electric vehicles), renewable energy, industrial automation, rail traction, and consumer electronics. The market is driven by the growing demand for energy-efficient and compact power solutions, rising electrification trends, and advancements in power electronics. Increasing investments in electric mobility and renewable infrastructure are further propelling growth, alongside technological improvements in thermal management, switching speed, and module reliability.

The Global IGBT Hybrid Modules Market is witnessing significant growth due to rising demand for energy-efficient power electronics in sectors such as electric vehicles (EVs), renewable energy systems, and industrial automation. Key trends include the integration of wide-bandgap materials like silicon carbide (SiC) for improved performance, and advancements in thermal management technologies to support higher power densities. Manufacturers are focusing on compact, hybrid designs that combine IGBTs with other components to enhance efficiency and reduce system complexity. The transition to higher voltage classes and the growing need for high-frequency switching applications are further driving innovation. Additionally, the global push towards electrification and sustainability is accelerating adoption, particularly in EVs and solar inverters, making IGBT hybrid modules increasingly indispensable in modern power systems.

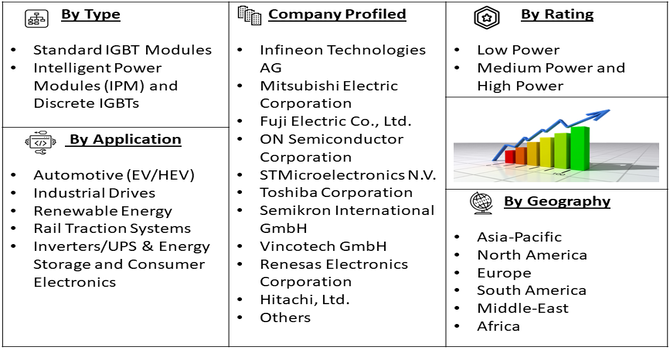

Segmentation: The Global IGBT Hybrid Modules Market is Segmented by Voltage Class (Low Voltage, Medium Voltage and High Voltage), Product Type (Standard IGBT Modules, Intelligent Power Modules (IPM) and Discrete IGBTs), Power Rating (Low Power, Medium Power and High Power), Application (Automotive (EV/HEV), Industrial Drives, Renewable Energy, Rail Traction Systems, Inverters/UPS & Energy Storage and Consumer Electronics) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The accelerating adoption of electric vehicles (EVs) globally, particularly in the U.S. where EV sales have surpassed 1 million units in nine months, is a key driver for the IGBT hybrid modules market. Leading automakers like Tesla and General Motors are pushing the transition to fully electric fleets, increasing demand for efficient power semiconductor components. IGBT hybrid modules play a critical role in electric drivetrains and onboard power management, ensuring high efficiency and reliability. As governments promote clean transportation and consumers shift towards sustainable mobility, EV production and infrastructure investments continue to rise. This sustained growth directly fuels the need for advanced IGBT modules, driving innovation and expansion within the market.

The growing focus on renewable energy sources such as solar and wind power is significantly propelling the demand for IGBT hybrid modules. These modules are essential components in power converters and inverters used to integrate renewable energy into electrical grids. As countries worldwide commit to reducing carbon emissions, the installation of solar farms, wind turbines, and other clean energy systems has surged. Efficient energy conversion and grid stabilization require high-performance IGBT modules capable of handling high voltages and currents with minimal losses. This shift toward cleaner energy infrastructure is creating lucrative opportunities for manufacturers and is a major factor supporting the expansion of the global IGBT hybrid modules market.

Market Restraints:

Despite growing demand, the Global IGBT Hybrid Modules Market faces challenges due to the high costs associated with manufacturing and raw materials. Producing advanced IGBT modules involves expensive semiconductor materials, such as silicon carbide and specialized insulation layers, alongside complex fabrication processes. These cost factors can limit affordability, particularly in price-sensitive markets or developing regions. Furthermore, supply chain constraints and fluctuating prices of raw materials like rare earth elements may disrupt production and increase overall costs. Such economic pressures can slow down market penetration, hinder adoption rates, and force manufacturers to balance cost-efficiency with performance, restraining the market’s overall growth potential.

The expansion of the IGBT hybrid modules market has notable socio-economic implications, particularly in driving the global shift towards sustainable energy and electrification. By enabling higher energy efficiency and lower power losses, these modules contribute to reduced carbon emissions and operational costs across multiple industries. Their use in electric vehicles and renewable energy infrastructure supports job creation in manufacturing, research, and deployment sectors, especially in emerging economies investing in clean energy. Government initiatives promoting green technologies and energy efficiency further stimulate market growth and accessibility. However, challenges remain in the form of high initial costs, supply chain dependencies, and limited access to advanced semiconductor technologies in developing regions. Thus, the market plays a crucial role in enabling economic modernization and environmental sustainability.

Segmental Analysis:

The Medium Voltage (601V to 1700V) segment is projected to exhibit the highest growth, driven primarily by the global shift towards 800V battery platforms in Electric Vehicles (EVs). This higher voltage architecture in performance vehicles requires 1200V and 1700V rated IGBTs for traction inverters to ensure efficient power conversion and faster charging times. Furthermore, the versatile nature of this voltage class makes it indispensable for industrial motor drives, high-efficiency Heating, Ventilation, and Air Conditioning (HVAC) systems, and residential solar PV inverters. The continuous industrial automation trend, demanding efficient motor control, cements the Medium Voltage segment as the future high-growth leader.

Intelligent Power Modules (IPMs) are forecast to see the strongest growth due to their inherent advantages of integration and enhanced reliability. IPMs combine the IGBT, gate driver, and various protection circuits (like over-current and over-temperature) into a single package. This "plug-and-play" capability dramatically simplifies system design for Original Equipment Manufacturers (OEMs), reduces overall Bill of Materials (BOM) cost, and minimizes system complexity. Their adoption is accelerating in high-growth applications such as industrial servo drives, high-efficiency home appliances, and Battery Energy Storage Systems (BESS), providing the compact, high-performance power control necessary for modern electronics.

The Medium Power (e.g., 10kW to 200kW) segment is a key high-growth area due to its perfect balance of power handling and cost-efficiency. This power band is ideally suited for the mass-market adoption of 1200V IGBTs in commercial and passenger Electric Vehicles, particularly for on-board chargers and the main traction drive. Crucially, Medium Power IGBTs are the workhorses of industrial automation, heavily utilized in Variable Frequency Drives (VFDs) for controlling moderate-sized factory equipment and pumps. The strong investment cycles in manufacturing and the surging demand for 5G infrastructure worldwide further underpin this segment's robust growth forecast.

The Consumer Electronics segment is anticipated to witness substantial growth, largely driven by regulatory pushes for energy efficiency in high-power home appliances. Governments worldwide are enforcing stricter energy standards for air conditioners, refrigerators, and washing machines, compelling manufacturers to transition from traditional motors to highly efficient inverter-based motor controls. These inverter controls use Low-to-Medium Voltage IGBTs to regulate power with minimal loss. The rising disposable incomes in the Asia-Pacific region, coupled with the demand for smart, silent, and reliable appliances, are providing the essential volume and technological upgrade momentum for this segment.

The North American region is expected to lead global market growth, driven by significant government-backed initiatives and private sector investment. The rapid expansion of electric vehicle manufacturing and charging infrastructure, supported by supportive federal policies, is creating massive demand for high-power IGBT modules.

Concurrently, investments in renewable energy, smart grid modernization, and large-scale data center expansion necessitate high-efficiency power semiconductors for inverters and power management. This confluence of technological innovation and mandated energy-saving initiatives positions the U.S. and Canada as the fastest-growing geographical market for IGBT technologies. For instance, in September 2025, ABB Installation Products advanced the home EV charging market with its Microlectric EM Series Electric Vehicle Energy Management System (EVEMS), designed to optimize energy distribution without costly electrical upgrades. By intelligently monitoring real-time electrical capacity and controlling charging accordingly, ABB’s EVEMS made residential EV charging more accessible and cost-effective amid rising EV adoption. This innovation reduced the need for expensive panel upgrades and eased power management challenges for homeowners. As a result, the growing deployment of such smart charging solutions has driven increased demand for high-performance power electronics, including IGBT hybrid modules used in EV chargers and energy management systems, thereby fueling growth in the global IGBT hybrid modules market.

In October 2025, an article published by CNBC reported that U.S. electric vehicle (EV) sales, surpassed 1 million units in the first nine months of the year, with a record-breaking third quarter of over 438,000 units sold, capturing a 10.5% market share. Tesla and General Motors have emerged as the leading players in all-electric vehicle sales within the U.S. This rapid growth in EV adoption is driving strong demand for power electronics components, particularly IGBT hybrid modules, which are critical for efficient power management in electric drivetrains and charging infrastructure. Consequently, the expanding EV market is significantly propelling the growth of the U.S. segment of the global IGBT hybrid modules market, stimulating investment and innovation in semiconductor manufacturing and supply chains.

| Report Matrics | Details |

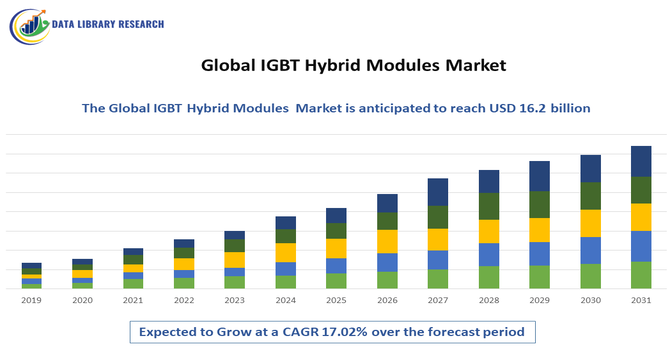

| Market Size Value | USD 16.2 billion |

| Growth Rate | CAGR of 17.02 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the IGBT hybrid modules market is defined by the presence of leading global players such as Infineon Technologies, Mitsubishi Electric, Fuji Electric, ON Semiconductor, and Semikron Danfoss. These companies compete on innovation, efficiency, product reliability, and cost. Technological advancements, particularly in SiC integration and thermal performance, are key differentiators. While large players dominate through established supply chains and R&D capabilities, regional manufacturers—particularly in Asia-Pacific—are rapidly gaining ground through competitive pricing and government-backed incentives. The market also sees increasing specialization, with niche players offering custom modules tailored for specific industries like automotive or solar energy. Strategic partnerships, mergers, and investments in localized production are becoming common strategies to maintain competitiveness in this rapidly evolving landscape.

The 20 major players for above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The main growth drivers are the accelerating global adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs), where IGBT hybrid modules are crucial for efficient motor control. Furthermore, the rapid expansion of renewable energy infrastructure, including wind and solar power inverters, and increasing industrial automation requiring efficient power conversion systems significantly boost market demand.

Q2. What are the main restraining factors for this market?

Key restraining factors include the relatively high initial manufacturing cost of IGBT hybrid modules compared to traditional power devices. Design complexities, such as the need for sophisticated thermal management systems for high-power applications, and concerns regarding long-term reliability and potential component failures also pose challenges to widespread market adoption.

Q3. Which segment is expected to witness high growth?

The Electric Vehicles/Hybrid Electric Vehicles (EV/HEV) application segment is projected to witness the highest Compound Annual Growth Rate (CAGR). This explosive growth is driven by stringent global emission regulations, government incentives for electric mobility, and the continuous need for high-efficiency, reliable power electronics in EV powertrains and charging infrastructure.

Q4. Who are the top major players for this market?

The IGBT Hybrid Modules market is dominated by several key players, primarily semiconductor manufacturers. The top major players include Infineon Technologies AG, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., ON Semiconductor (onsemi), STMicroelectronics, and Semikron Danfoss. These companies lead in product innovation, especially in incorporating Silicon Carbide (SiC) technology.

Q5. Which country is the largest player?

The Asia Pacific region, particularly China, is the largest player in the IGBT market in terms of both manufacturing and consumption. This dominance is due to rapid industrialization, the region's massive automotive electrification initiatives, and substantial government-backed investments in renewable energy and power infrastructure.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model