Get Complete Analysis Of The Report - Download Updated Free Sample PDF

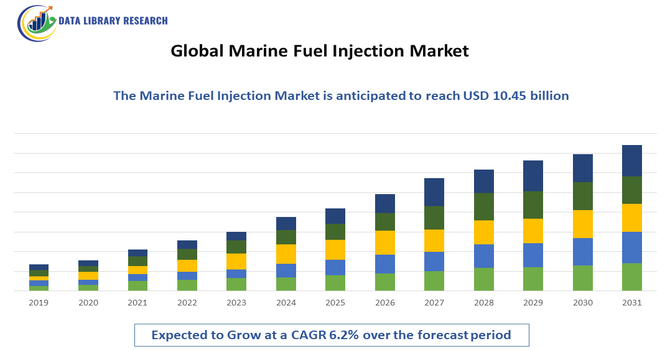

The Global Marine Fuel Injection Market encompasses the production, distribution, and technological advancement of fuel injection systems for marine engines. It focuses on improving fuel efficiency, reducing emissions, and ensuring optimal engine performance in ships, boats, and submarines, driven by environmental regulations and increasing maritime trade activities worldwide.

The growth of the Global Marine Fuel Injection Market is driven by increasing international maritime trade, the rising demand for fuel-efficient and low-emission marine engines, and stringent environmental regulations by organizations such as the IMO. Advancements in fuel injection technologies, such as electronic and common rail systems, are enhancing engine performance, fuel economy, and emission control. Additionally, the growing adoption of cleaner fuels like LNG and biofuels, coupled with the modernization of older vessels, further boosts market expansion. Rapid shipbuilding activities and increasing investments in marine transportation infrastructure also contribute significantly to the market’s growth.

The Global Marine Fuel Injection Market is witnessing several key trends, including the growing adoption of electronically controlled and common rail fuel injection systems for enhanced efficiency and precision. There is an increasing shift toward cleaner and sustainable marine fuels such as LNG, biofuels, and methanol to meet stringent emission norms. Digitalization and automation in marine engines, along with the integration of IoT-based monitoring systems, are improving performance, fuel optimization, and maintenance efficiency. Additionally, rising investments in R&D for hybrid and low-emission propulsion technologies, as well as the retrofitting of older vessels with advanced fuel injection systems, are shaping the market’s future landscape.

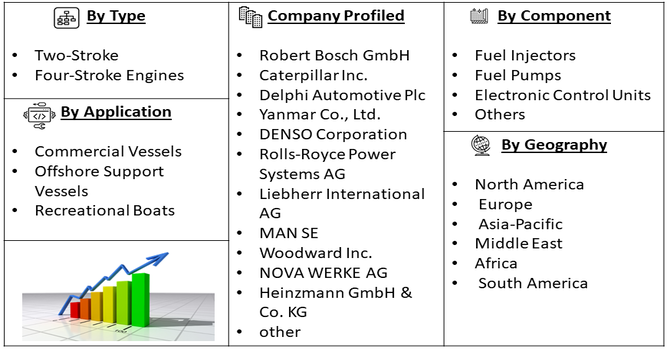

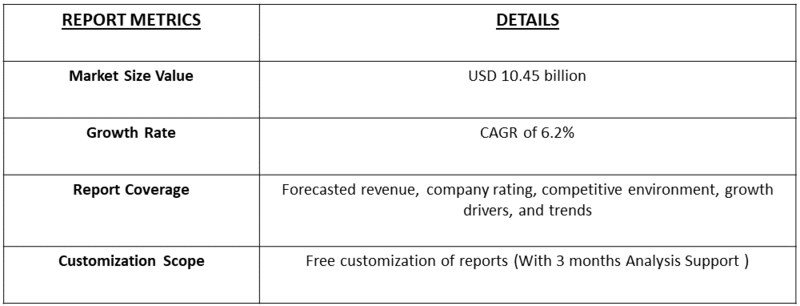

Segmentation: The Global Marine Fuel Injection Market is segmented by Component (Fuel Injectors, Fuel Pumps, Electronic Control Units, and Others), Engine Type (Two-Stroke and Four-Stroke Engines), Application (Commercial Vessels, Offshore Support Vessels, and Recreational Boats) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The key drivers of the Global Marine Fuel Injection Market is the growing demand for fuel-efficient and low-emission marine engines. With rising environmental concerns and stricter regulations imposed by international bodies like the International Maritime Organization (IMO), shipowners and manufacturers are prioritizing advanced fuel injection systems that optimize fuel combustion and minimize pollutants such as NOx, SOx, and particulate matter. These systems ensure better atomization and precise fuel delivery, leading to improved engine efficiency and reduced fuel consumption. Additionally, the increasing adoption of technologies like electronic and common rail fuel injection systems is further propelling market growth, as they offer enhanced performance, reliability, and compliance with evolving global emission standards.

The expansion of global maritime trade and increasing shipbuilding activities are major factors fueling the growth of the marine fuel injection market. With over 80% of global trade transported by sea, the demand for new vessels, including cargo ships, tankers, and container ships, continues to rise. This surge in fleet size drives the need for efficient and durable fuel injection systems to support high-performance marine engines. Furthermore, emerging economies in Asia-Pacific, particularly China, South Korea, and Japan, are witnessing rapid industrialization and infrastructural growth, which has strengthened shipbuilding capabilities. As international shipping routes expand and the global economy rebounds, the modernization of existing fleets and the integration of advanced fuel injection technologies are expected to further accelerate market development.

Market Restraint:

The Global Marine Fuel Injection Market faces challenges due to the high initial investment and complex maintenance associated with advanced fuel injection systems. Modern systems, such as electronic and common rail types, involve sophisticated components and precision engineering, which significantly increase installation and production costs. Smaller ship operators, particularly in developing regions, often find it difficult to afford these technologies, limiting market penetration. Additionally, maintaining and calibrating these systems requires skilled technicians and specialized tools, increasing operational expenses. The availability of spare parts and technical expertise can also be a challenge in remote marine regions. These cost-related barriers may hinder the adoption rate of advanced systems, especially among cost-sensitive market segments.

The Global Marine Fuel Injection Market has significant socioeconomic impacts, influencing both global trade efficiency and environmental sustainability. By enhancing fuel efficiency and reducing emissions, advanced fuel injection systems help lower operational costs for shipping companies, thereby supporting international trade and economic growth. The industry also stimulates job creation in sectors such as shipbuilding, manufacturing, maintenance, and marine engineering, particularly in coastal economies like China, South Korea, and Japan. Moreover, the adoption of cleaner fuel technologies contributes to improved air quality and reduced health risks in port cities and coastal communities. However, the high cost of technological upgrades poses financial challenges for smaller operators, potentially widening the gap between developed and developing maritime economies.

Segmental Analysis:

The fuel injectors segment is projected to experience substantial growth in the Global Marine Fuel Injection Market over the forecast period, driven by increasing demand for efficient fuel delivery and combustion systems in marine engines. Fuel injectors play a critical role in optimizing engine performance, improving fuel economy, and reducing harmful emissions. The shift toward electronically controlled and high-pressure injectors, particularly in large commercial vessels and modern ship engines, is further accelerating market expansion. Advancements in materials and design are enhancing injector durability and precision, enabling them to withstand harsh marine environments. Additionally, rising investments in R&D for next-generation injectors compatible with cleaner fuels such as LNG and biofuels are expected to create significant growth opportunities.

The two-stroke engine segment is expected to witness notable growth in the marine fuel injection market due to its widespread use in large vessels such as cargo ships, bulk carriers, and tankers. These engines are favored for their high power output, fuel efficiency, and ability to handle heavy-duty operations over long distances. The integration of advanced fuel injection systems in two-stroke engines enhances combustion control, reduces emissions, and ensures compliance with stringent international maritime regulations. Growing global trade activities and fleet modernization programs are further driving demand for these engines. Additionally, ongoing technological innovations—such as electronic common rail systems and adaptive injection timing—are improving engine reliability and performance, making two-stroke engines increasingly preferred in the global marine industry.

The recreational boats segment is anticipated to show strong growth in the Global Marine Fuel Injection Market, supported by increasing disposable incomes, rising interest in leisure boating, and expanding marine tourism. Modern recreational boats demand high-performance engines that offer smooth operation, enhanced fuel efficiency, and lower emissions—all of which rely heavily on advanced fuel injection systems. The growing popularity of personal watercraft, yachts, and small boats in regions such as North America, Europe, and Asia-Pacific is creating substantial opportunities for fuel injection system manufacturers. Moreover, the trend toward environmentally friendly boating, coupled with the adoption of cleaner fuels and electronically controlled injectors, is fostering innovation in this segment, ensuring long-term market expansion across both developed and emerging economies.

The Asia-Pacific region is expected to dominate and witness significant growth in the Global Marine Fuel Injection Market throughout the forecast period. This growth is primarily attributed to the region’s robust shipbuilding industry, increasing maritime trade, and rising demand for commercial vessels. Countries such as China, South Korea, and Japan are major shipbuilding hubs, driving large-scale adoption of advanced fuel injection technologies.

Additionally, rapid industrialization, economic expansion, and investments in port infrastructure are boosting marine transportation activities across the region. HSD Engine’s Tekomar XPERT transformed reliable engine data into actionable insights, reducing fuel consumption, lowering emissions, and optimizing maintenance, while enabling fleet-wide performance benchmarking. HSD Engine, formerly Doosan, had delivered 90–100 low- and medium-speed marine engines For instance, in December 2023, Nippon Yusen Kabushiki Kaisha, Japan Engine Corporation, IHI Power Systems, and Nihon Shipyard constructed the world’s first ammonia-fueled medium gas carrier, advancing low-emission marine technologies. Together, these developments boosted the Global Marine Fuel Injection Market by driving adoption of intelligent and alternative-fuel injection systems, improving efficiency, and supporting decarbonization initiatives.

Moreover, the government initiatives promoting cleaner marine fuels and compliance with IMO emission regulations are further accelerating technological adoption. With growing exports, expanding naval fleets, and modernization of existing ships, Asia-Pacific is set to remain the leading contributor to market growth globally.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global marine fuel injection market is characterized by a moderately concentrated structure with leading technology-driven firms commanding a meaningful portion of market share. Key players such as Robert Bosch GmbH, Caterpillar Inc., Delphi Automotive PLC, Yanmar Co. Ltd and MAN SE are investing in R&D, alliances with shipbuilders, and aftermarket services to differentiate through performance, reliability and emission-compliance. Meanwhile, competition is intensifying via product upgrades (e.g., common-rail systems, electronic control units), cost pressures especially in retrofit and aftermarket segments, and geographic expansion into growth regions such as Asia-Pacific. The result is that smaller players must focus on niche segments or partnerships to maintain competitiveness while larger firms capitalize on scale, technological superiority and established customer relationships.

Here are 20 major players operating in the Global Marine Fuel Injection Market:

Recent Development

Q1. What the main growth driving factors for this market?

The marine fuel injection market is strongly driven by stringent global environmental regulations, particularly those from the International Maritime Organization (IMO), which require ships to significantly reduce Sulfur Oxide and Nitrogen Oxide emissions. This necessitates the adoption of advanced, high-pressure fuel injection systems, like common rail, for superior fuel efficiency and lower emissions. Furthermore, the steady growth in global maritime trade and the need to modernize aging commercial vessel fleets globally create consistent demand for new and replacement fuel injection systems.

Q2. What are the main restraining factors for this market?

The key restraining factors is the high upfront cost and complexity of advanced electronic and common rail fuel injection systems compared to older mechanical types. This high investment can deter smaller shipping companies and vessel owners from upgrading their fleets. Additionally, the volatility in the prices of both conventional and alternative marine fuels creates uncertainty in long-term investment decisions, as ship operators hesitate to commit to expensive injection systems designed for a specific fuel type.

Q3. Which segment is expected to witness high growth?

The Common Rail Systems product type segment is expected to witness the highest growth. This technology allows for electronic control and high injection pressure, which is critical for meeting the latest IMO Tier III emission standards and optimizing fuel consumption. Common rail systems offer superior precision, enabling the use of dual-fuel engines (e.g., LNG and MGO), which are increasingly preferred for environmental compliance and operational flexibility, thus pushing this segment forward.

Q4. Who are the top major players for this market?

The market is dominated by global technology and engine manufacturing giants that have specialized in high-performance power systems. The top major players include Wärtsilä, MAN Energy Solutions (part of Volkswagen Group), and specialized component manufacturers like Woodward, Inc. and Robert Bosch GmbH. Additionally, engine and equipment manufacturers such as Caterpillar Inc. and Rolls-Royce plc are significant players, offering integrated marine power and propulsion solutions that incorporate advanced fuel injection technology.

Q5. Which country is the largest player?

The Asia-Pacific (APAC) region holds the largest market share, driven primarily by major shipbuilding countries like China, South Korea, and Japan. China, in particular, is considered the largest country player due to its massive shipbuilding industry, high output of commercial vessels, and its growing role in global maritime trade, which generates significant demand for new marine engines and advanced fuel injection systems for both domestic use and export.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model