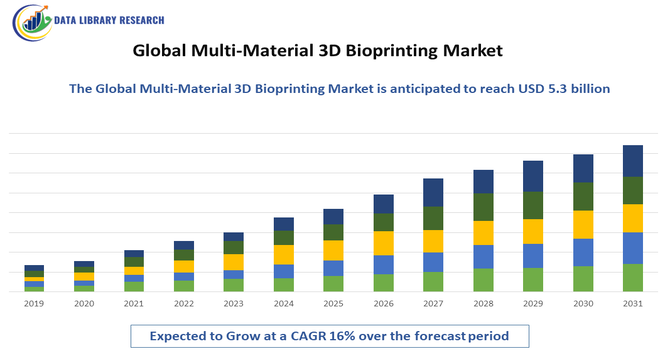

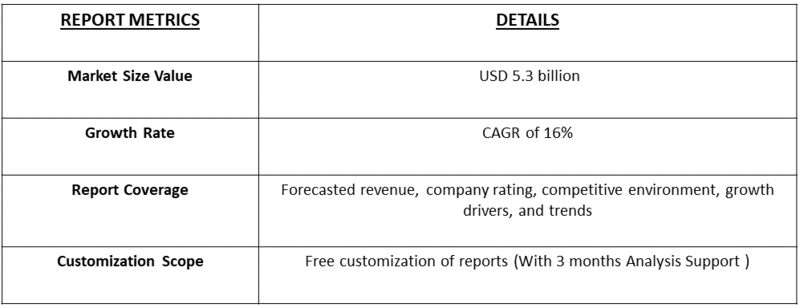

The Global 3D Bioprinting Market, which includes the advanced multi-material segment, was valued at approximately USD 1.73 billion in 2025 and is projected to reach around USD 5.3 billion by 2032. This rapid growth is expected to occur at a robust Compound Annual Growth Rate (CAGR) in the range of 13% to 16% over the forecast period, driven by surging demand for regenerative medicine and the development of personalized drug testing platforms.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Rapid advances in multi-material printing technologies, especially printers that can deposit different cell types, hydrogels and sacrificial/support materials with micrometer precision, are the primary engine behind growth—these technical improvements make heterogeneous, vascularized tissue constructs feasible and expand application scope. Coupled to this, sustained R&D and rising investment from governments, academic consortia and industry (strategic partnerships, start-up funding and M&A) are accelerating commercialization and scaling of platforms and consumables.

The latest trends in the global multi-material 3D bioprinting market center on richer, application-tailored bioinks and material blends (decellularized-matrix, composite hydrogels and cell-laden hybrid formulations) that allow finer control of mechanics and biology; this is driving more physiologically relevant constructs. Closely linked is a strong push toward vascularized and perfusable multi-material prints—using sacrificial inks, coaxial/nozzle innovations and embedded microchannels—to produce tissue models and implants that can be maintained and matured in vitro. Technically, the field is moving beyond simple 3D deposition toward multimaterial, multidimensional approaches (sometimes framed as 4D/5D printing), with higher resolution multi-nozzle systems and programmable materials that change properties after printing.

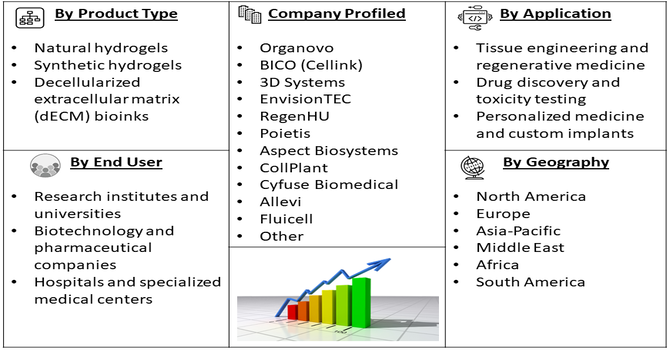

Segmentation: Global Multi-Material 3D Bioprinting Market is segmented By Technology (Extrusion-based multi-material bioprinting, Inkjet-based multi-material bioprinting, Laser-assisted multi-material bioprinting, Stereolithography (SLA)/Digital Light Processing (DLP) bioprinting), Material Type (Natural hydrogels, Synthetic hydrogels, Decellularized extracellular matrix (dECM) bioinks), Application (Tissue engineering and regenerative medicine, Drug discovery and toxicity testing, Personalized medicine and custom implants), End User (Research institutes and universities, Biotechnology and pharmaceutical companies, Hospitals and specialized medical centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A major driver for the global multi-material 3D bioprinting market is the growing demand for highly functional, physiologically accurate tissue constructs that mimic the structural and biological complexity of human organs. Traditional single-material bioprinting cannot replicate heterogeneous tissues where multiple cell types, extracellular matrix components, and mechanical gradients coexist. In 2025, an article published in journal, Front. Bioeng. Biotechnol. Reported that the evolution of 3D bioengineered tissue models had addressed limitations of traditional 2D and animal-based preclinical testing, offering more reliable human-relevant results. This advancement had driven pharmaceutical companies to adopt multi-material 3D bioprinting, boosting demand for complex, functional, and vascularized tissue models, and accelerating innovation in drug discovery and screening.

Pharmaceutical companies increasingly require advanced tissue models for high-throughput drug screening, toxicity assessment, and disease modeling, as multi-material constructs provide superior predictive accuracy compared to 2D cultures or animal models. As the industry moves closer to functional organ fabrication, demand for multi-material-enabled platforms continues to accelerate.

The rapid progression of the multi-material 3D bioprinting market is strongly supported by rising R&D investments across biotechnology firms, academic institutions, and government-funded research programs. Significant financial support is directed toward developing next-generation bioinks, including hybrid hydrogels, decellularized extracellular matrix formulations, and smart materials that exhibit tunable mechanical, chemical, and biological properties. The convergence of bioprinting with AI, microfluidics, organ-on-chip technologies, and 4D materials further expands its application potential. As R&D ecosystems grow and patents increase, the pace of commercialization quickens, encouraging broader adoption across clinical and industrial domains.

Market Restraints:

The growth of the global multi-material 3D bioprinting market is hindered by several challenges, including the high cost of advanced bioprinters, multi-nozzle systems, and specialized bioinks, which limits adoption among smaller research labs and emerging biotech companies. Technical complexities—such as achieving stable crosslinking between different materials, ensuring cell viability during multi-material deposition, and maintaining structural integrity in highly heterogeneous constructs—also slow commercialization and routine clinical use. Additionally, the lack of standardized protocols for multi-material bioink formulation, printing parameters, and post-printing tissue maturation creates variability in research outcomes.

The Global Multi-Material 3D Bioprinting Market has had profound socioeconomic impacts by transforming healthcare, pharmaceuticals, and research sectors. It has enabled rapid development of tissue engineering, organ models, and drug testing platforms, reducing reliance on animal testing and accelerating medical innovation. The market’s growth has created high-skill job opportunities in biotechnology, engineering, and materials science, while fostering investment in research, infrastructure, and advanced manufacturing. Additionally, it has the potential to improve patient outcomes, lower treatment costs, and enhance accessibility to personalized medicine. However, high technological and regulatory barriers may limit adoption in developing regions, highlighting global disparities in access to advanced healthcare solutions.

Segmental Analysis:

Extrusion-based multi-material bioprinting dominates the market as the most widely adopted technology due to its versatility, ability to print high-viscosity bioinks, and compatibility with multiple cell-laden materials simultaneously. This technology enables precise layer-by-layer deposition, making it ideal for producing structurally stable constructs such as cartilage, bone, and vascularized tissues. Its scalability, cost-effectiveness, and support for multi-nozzle configurations further strengthen its use in both research and preclinical applications. As innovation advances, extrusion systems are increasingly integrated with temperature control, automated calibration, and real-time imaging, improving print resolution and biological performance.

Natural hydrogels represent a major material segment owing to their biocompatibility, bioactivity, and suitability for supporting cell growth and differentiation. Materials such as collagen, gelatin, alginate, and fibrin closely mimic the extracellular matrix (ECM), making them essential for printing multi-material, cell-laden tissue constructs. Their ability to be blended with synthetic polymers or functional additives enhances mechanical strength while maintaining biological integrity. As demand grows for more physiologically relevant engineered tissues, natural hydrogels remain the preferred choice for complex, multi-material bioprinting applications used in regenerative medicine and in vitro modeling.

Tissue engineering and regenerative medicine account for the largest share within applications, driven by increasing efforts to create implantable tissues, organoids, and vascularized constructs for therapeutic use. Multi-material bioprinting enables the precise combination of multiple cell types, bioinks, and support structures, which is essential for replicating heterogeneous tissues such as skin, bone, cartilage, and cardiac tissue. The rising prevalence of chronic diseases, increased need for organ replacements, and advancements in stem cell research further boost demand in this segment. As clinical translation advances, this application is expected to witness strong growth over the forecast period.

Biotechnology and pharmaceutical companies represent a rapidly growing end-user segment, driven by the increasing use of multi-material 3D bioprinting for drug discovery, toxicity screening, and personalized therapeutic development. Multi-material printed tissues provide more accurate human-like models, reducing reliance on animal testing and improving early prediction of drug safety and efficacy. Companies are investing heavily in high-throughput bioprinting platforms, automated workflows, and bioprinted organ-on-chip systems to accelerate R&D timelines. This segment’s growth is further fueled by collaborations between pharma companies, bioprinting technology providers, and academic institutions.

North America leads the global market due to strong research infrastructure, high R&D investments, and early adoption of advanced bioprinting technologies. The region benefits from a large presence of bioprinting companies, biotechnology firms, and well-funded academic research centers working on regenerative medicine and tissue engineering.

Supportive government initiatives, increasing clinical trials involving bioprinted tissues, and growing collaborations between universities and industry players further strengthen the region's dominance. With continued investment in precision medicine and advanced biomaterials, North America is expected to maintain its leading position during the forecast period. For instance, November 2025, Scientists at the University of Virginia had developed a novel 3D printable material compatible with the immune system. This innovation had advanced safer implantable devices, next-generation drug-delivery systems, and solid-state battery applications, driving technological progress, fostering adoption, and strengthening growth in the US Multi-Material 3D Bioprinting Market.

Similarly, in September 2025, ETH Zurich students’ development of a multi-metal laser powder bed fusion 3D printing system had represented a major technological breakthrough. By enabling simultaneous printing of multiple metals, it had showcased the potential of advanced multi-material fabrication, inspiring innovation and indirectly driving growth and adoption in the US Multi-Material 3D Bioprinting Market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape for the global multi-material 3D bioprinting market is dynamic and fragmented, characterized by a mix of specialized start-ups, established medical device firms, and multidisciplinary players. Competition centers on platform performance (resolution, multi-nozzle capability, automation), proprietary bioinks and material libraries, partnerships with pharma and academic centres, and pathways to regulatory validation and commercialization. Increasing M&A, strategic collaborations, and vertical integration (hardware + consumables + software + application services) are common as firms seek to build end-to-end solutions and shorten time-to-market. Price pressures from new low-cost entrants are balanced by premium offerings that target clinical translation and pharmaceutical-grade workflows, making innovation, IP and strong customer validation the key differentiators going forward.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is primarily driven by the massive increase in research and development funding directed towards regenerative medicine and tissue engineering globally. Additionally, there is a surge in demand for non-animal-based testing, particularly in the pharmaceutical and cosmetic sectors, where bioprinted tissues offer ethical and effective alternatives for drug discovery and consumer product testing.

Q2. What are the main restraining factors for this market?

The primary constraint is the extraordinarily high capital and operational costs associated with bioprinting technology. This includes the expense of both the sophisticated printing equipment and the specialized biological materials, or "bioinks," which are required to maintain cell viability. This cost barrier significantly limits the widespread adoption of the technology, especially in smaller research institutions.

Q3. Which segment is expected to witness high growth?

The regenerative medicine application segment is expected to witness the highest growth, as bioprinting is crucial for developing functional tissues and organs for transplantation, addressing the critical shortage of organ donors. Among technology types, extrusion-based and inkjet-based methods hold large shares, with advancements focused on multi-material capabilities for greater precision and complexity in tissue structures.

Q4. Who are the top major players for this market?

The competitive landscape includes specialized bioprinting firms and larger companies. Top major players are BICO Group AB (Cellink), Organovo Holdings Inc., 3D Systems, Inc., and Aspect Biosystems Ltd. These companies focus on developing advanced bioprinters, bioinks, and proprietary software to create complex, viable tissue models for research and eventual clinical use.

Q5. Which country is the largest player?

North America, specifically the United States, holds the largest market share globally. This dominance is due to the region's advanced healthcare infrastructure, substantial government and private R&D investments, and the strong presence of major biotechnology and pharmaceutical companies. The U.S. remains a global leader in commercializing bioprinting applications.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model