Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Oyster Farming Market refers to the cultivation and harvesting of oysters for commercial purposes, primarily for human consumption as seafood, as well as for environmental and ecological benefits such as water filtration and reef restoration. This market encompasses various farming techniques, including bottom culture, off-bottom culture, and suspended systems, across coastal regions worldwide. Driven by rising consumer demand for high-protein, sustainable seafood, increasing awareness of oysters' nutritional value, and expanding aquaculture investments, the market is experiencing steady growth. Technological advancements in hatchery practices, disease management, and water quality monitoring are further enhancing productivity. Additionally, the industry's role in supporting coastal economies and contributing to marine ecosystem health positions oyster farming as a key component of sustainable aquaculture globally.

The Global Oyster Farming Market is experiencing steady, robust growth, driven by increasing worldwide demand for healthy, protein-rich, and sustainable seafood options. Key market trends include a strong consumer preference for premium and artisanal oysters, particularly within the lucrative restaurant and fine-dining foodservice sector, coupled with rising demand from emerging markets in Asia-Pacific. Operational efficiency is being significantly enhanced by technological advancements in aquaculture, such as off-bottom farming methods, selective breeding for disease resistance (specifically for the dominant Pacific Cupped Oyster segment), and the integration of AI for real-time monitoring. Furthermore, a growing focus on sustainable aquaculture practices and the ability of oysters to improve water quality (eco-friendly positioning) is attracting eco-conscious consumers, while the rise of direct-to-consumer online sales is optimizing the supply chain for fresh products.

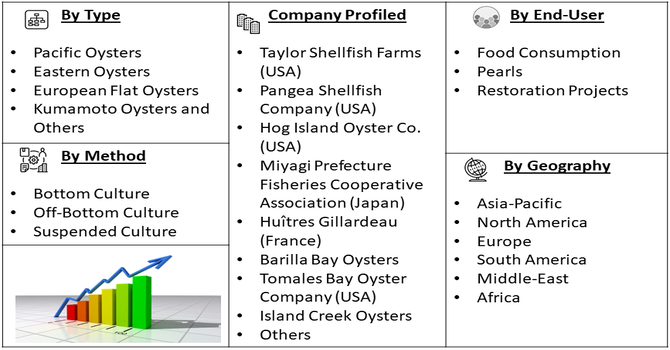

Segmentation: The Global Oyster Farming Market is segmented by Oyster Type (Pacific Oysters, Eastern Oysters, European Flat Oysters, Kumamoto Oysters, and Others), Cultivation Method (Bottom Culture, Off-Bottom Culture, and Suspended Culture), End Use (Food Consumption, Pearls, and Restoration Projects), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global shift toward healthier and more sustainable dietary choices is a major driver of the oyster farming market. Oysters are rich in essential nutrients such as zinc, omega-3 fatty acids, protein, and vitamins, making them a desirable option for health-conscious consumers. Additionally, oysters are considered an environmentally sustainable seafood choice because they require no feed, naturally filter and clean ocean water, and help maintain ecological balance. As sustainability and ocean conservation become global priorities, consumer preference is increasingly moving toward aquaculture products like oysters that have a low environmental footprint. For instance, The OECD-FAO Agricultural Outlook 2025-2034 projected a 6 percent global increase in per capita calorie intake from livestock and fish products over the next decade, with lower-middle-income countries experiencing a rapid 24 percent growth, nearly four times the global average. This significant rise in fish consumption, especially in emerging markets, is expected to boost demand for oyster farming as a sustainable source of protein and nutrition.

The technological advancements in aquaculture practices, including automated feeding systems, water quality monitoring, and disease management, have significantly improved productivity and reduced mortality rates in oyster farming. Hatchery technologies have enabled year-round seed availability and selective breeding for disease resistance and faster growth. These innovations are making oyster farming more commercially viable and scalable.

Simultaneously, governments around the world are supporting aquaculture development through subsidies, training programs, and regulatory frameworks that promote sustainable practices. For instance, in October 2024, Scientists from the Northeast Fisheries Science Center and National Centers for Coastal Ocean Science developed an online Aquaculture Nutrient Removal Calculator for oyster farmers in the Northeast U.S. This tool estimates the amount of nitrogen removed by oyster farms, aiding growers in environmental reporting. The Aquaculture Nutrient Removal Calculator enhances the oyster farming market by promoting environmentally sustainable practices and supporting regulatory compliance. By quantifying the ecological benefits, it helps growers secure permits more easily and improves public perception of oyster farming, encouraging industry growth and investment in the Northeast U.S.

Market Restraints:

Oyster farming is highly sensitive to environmental conditions, which presents a significant restraint to market growth. Factors such as water pollution, rising sea temperatures, ocean acidification, and harmful algal blooms can severely impact oyster survival and quality. Additionally, the spread of diseases like oyster herpesvirus (OsHV-1) and other bacterial infections can lead to large-scale mortality and heavy economic losses for farmers. Climate change further exacerbates these risks, making farming conditions increasingly unpredictable. In many regions, a lack of advanced monitoring and mitigation infrastructure limits the ability to respond quickly to such challenges. These environmental vulnerabilities not only increase production risks and costs but also deter potential new entrants and investors, thereby restraining the long-term scalability of the market.

The Global Oyster Farming Market has a significant socio-economic impact, particularly in coastal and rural communities where it provides vital employment opportunities and supports local economies. As a labor-intensive sector, oyster farming contributes to livelihoods through hatchery operations, farm labor, processing, and distribution. It also stimulates growth in allied industries such as equipment manufacturing, logistics, and seafood retail. Socially, increased access to affordable, nutrient-rich seafood helps improve food security and public health. Environmentally sustainable by nature, oyster farming enhances coastal resilience through water filtration and habitat restoration, contributing to long-term ecological and economic stability. As global demand rises, the market continues to attract investment and innovation, further reinforcing its role in sustainable development and blue economy strategies worldwide.

Segmental Analysis:

The Kumamoto oysters segment is anticipated to witness significant growth due to increasing consumer demand for premium, small-sized oysters with a sweet, buttery flavor. Native to Japan but now cultivated in parts of the U.S. and other regions, Kumamoto oysters are highly prized in gourmet cuisine and upscale seafood markets. Their distinct taste and texture make them a favorite among chefs and oyster connoisseurs, driving demand in both domestic and international markets. Additionally, advancements in hatchery techniques and selective breeding are improving their availability and resilience. As consumers increasingly seek specialty and high-end seafood products, Kumamoto oysters are expected to gain a larger share of the market, especially in countries like the United States, Japan, and South Korea.

The suspended culture segment is projected to experience strong growth due to its high yield potential, efficient space utilization, and reduced risk of sediment-related contamination. This method involves growing oysters in floating baskets, bags, or cages suspended in the water column, allowing for better water flow, oxygenation, and access to nutrients. It also protects oysters from predators and reduces the likelihood of disease and deformities. Suspended culture systems are increasingly adopted in regions with limited intertidal zones and are considered more environmentally sustainable than bottom culture. With rising global demand for premium-quality oysters and the need for scalable, efficient farming systems, suspended culture is becoming the preferred method for commercial oyster production, particularly in North America, Europe, and Asia-Pacific.

The food consumption segment is expected to dominate the oyster farming market, driven by rising global demand for protein-rich, low-fat, and nutrient-dense seafood. Oysters are widely recognized for their health benefits, including high levels of zinc, omega-3 fatty acids, and essential vitamins, making them increasingly popular among health-conscious consumers. The growth of seafood-based cuisines, fine dining trends, and the popularity of raw bars in urban centers are further fueling oyster consumption. In addition, increased availability of farmed oysters through retail chains, seafood markets, and e-commerce platforms is expanding consumer access. As culinary preferences shift toward fresh and sustainable options, the demand for oysters as a delicacy and everyday protein source is projected to rise significantly, particularly in developed economies.

The Asia Pacific region is poised for significant growth in the oyster farming market, led by countries such as China, Japan, South Korea, and the Philippines. China alone contributes the largest share of global oyster production, supported by vast coastal resources, government-backed aquaculture policies, and advanced farming infrastructure. Rising seafood consumption, driven by growing middle-class populations and increasing health awareness, is further accelerating demand across the region. Additionally, technological adoption in hatcheries, disease management, and export logistics is improving production efficiency and product quality.

With expanding international trade, supportive regulations, and strong domestic demand, Asia Pacific is not only a production hub but also an emerging consumption market for oysters. For instance, In January 2025, the Ministry of Oceans and Fisheries unveiled an ambitious Development Plan for South Korea’s oyster aquaculture industry, aiming to increase annual production from 300,000 tons in 2023 to 400,000 tons by 2030 and double exports to reach USD 160 million by 2030, targeting market expansion in Europe and improving pollution prevention and safety standards. Thus, such factors are expected to drive the growth of market over the forecast period.

| Report Matrics | Details |

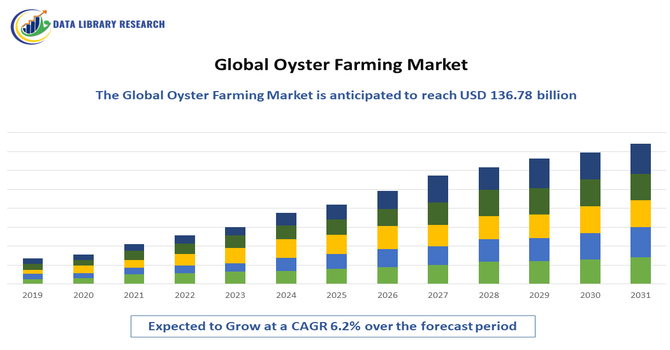

| Market Size Value | USD 136.78 billion |

| Growth Rate | CAGR of 6.2 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global oyster farming market presents a competitive landscape characterized by a mix of large-scale, international producers and numerous smaller, local players, with Asia-Pacific, especially China, holding overwhelming dominance in terms of production volume. Competition centers on species, with the highly adaptable Pacific Oyster being the market leader, and on farming methods, where advanced techniques like suspended culture offer an advantage in efficiency and quality. Major companies such as Taylor Shellfish Farms, Hog Island Oyster Company (US), and France Naissain (France) differentiate themselves through a strong focus on sustainability, product traceability, and brand premiumization for the lucrative raw, half-shell market, particularly in North America and Europe. The competitive strategies also involve adopting technological innovations like automated sorting and hatchery-based seed production to ensure consistent supply and quality, expanding distribution channels to include direct-to-consumer sales, and leveraging eco-certifications to meet the rising consumer demand for high-quality, sustainably farmed seafood.

The 20 major players for above market are:

Recent News:

Q1. What are the main growth driving factors for this market?

The main growth drivers for the global oyster farming market include rising global demand for sustainable and high-protein seafood, increased health consciousness among consumers, and the nutritional benefits of oysters, which are rich in zinc, omega-3 fatty acids, and vitamins. Technological advancements in aquaculture practices—such as improved hatchery techniques, water filtration systems, and disease control—are enhancing production efficiency. Additionally, supportive government policies and investments in coastal aquaculture infrastructure are helping to boost oyster farming. Environmental benefits, like natural water purification and carbon capture, also contribute to the market’s appeal.

Q2. What are the main restraining factors for this market?

The market faces several challenges, including vulnerability to environmental changes such as water pollution, ocean acidification, and climate change, which affect oyster growth and survival rates. Disease outbreaks, such as oyster herpesvirus, can devastate stocks and result in major financial losses. High initial investment costs, limited access to quality seed, and complex regulatory frameworks can deter small-scale farmers from entering or expanding in the market. Furthermore, fluctuating market prices and limited cold chain logistics in some regions also pose hurdles to consistent supply and profitability in the oyster farming industry.

Q3. Which segment is expected to witness high growth?

The Pacific oyster (Crassostrea gigas) segment is expected to witness high growth over the forecast period. This species is favored for its fast growth rate, adaptability to various farming conditions, and strong consumer demand due to its mild flavor and nutritional profile. It is widely cultivated in regions such as Asia-Pacific, North America, and Europe. Additionally, advancements in breeding techniques and disease resistance for Pacific oysters make them a more viable option for both small and large-scale farmers. Their versatility in preparation and export suitability further boosts their dominance in the global market.

Q4. Who are the top major players for this market?

Leading players in the global oyster farming market include Taylor Shellfish Farms (USA), Pangea Shellfish Company (USA), Hog Island Oyster Co. (USA), Chatham Shellfish Company (USA), Zhongshan Foodstuffs and Aquatic Imp. & Exp. Group Co., Ltd. (China), Huon Aquaculture Group Ltd. (Australia), and Maine Shellfish Company (USA). These companies are recognized for their large-scale production, advanced aquaculture technologies, and strong distribution networks. Many of them are vertically integrated, controlling everything from hatcheries to retail. Innovation in sustainable farming methods and international export capabilities helps them maintain a competitive edge in the global market.

Q5. Which country is the largest player?

China is the largest player in the global oyster farming market, accounting for the majority of global production. With vast coastal resources, government support for aquaculture development, and a long-standing tradition of shellfish farming, China leads in both volume and technological advancement. The country's large domestic market for seafood, combined with strong export capacity, supports sustained growth. China's oyster farms benefit from integrated supply chains, extensive hatchery infrastructure, and a skilled labor force. Additionally, the emphasis on sustainable practices and innovation in farming techniques continues to position China as the dominant force in global oyster aquaculture.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model