Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Pathogen metagenomic Next-Generation Sequencing (mNGS) Detection Market refers to the rapidly growing sector focused on the use of high-throughput sequencing technologies to identify and analyze a broad range of pathogens—bacteria, viruses, fungi, and parasites—from clinical samples in a single, unbiased test. Unlike traditional diagnostic methods, mNGS enables comprehensive detection without prior knowledge of the infectious agent, making it especially valuable in complex or undiagnosed infections. This market is driven by rising infectious disease prevalence, antimicrobial resistance, and the demand for precision diagnostics in clinical settings. Key stakeholders include sequencing technology providers, diagnostic labs, hospitals, and research institutions, all contributing to the development and adoption of mNGS as a powerful tool in infectious disease management and public health surveillance.

The Global Pathogen mNGS Detection Market is witnessing rapid growth driven by advancements in sequencing technologies, decreasing costs of genomic testing, and rising demand for comprehensive infectious disease diagnostics. There is a noticeable shift from conventional culture-based methods to unbiased metagenomic approaches due to their ability to detect multiple pathogens—including rare and novel ones—in a single assay. Integration of artificial intelligence and bioinformatics tools for faster and more accurate data interpretation is also gaining traction. Additionally, increased adoption of mNGS in hospital settings, especially for immunocompromised and critically ill patients, along with expanding applications in public health surveillance and outbreak response, continues to accelerate market expansion globally.

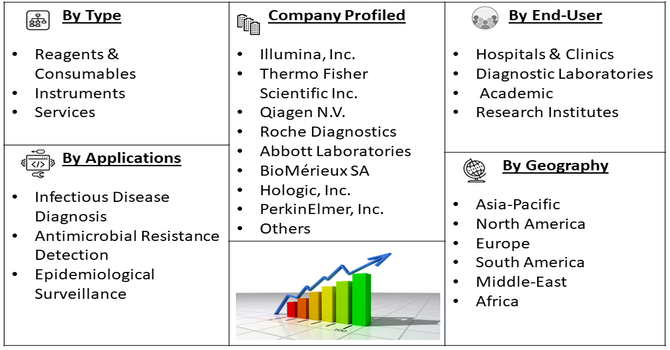

Segmentation: The Global Pathogen mNGS Detection Market is segmented by Product & Service (Reagents & Consumables, Instruments, and Services), Application (Infectious Disease Diagnosis, Antimicrobial Resistance Detection, and Epidemiological Surveillance), End-Users (Hospitals & Clinics, Diagnostic Laboratories, and Academic & Research Institutes) and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing global burden of infectious diseases and the alarming rise in antimicrobial resistance (AMR) are key drivers for the pathogen mNGS detection market. Traditional diagnostic methods often fail to identify uncommon or drug-resistant pathogens promptly, leading to delayed or inappropriate treatment. mNGS offers a comprehensive, unbiased detection platform capable of identifying multiple pathogens and resistance genes from a single sample. This is particularly critical in cases involving sepsis, immunocompromised patients, or unexplained infections. As hospitals and healthcare systems seek more accurate and timely diagnostics to reduce mortality, control outbreaks, and manage AMR, mNGS is becoming an essential tool, driving its adoption and fueling sustained market growth across both developed and emerging healthcare settings.

Rapid advancements in sequencing technologies, coupled with robust bioinformatics tools, are significantly propelling the pathogen mNGS detection market. Innovations such as nanopore sequencing, automation, and reduced turnaround times have made mNGS more accessible and clinically viable. In parallel, AI-powered data interpretation platforms now allow for faster, more accurate analysis of complex metagenomic data, enabling real-time diagnosis and decision-making. These developments reduce the technical barriers that once limited mNGS to research settings and are driving its transition into routine clinical diagnostics. Furthermore, decreasing sequencing costs and improved sample preparation protocols are enhancing scalability. Together, these innovations are expanding the clinical utility of mNGS, boosting adoption across hospitals, labs, and public health agencies.

Market Restraints:

Despite its diagnostic advantages, the high cost of mNGS testing remains a significant barrier to widespread adoption, particularly in low- and middle-income countries. The expenses associated with sequencing equipment, sample processing, bioinformatics infrastructure, and skilled personnel make it less accessible for many healthcare providers. Additionally, limited reimbursement policies from insurers further hinder clinical uptake, as most payers consider mNGS investigational or non-standard for routine use. This financial challenge restricts availability to well-funded hospitals and research institutions. Without broader insurance coverage or cost-reduction strategies, many institutions hesitate to adopt mNGS despite its clinical potential, thereby slowing market penetration, especially in price-sensitive healthcare environments.

The adoption of pathogen mNGS detection is delivering significant socio-economic benefits by enabling earlier and more precise diagnosis of infectious diseases, which reduces unnecessary treatments, hospital stays, and overall healthcare costs. It plays a crucial role in addressing antimicrobial resistance by accurately identifying causative agents, thereby supporting targeted therapy and reducing misuse of antibiotics. In low- and middle-income countries, mNGS has the potential to revolutionize disease surveillance and outbreak containment, although affordability remains a challenge. As the technology becomes more accessible, it contributes to health equity and improved patient outcomes, reinforcing national and global efforts toward enhanced infectious disease preparedness and public health resilience.

Segmental Analysis:

The instruments segment is anticipated to witness significant growth in the pathogen mNGS detection market due to rising demand for advanced sequencing platforms in clinical and research settings. As mNGS transitions from research to routine diagnostics, there is an increasing need for high-throughput, automated instruments capable of delivering rapid and accurate results. The development of compact, cost-effective sequencers with improved sensitivity is driving adoption among hospitals, diagnostic labs, and public health facilities. Additionally, manufacturers are focusing on integrating user-friendly features and real-time data analytics into sequencing instruments, making them more accessible for non-specialist users. This growth is further supported by expanding investments in infectious disease surveillance and personalized medicine, reinforcing the importance of instruments in this evolving market.

The infectious disease segment is projected to experience significant growth within the pathogen mNGS detection market, driven by the increasing prevalence of complex, drug-resistant, and emerging infectious agents. Unlike conventional diagnostics that require targeted assays, mNGS enables comprehensive pathogen identification in a single test, making it ideal for diagnosing unknown or co-infections. Its value is especially pronounced in critical care settings, such as for patients with sepsis or immunocompromised conditions, where time-sensitive, accurate diagnosis is crucial. The segment’s growth is further fueled by global concerns over antimicrobial resistance and the need for rapid outbreak response tools. As healthcare providers increasingly seek accurate, real-time infectious disease diagnostics, mNGS is becoming a cornerstone technology in this application area.

Hospitals and clinics are expected to be major contributors to the growth of the pathogen mNGS detection market, as these facilities are on the front lines of diagnosing and managing infectious diseases. With the rise in hospital-acquired infections, sepsis cases, and undiagnosed febrile illnesses, the demand for comprehensive and accurate diagnostic tools is growing rapidly. mNGS provides hospitals with the ability to detect a wide range of pathogens—including rare and resistant strains—in a single test, significantly improving diagnostic speed and accuracy. Furthermore, as healthcare systems adopt precision medicine approaches, mNGS is increasingly integrated into clinical workflows. With improved reimbursement prospects and awareness, hospitals and clinics are accelerating adoption, positioning this segment for strong, sustained growth.

North America is expected to lead the pathogen mNGS detection market due to its advanced healthcare infrastructure, strong R&D investment, and early adoption of innovative diagnostics. The region benefits from a high prevalence of infectious diseases, growing antimicrobial resistance concerns, and a supportive regulatory environment that encourages clinical implementation of next-generation technologies.

Leading academic institutions, biotech firms, and hospitals in the U.S. and Canada are actively deploying mNGS for infectious disease diagnosis, outbreak surveillance, and personalized treatment planning. For instance, In November 2024, an article published by researchers of Department of Laboratory Medicine, University of California, San Francisco, San Francisco, CA, USA, reported that a 7-year analysis by UCSF of 4,828 cerebrospinal fluid (CSF) samples found mNGS detected pathogens in 14.4% of cases, including viruses (DNA 45.5%, RNA 26.4%), bacteria (16.6%), fungi (8.5%), and parasites (2.9%). Among 220 confirmed infections in a subset, 21.8% were diagnosed solely by mNGS. The test showed a sensitivity of 63.1%, significantly outperforming serologic (28.8%) and other direct detection methods. Such real-world data directly supports the expansion of the global Pathogen mNGS Detection Market across both developed and emerging healthcare systems.

Moreover, increasing public health funding and strategic collaborations among industry players further boost regional growth. With favorable reimbursement trends and a strong focus on precision medicine, North America is positioned to remain at the forefront of mNGS adoption throughout the forecast period.

| Report Matrics | Details |

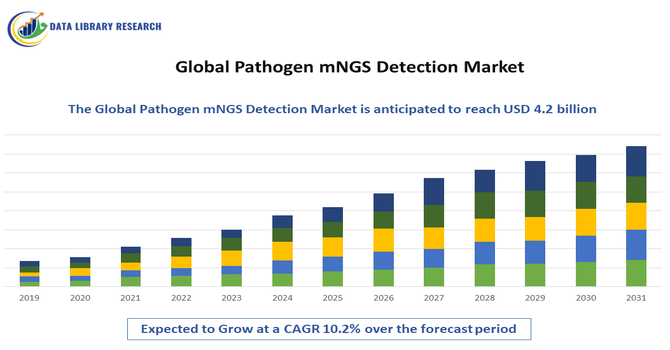

| Market Size Value | USD 4.2 billion |

| Growth Rate | CAGR of 10.2 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the pathogen mNGS detection market is characterized by a mix of established genomics companies and emerging biotech innovators. Key players such as Illumina, Oxford Nanopore Technologies, BGI Genomics, and Fulgent Genetics are investing heavily in technology enhancement, strategic partnerships, and regulatory approvals. Startups focusing on rapid sample-to-result platforms and cloud-based bioinformatics are also gaining ground. Competition centers on turnaround time, accuracy, affordability, and ease of use. Many companies are expanding their clinical diagnostic portfolios, while others are targeting niche areas like neonatal infections or immunocompromised patient care. As regulatory pathways become clearer, the market is expected to see intensified competition and consolidation.

The 20 major players for above market are:

Recent News:

Q1. What are the main growth driving factors for this market?

The primary growth drivers are the increasing global prevalence of infectious diseases, particularly CNS infections like meningitis and encephalitis, and the continuous advancement in sequencing and bioinformatics technologies. Metagenomic Next-Generation Sequencing (mNGS) offers rapid, comprehensive, and unbiased pathogen detection, which is superior to traditional methods. Furthermore, the growing emphasis on precision medicine and increasing investments in genomic research and public health initiatives worldwide are fueling market expansion.

Q2. What are the main restraining factors for this market?

The high initial costs associated with sequencing instruments, reagents, and the necessary data analysis infrastructure are major restraints, especially in low- and middle-income countries. Additional hurdles include the complexity of interpreting mNGS data, the challenge of standardizing methodologies across labs, and the difficulty in distinguishing true pathogens from environmental contaminants or normal colonization, which complicates clinical adoption.

Q3. Which segment is expected to witness high growth?

The Shotgun Metagenomic Sequencing segment is anticipated to witness the highest growth rate within the technology category. Shotgun sequencing provides the most comprehensive data, allowing for the unbiased identification of all microorganisms and the characterization of their functions and antimicrobial resistance genes. Additionally, the Clinical Diagnostics application segment is set for significant expansion as mNGS transitions from a research tool to a routine, critical diagnostic method for severe, hard-to-diagnose infections.

Q4. Who are the top major players for this market?

The global pathogen mNGS detection market is led by major companies that dominate the next-generation sequencing and diagnostics space. Key players include:

These companies offer sequencing instruments, reagents, and bioinformatics software essential for mNGS workflows, driving technological development and market penetration.

Q5. Which country is the largest player?

North America currently dominates the global market and is the largest regional player for Pathogen mNGS Detection. This dominance is underpinned by a robust, well-established healthcare infrastructure, high research and development (R&D) expenditure, and the early, widespread adoption of advanced diagnostic technologies. However, the Asia Pacific region, fueled by rising healthcare expenditure and government investments in genomics, is projected to be the fastest-growing market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model