Get Complete Analysis Of The Report - Download Updated Free Sample PDF

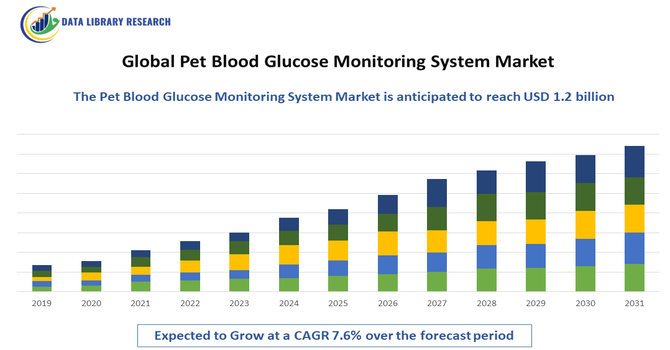

The Global Pet Blood Glucose Monitoring System Market refers to the industry focused on devices, consumables, and software used to measure and track blood glucose levels in pets, primarily dogs and cats. Growth of the Global Pet Blood Glucose Monitoring System Market is driven by rising incidences of diabetes in pets, increasing awareness of early disease detection, and expanding pet ownership worldwide. Higher spending on veterinary care, advancements in glucose monitoring technologies such as continuous monitoring devices, and growing preference for home-based pet health management further support market expansion. Additionally, improved veterinary infrastructure and greater availability of specialized diagnostic products contribute to sustained market growth.

The Global Pet Blood Glucose Monitoring System Market is experiencing strong momentum driven by technological innovation, increasing adoption of continuous glucose monitoring systems, and growing integration of digital health tools for pets. Remote monitoring apps, Bluetooth-enabled meters, and data analytics platforms are enhancing accuracy and convenience for pet owners and veterinarians. Rising emphasis on preventive care and early disease detection continues to expand demand for advanced diagnostics.

Segmentation: The Global Pet Blood Glucose Monitoring System Market is segmented by Animal Type (Canine (Dogs), Feline (Cats) and Other Animals), Product Type (Traditional Blood Glucose Meters (BGM), Continuous Glucose Monitoring (CGM) Systems and Consumables (Strips, Lancets, etc.)), End-User (Veterinary Hospitals & Clinics and Home Care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Rising prevalence of diabetes in pets, particularly dogs and cats, is a major driver of the Global Pet Blood Glucose Monitoring System Market. Increasing obesity rates, aging pet populations, and lifestyle changes contribute to higher diabetes incidence, prompting greater need for accurate and timely glucose monitoring. As more pets are diagnosed, veterinarians emphasize continuous and home-based glucose tracking to prevent complications and improve treatment outcomes. This growing medical necessity encourages pet owners to adopt advanced glucose meters, test strips, and continuous glucose monitoring systems. Awareness campaigns and improved diagnostic capabilities further support early detection, increasing demand for monitoring solutions and driving sustained market growth across both developed and emerging regions.

The growing trend of pet humanization, where pets are viewed as family members, is significantly driving the adoption of advanced glucose monitoring systems. Pet owners are increasingly willing to invest in high-quality healthcare products, including real-time monitoring devices, pet-specific glucometers, and premium diagnostic solutions. Rising disposable incomes, expanding access to veterinary services, and increased availability of specialized pet insurance plans further support this shift. Owners seek convenient at-home testing options that enhance comfort and reduce stress for diabetic pets. Additionally, manufacturers are developing more user-friendly, accurate, and digital-enabled devices to meet these expectations. This heightened focus on preventive care and chronic disease management continues to accelerate market demand for effective glucose monitoring technologies.

Market Restraints:

A key restraint in the Global Pet Blood Glucose Monitoring System Market is the high cost associated with advanced monitoring technologies, particularly continuous glucose monitoring (CGM) systems. These devices require sensors, transmitters, and regular maintenance, making them expensive for many pet owners. Additionally, recurring costs of test strips and replacement parts for traditional glucometers can burden long-term disease management. Limited insurance coverage in several regions further increases out-of-pocket expenses, discouraging adoption among cost-sensitive consumers. Veterinary clinics in developing markets may also face challenges in investing in advanced diagnostic tools due to budget limitations. As a result, high upfront and ongoing costs can restrict widespread use of sophisticated monitoring systems, slowing market penetration in certain segments.

Socioeconomic factors significantly shape the Global Pet Blood Glucose Monitoring System Market by influencing consumer spending patterns and access to veterinary care. Growing disposable incomes and the ongoing trend of pet humanization encourage owners to invest in advanced diagnostic tools and long-term disease management solutions for diabetic pets. Increased urbanization and lifestyle shifts contribute to higher diabetes prevalence in pets, prompting greater reliance on monitoring systems. Improved veterinary infrastructure in developing regions enhances accessibility to diagnostic technologies. At the same time, rising awareness campaigns and supportive pet insurance policies help reduce financial barriers, enabling broader adoption of glucose monitoring devices globally.

Segmental Analysis:

The canine segment is expected to witness the highest growth over the forecast period due to the rising incidence of diabetes in dogs, increasing pet ownership, and growing awareness among dog owners regarding early detection of chronic conditions. Dogs are more frequently diagnosed with diabetes than many other companion animals, driving demand for accurate and user-friendly glucose monitoring systems. Veterinary professionals also emphasize routine glucose testing for diabetic dogs, supporting higher adoption of home-use glucometers and continuous monitoring devices. Increased spending on canine healthcare, coupled with advancements in pet-specific diagnostic technologies, further accelerates segment expansion. Additionally, the growing trend of pet humanization encourages owners to invest in premium diabetes care solutions, strengthening the growth outlook for canine glucose monitoring.

The Continuous Glucose Monitoring (CGM) Systems segment is expected to experience the highest growth during the forecast period due to its superior accuracy, real-time data capabilities, and reduced need for frequent blood sampling. These systems offer continuous insights into glucose fluctuations, enabling better management of diabetic pets and early detection of hypoglycemic or hyperglycemic episodes. Growing technological advancements, such as wireless sensors, smartphone integration, and data-sharing with veterinarians, are increasing adoption rates among pet owners. As pet diabetes cases rise globally, CGM devices provide convenience and improved disease management compared to traditional meters. Their ability to minimize stress in pets, enhance treatment outcomes, and support remote monitoring further contributes to strong market growth in this segment.

The veterinary hospitals and clinics segment is projected to witness the highest growth over the forecast period due to the increasing demand for professional diagnostics and comprehensive diabetes management in pets. Clinics serve as key diagnostic and treatment hubs, offering advanced glucose monitoring services, continuous monitoring device installations, and regular check-ups. Rising awareness of early disease detection and increased frequency of veterinary visits support segment expansion. Moreover, veterinarians play a crucial role in recommending and validating glucose monitoring devices, driving trust and adoption among pet owners. Growing investments in veterinary infrastructure, enhanced availability of specialized endocrinology services, and widespread access to trained professionals make clinics essential for accurate monitoring and long-term management of diabetic pets.

The North America region is expected to witness the highest growth over the forecast period due to high pet ownership rates, strong awareness of pet health, and widespread access to advanced veterinary care.

The region benefits from early adoption of innovative technologies such as continuous glucose monitoring systems, smartphone-integrated devices, and specialized diagnostic tools. Increasing prevalence of diabetes in pets, rising expenditure on veterinary services, and robust presence of leading market players further support regional dominance. For instance, in August 2025, Lifecare ASA reported reaffirmed positive findings from its ongoing veterinary study evaluating a next-generation Continuous Glucose Monitoring (CGM) technology, reinforcing its progress toward commercial launch. The results validate the device’s safety, biocompatibility, and long-term usability. This development is expected to significantly advance the Global Pet Blood Glucose Monitoring System Market by accelerating innovation in long-term, minimally invasive CGM solutions. Lifecare’s technology could expand clinical adoption, enhance monitoring accuracy, and boost veterinarian and pet-owner confidence in continuous monitoring devices. As a result, competition may intensify, encouraging further technological advancements and broadening availability of premium glucose management options for diabetic pets in this region.

Additionally, pet insurance coverage is more prevalent in North America, reducing the financial burden of chronic disease management. Well-established veterinary networks, strong research initiatives, and high consumer willingness to invest in premium pet healthcare solutions contribute to sustained market growth. For instance, NAPHIA’s 2024 State of the Industry report, 6.25 million pets are insured in North America, up 16.6% from 5.36 million in 2022. Rising pet adoption and increasing prevalence of chronic diseases drive global pet insurance growth, helping owners manage high veterinary costs for serious conditions. Demand for advanced treatments and specialized care further boosts insurance adoption and veterinary service utilization. Thus, such factors are expected to drive the market growth in this region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Pet Blood Glucose Monitoring System Market is defined by strong rivalry among established veterinary diagnostic companies, emerging health-tech startups, and global pet care brands. Key players compete through continuous innovation, product accuracy improvements, and expansion of digital capabilities such as mobile data tracking and AI-driven health insights. Strategic partnerships with veterinary clinics, distributors, and telehealth providers further strengthen market presence. Companies increasingly focus on developing cost-effective, user-friendly monitoring solutions to capture the growing home-care segment. Additionally, mergers, acquisitions, and regional expansions are common strategies used to enhance portfolios and maintain competitive advantages across global markets.

The major players for above market:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the rising prevalence of pet diabetes, particularly in aging and obese dogs and cats, which requires continuous glucose management. Pet owners are increasingly treating their companion animals like family members, leading to a rise in pet healthcare expenditure and demand for advanced veterinary care. Additionally, the shift towards at-home monitoring driven by the convenience and reduced stress for pets (compared to clinic visits) is pushing the adoption of user-friendly monitoring devices, fueling market expansion.

Q2. What are the main restraining factors for this market?

The biggest constraint is the high cost of monitoring supplies, including the specific meters, test strips, and specialized needles designed for pets, making long-term management expensive for many owners. Another significant hurdle is owner compliance and the technical difficulty of performing routine venipuncture on pets at home, leading to inaccurate results or inconsistency. Furthermore, the lack of standardized veterinary guidelines and limited awareness in some regions about the necessity of frequent glucose monitoring can also slow down the widespread adoption of these systems.

Q3. Which segment is expected to witness high growth?

The Continuous Glucose Monitoring (CGM) Segment is anticipated to witness the highest growth. While traditional glucose meters require repeated blood sampling, CGM devices use a sensor inserted under the pet's skin to provide real-time, continuous data without repeated skin pricks. This technology offers superior accuracy and comprehensive data on glucose trends, allowing veterinarians and owners to adjust insulin and diet more effectively. The reduced stress for the pet and the convenience for the owner are making CGM the preferred, next-generation monitoring solution.

Q4. Who are the top major players for this market?

The market is led by companies that focus on both animal health and human medical diagnostics, often leveraging existing technology platforms. Top major players include Zoetis, which has a strong presence in animal pharmaceuticals; Bayer AG (now Elanco for certain animal health products); Abbott Laboratories, known for its FreeStyle Libre CGM technology adapted for pets (e.g., FreeStyle Libre Flash Glucose Monitoring System); and Arkray, Inc. These companies compete through product innovation, strategic veterinary partnerships, and educational initiatives for pet owners.

Q5. Which country is the largest player?

The United States, within the North American region, holds the largest market share. This dominance is due to several factors, including the high rate of pet ownership, the high incidence of pet obesity and diabetes, and the enormous pet health insurance penetration. U.S. pet owners spend significantly more on advanced veterinary care than those in most other regions, leading to faster adoption of premium monitoring systems like CGMs. The robust presence of key industry players and veterinary specialists also solidifies the country's market leadership.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model