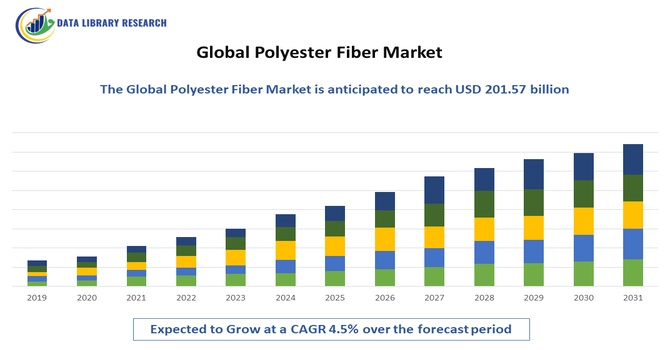

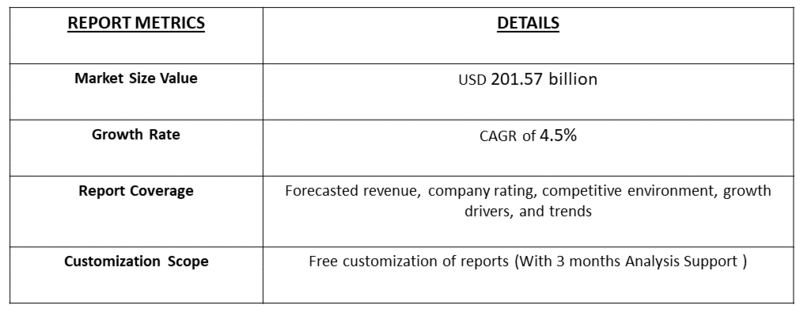

The global polyester fiber market size was estimated at USD 121.51 billion in 2025 and is projected to reach USD 201.57 billion by 2032, growing with a CAGR of 4.5% from 2025 to 2032.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Polyester fiber is a synthetic fiber made from petrochemical-based polymers, primarily polyethylene terephthalate (PET). It is known for its strength, durability, wrinkle resistance, and affordability, making it one of the most widely used fibers in textiles, apparel, home furnishings, and industrial applications. Increasingly, recycled polyester from plastic waste is being adopted to reduce environmental impact. @@ Latest Trends: The trends in the polyester fiber market are being driven by its use in advanced composite materials. The major trends highlighted are its expansion into high-tech industries like automotive, aircraft, marine, and renewable energy, moving far beyond traditional consumer products. This is because it offers a powerful combination of being both high-performance (with impressive mechanical properties) and low-cost. There is significant and ongoing research and development focused on creating new and improved polyester resin composites. The goal of this innovation is to design materials with specific, tailored properties for specialized applications, pushing technology forward in various fields. A central and growing focus of this development is on creating more durable and sustainable solutions for the future.

Segmentation:

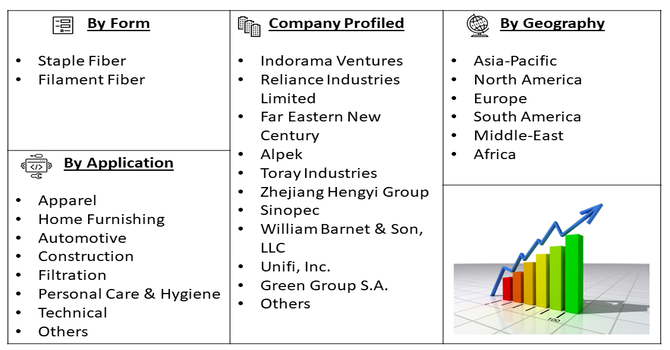

The Global Polyester Fiber Market is Segmented by Form (Staple Fiber, and Filament Fiber), Application (Apparel, Home Furnishing, Automotive, Construction, Filtration, Personal Care & Hygiene, Technical, and Others), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary driving factor for advancing bio-based polyester composites is the urgent need to develop sustainable alternatives to conventional petroleum-based materials. This push is fueled by environmental concerns, demanding a shift towards circular economies.

Key drivers include innovating cost-effective production methods, creating ecologically sound material designs, and securing policy support for commercialization. For instance, in May 2025, HUGO BOSS unveiled NovaPoly, an innovative recycled polyester yarn it co-develops with suppliers Jiaren Chemical Recycling and NBC LLC. Holding the trademark and exclusive usage rights for a year, the brand aims to set a new industry standard and plans to license the technology across the fashion sector. As part of its sustainability initiative, the first products featuring NovaPoly launch globally in October 2025. This directly impacts the polyester market by accelerating the shift from virgin to recycled PET. It creates a new, branded, high-value circular product, setting a technical benchmark that competitors must match, thereby raising sustainability standards and increasing demand for advanced chemical recycling technologies.

Thus, interdisciplinary collaboration across science and engineering is crucial to expand the industrial applications of these sustainable materials and successfully integrate them into future technologies. @@ Increasing Consumer Purchasing Power.

Another driving factor for the shift towards eco-friendly textiles is heightened consumer awareness and demand. Motivated by environmental concerns, a sense of social responsibility, and health considerations, consumers globally are actively seeking sustainable options. This market pull is compelling the industry to innovate and adapt. For instance, in October 2024, PUMA joined a multi-brand consortium that unveils the world’s first garment made entirely from textile waste. It utilizes a novel biorecycling technology from CARBIOS. This process employs enzymes to break down polyester waste into its core building blocks, producing a biorecycled polyester fiber. This development is a direct response to growing consumer purchasing power demanding sustainable products. It validated enzymatic recycling as a viable, high-quality solution for fiber-to-fiber recycling, moving beyond mechanical methods. This technological breakthrough pressures the entire market to innovate, accelerating the shift from a linear to a circular economy and reducing the industry's dependence on virgin petroleum-based polyester.

The industry is therefore driven to invest in cost-effective sustainable supply chains, pursue credible certifications to build trust, and leverage digital education to overcome barriers of affordability and availability, ultimately making green textiles more mainstream.

Market Restraints:

A significant restraint hindering the faster growth of the recycled polyester fiber market is the substantial economic and infrastructural challenge of establishing a closed-loop recycling system. The current collection, sorting, and processing of post-consumer textile waste remains highly inefficient and costly. Unlike PET bottles, textiles are often blended with other fibers and contaminated with dyes and chemicals, making them difficult and expensive to separate and purify for high-quality recycling. This complexity creates a supply bottleneck for clean, homogeneous waste feedstock.

Consequently, the production cost for recycled polyester often exceeds that of its virgin counterpart, which benefits from established, economies-of-scale fossil fuel supply chains, limiting price competitiveness and widespread adoption despite consumer demand.

The polyester fiber market has a complex and significant impact on our world. It creates jobs globally, from manufacturing to retail, and provides affordable clothing that billions of people rely on. However, its reliance on petroleum makes it vulnerable to unpredictable fossil fuel prices, which can affect its cost stability. A growing push for sustainability has led to a shift towards using recycled polyester, which creates new "green jobs" in waste management and recycling and promotes a more circular economy. Despite these benefits, the higher cost of recycled materials presents a new challenge: it can make sustainable products less accessible for low-income consumers, potentially creating a disparity in who can afford to participate in eco-friendly consumption. This dynamic highlights the need to balance economic accessibility with environmental progress.

Segmental Analysis:

The staple fiber segment is poised for substantial growth, primarily driven by its extensive use in the non-woven fabrics industry. This demand is fueled by the rapidly expanding personal care and hygiene sector, which relies heavily on non-wovens for products like baby diapers, wipes, and feminine hygiene items. Furthermore, staple fibers are indispensable in traditional applications such as spinning yarn for apparel and home furnishings like carpets and upholstery. Their versatility, cost-effectiveness, and adaptability to be blended with other natural and synthetic fibers make them a preferred choice for manufacturers aiming to meet the rising global demand for both technical and conventional textile products, ensuring their market expansion.

The personal care and hygiene segment is projected to experience significant growth, as it is a major consumer of non-woven fabrics made from polyester staple fiber. Key drivers include rising global populations, increasing disposable incomes in emerging economies, and heightened health and wellness awareness post-pandemic. The demand for premium, disposable hygiene products like diapers, adult incontinence products, and sanitary napkins is surging. Polyester is favored for its high strength, durability, absorbency, and cost efficiency compared to alternatives. This consistent, high-volume demand from an essential goods sector makes it a resilient and rapidly growing end-use market for polyester fiber producers.

The Asia Pacific region is unequivocally the dominant and fastest-growing market for polyester fiber. This growth is anchored by massive textile manufacturing hubs in China, India, and Southeast Asia, which benefit from cost-competitive labor, well-established supply chains, and significant production capacities.

Furthermore, the region itself is a booming consumption market, fueled by a growing middle class with increasing purchasing power, rapid urbanization, and expanding retail sectors. For instance, in August 2025, Loop Industries' Indian joint venture reached an agreement to acquire a key site in Gujarat for its Infinite Loop manufacturing facility, marking a significant step in the project's development. The land, costing USD 10.5 million, came in at a lower price than initially projected, providing a USD 5 million saving on the total capital cost. This development is expected to significantly impact the Asia-Pacific polyester fiber market by promoting a more circular economy. By establishing a facility in Gujarat—a major textile hub—the company gained direct access to a huge source of polyester textile waste, which it plans to recycle into virgin-quality material. This initiative will reduce the region's reliance on new petroleum-based fibers, cut down on environmental waste, and position the company to meet the rising demand for sustainable and recycled materials from major global brands.

Thus such rising demand for affordable apparel, home textiles, and hygiene products coupled with such investments is significant growth driver of this market in the region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global polyester fiber market is intensely fragmented and highly competitive, characterized by the presence of numerous established global players and low-cost regional manufacturers. Key companies like Indorama Ventures, Reliance Industries, and Far Eastern New Century dominate through extensive backward integration, controlling production from raw materials to finished fiber, which ensures cost leadership and supply chain resilience. Competition primarily revolves on production cost efficiency, product innovation—particularly in developing sustainable and recycled fibers—and expanding application reach into technical and non-woven sectors. Strategic activities include capacity expansions in Asia-Pacific, partnerships for recycling technologies, and mergers and acquisitions to consolidate market share and enhance geographic and product portfolio diversification.

Here are list of 10 major players for above market:

Recent Developments:

Q1. What the main growth driving factors for this market?

The market is mainly driven by rising demand in textiles, apparel, and home furnishings due to polyester’s affordability, strength, and easy maintenance. Increasing use of recycled polyester, government support for circular economy initiatives, and large-scale capacity expansions in Asia further fuel growth across global textile and industrial applications.

Q2. What are the main restraining factors for this market?

Environmental concerns about plastic waste, microfibers, and high carbon emissions restrain growth. Regulations in Europe and North America are pushing for sustainable alternatives. Price fluctuations of petrochemical feedstock also create market instability. Recycling challenges, including sorting and cost, limit the pace of adoption and hinder smooth growth worldwide.

Q3. Which segment is expected to witness high growth?

Recycled polyester fiber is expected to see the fastest growth due to sustainability commitments from global brands and consumer demand for eco-friendly fabrics. Polyester staple fiber (PSF) is also expanding quickly, especially in apparel, bedding, and nonwovens, supported by affordable costs and versatile applications across industries worldwide.

Q4. Who are the top major players for this market?

Key players include Indorama Ventures (Thailand), Reliance Industries (India), Sinopec Yizheng (China), Tongkun Group (China), and Alpek (Mexico). These companies dominate global production capacity, supplying both virgin and recycled polyester. Their expansion strategies, technological improvements, and investments in sustainable polyester strengthen their leadership in this competitive market.

Q5. Which country is the largest player?

China is the world’s largest producer and consumer of polyester fiber. It accounts for the majority of global output due to its vast manufacturing base, cost advantages, and established supply chain. The country is also leading in recycled polyester adoption, supporting growth in apparel, industrial, and technical textile sectors.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model