Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Recreational Vehicle (RV) Chassis Market refers to the worldwide industry involved in the design, manufacture, and sale of the structural frameworks that serve as the foundation for recreational vehicles such as motorhomes, camper vans, and trailers. This market encompasses various types of chassis including motorized and towable platforms, catering to diverse consumer demands for travel and leisure. Driven by rising tourism, increasing disposable incomes, and a growing preference for outdoor and mobile lifestyles, the market is characterized by advancements in lightweight materials, enhanced safety features, and integration of smart technologies. Key players operate across regions to meet the expanding demand for durable, versatile, and efficient RV chassis solutions, making this market a critical segment within the broader automotive and recreational industries.

The Global RV Chassis Market is witnessing notable trends driven by evolving consumer preferences and technological innovation. Lightweight and fuel-efficient chassis are increasingly in demand, aligning with global sustainability goals and rising fuel costs. Electrification is gaining momentum, with manufacturers exploring hybrid and fully electric RV platforms. Smart technologies, including integrated telematics, advanced driver-assistance systems (ADAS), and real-time diagnostics, are becoming standard features. Additionally, the surge in remote work culture and digital nomadism has fueled interest in mobile living, prompting demand for customizable and multifunctional RV chassis. The market is also seeing growth in modular chassis designs to support a variety of RV configurations, enabling greater flexibility and catering to the increasing popularity of outdoor and adventure travel lifestyles.

Segmentation: The Global Recreational Vehicle (RV) Chassis Market is segmented by Type (RVS and Motorhomes), Application (Domestic and Commercial), Propulsion (Internal Combustion Engine (ICE), Hybrid, and Battery Electric), Length (Below 20 Ft, 20–30 Ft, and Above 30 Ft), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing popularity of outdoor recreation and mobile living is a significant driver for the RV chassis market. Consumers, particularly millennials and retirees, are seeking flexible travel options that offer autonomy, affordability, and a closer connection to nature. The post-pandemic era accelerated this trend, as travelers turned away from crowded hotels and airports in favor of self-contained, road-based travel. RVs—especially motorhomes and camper vans—allow for social distancing, remote work, and extended family vacations. This shift in lifestyle preferences has boosted RV sales and, by extension, the demand for robust, reliable, and customizable chassis platforms that can support various configurations and amenities, encouraging manufacturers to innovate and diversify their offerings to meet evolving consumer needs.

Technological innovations in chassis design are driving significant growth in the RV industry. Advances in lightweight materials, electric drivetrains, and integrated safety systems are making RVs more efficient, durable, and user-friendly. Modern chassis are now engineered for better fuel economy, higher load-bearing capacity, and smoother ride quality. The introduction of electric and hybrid chassis also reflects a growing focus on sustainability and regulatory compliance, particularly in North America and Europe. Features such as modular architecture, advanced suspension systems, and digital monitoring tools enhance the overall value proposition for both manufacturers and consumers. These developments not only expand the design possibilities for RVs but also reduce operational costs, making RV ownership more accessible and appealing to a broader demographic.

Market Restraints:

The key restraints facing the global RV chassis market is the tightening of regulatory controls and urban parking restrictions, especially in major cities across North America and Europe. As urban populations grow, municipalities are increasingly limiting the use and storage of large vehicles like motorhomes on public streets and residential zones. These restrictions can deter potential buyers who lack private storage or who live in urban environments where RV use is impractical. Furthermore, emissions regulations are placing added pressure on manufacturers to transition to cleaner chassis technologies, which increases production costs. These legal and logistical barriers could slow the adoption of larger RVs and affect demand for specific chassis sizes, particularly in densely populated or regulated regions.

The RV chassis market plays a significant socio-economic role, particularly in regions where tourism, outdoor recreation, and mobile living are integral to local economies. Increased consumer interest in RV travel supports job creation across manufacturing, retail, maintenance, and tourism sectors. The market benefits from rising disposable incomes and changing lifestyles, particularly among retirees and younger travelers seeking affordable, flexible alternatives to traditional vacations. It also stimulates local economies as RV travelers often spend in rural and remote areas that typically see less tourist activity. Furthermore, the RV lifestyle's appeal during crises—such as pandemics—highlights its value in promoting social distancing while sustaining travel. The market's expansion reflects a broader shift toward experience-driven consumption and supports both economic growth and personal well-being.

Segmental Analysis:

The motorhomes segment is projected to experience the highest growth in the RV chassis market due to rising consumer demand for all-in-one mobile living solutions. Motorhomes offer enhanced convenience, mobility, and luxury, making them especially appealing for extended travel and full-time RV lifestyles. Advances in chassis technology have improved fuel efficiency, handling, and durability, further boosting adoption. Additionally, increased interest in domestic tourism, especially post-pandemic, has shifted consumer preferences toward motorized RVs over towables. The surge in remote work and digital nomadism also supports demand for self-contained, drivable units. North America and Europe are key regions driving this growth, with strong infrastructure, disposable income, and a growing population of retirees seeking flexible travel options.

The commercial segment within the RV chassis market is expected to register the highest growth due to expanding applications in mobile offices, medical units, food trucks, and rental fleets. Businesses are increasingly adopting customized RVs to serve remote and temporary locations, leveraging their mobility and self-sufficiency. Post-pandemic, mobile healthcare services and testing labs gained popularity, further validating RVs as viable commercial assets. Additionally, the event and tourism industries are investing in commercial RVs for transport, hospitality, and promotional purposes. Rental companies are also expanding fleets to meet growing demand from travelers who prefer short-term RV use without ownership. This trend is especially strong in urban centers and tourism hotspots, where mobile services offer cost-effective, flexible, and scalable solutions.

Despite the rise of electrification, the Internal Combustion Engine (ICE) segment is expected to dominate the RV chassis market over the forecast period, driven by existing infrastructure, affordability, and long-range capabilities. ICE-powered RVs offer extensive fueling networks, well-established maintenance ecosystems, and higher towing capacities, making them ideal for long-distance travel and heavy-duty applications. Many consumers, especially in North America, prefer diesel and gasoline engines due to familiarity and availability. Additionally, innovations in cleaner ICE technologies and compliance with stricter emission norms are helping prolong the segment’s relevance. While electric and hybrid models are gaining interest, ICE continues to be the most practical and cost-effective solution for most RV manufacturers and buyers in the current market landscape.

The 20–30 ft RV chassis segment is poised for the highest growth, owing to its balance between maneuverability and space. This length category is ideal for families and couples seeking compact, yet comfortable living spaces without sacrificing drivability. It caters to both first-time RV buyers and experienced users looking to downsize without losing core amenities. RVs in this segment can access a wider range of campsites and parking spots, making them versatile for diverse travel needs. Manufacturers are increasingly focusing on this size range to meet growing demand, offering advanced features and lightweight chassis to improve performance and fuel efficiency. This segment’s affordability, practicality, and increasing popularity among younger travelers further contribute to its robust growth outlook.

North America is expected to lead the RV chassis market growth, supported by a strong RV culture, extensive road infrastructure, and high disposable incomes. The U.S. and Canada together represent a mature yet expanding market, with increasing interest in outdoor recreation, especially post-pandemic. Consumer trends favoring mobile lifestyles, remote work, and family-oriented travel have accelerated demand for both motorhomes and towables.

Additionally, a well-established RV manufacturing base, major players like Thor and Winnebago, and robust dealership networks enhance regional growth. For instance, in April 2024, the Los Angeles City Council expanded its overnight parking restrictions by adding 30 more streets where recreational vehicles longer than 22 feet are prohibited from parking between 2 a.m. and 6 a.m. This regulation is part of ongoing efforts to address street congestion and community concerns related to long-term RV parking in residential areas. This development highlights growing regulatory pressure in urban centers across North America concerning large recreational vehicles. Restrictions like these may influence consumer behavior, with potential buyers opting for smaller RVs under 22 feet, leading to a shift in chassis demand toward compact and lightweight platforms. It could also drive increased interest in towable RVs or Class B and C motorhomes that are easier to park and maneuver. For manufacturers, adapting to changing urban policies may mean prioritizing modular, city-friendly chassis designs and promoting innovations that balance size with livability. Long-term, such regulations could reshape regional product strategies and fuel demand for RVs tailored to tighter parking and zoning laws.

Government incentives for tourism and infrastructure development also support this market. With innovations in ICE and growing interest in hybrid models, North America remains the most lucrative region, attracting investment and innovation across the RV chassis value chain.

| Report Matrics | Details |

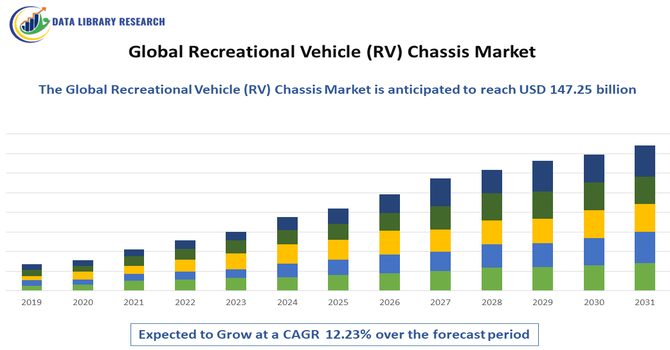

| Market Size Value | USD 147.25 billion |

| Growth Rate | CAGR of 12.23% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global RV Chassis Market is marked by the presence of both established automotive giants and specialized chassis manufacturers. Key players such as Ford, Mercedes-Benz, Fiat Chrysler, and Freightliner dominate the motorized segment, while companies like AL-KO and Lippert Components lead in towable chassis solutions. Intense competition is pushing firms to innovate through electric drivetrains, weight reduction techniques, and smart integration. Partnerships between chassis manufacturers and RV assemblers are growing, fostering customization and faster go-to-market strategies. Startups and regional players are also emerging, particularly in Asia-Pacific and Europe, capitalizing on local market demands. Competitive dynamics are further influenced by regulatory standards around emissions and safety, encouraging R&D investments and strategic expansions into emerging markets.

The 20 major players for above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The primary growth drivers are the surging consumer interest in outdoor tourism, road trips, and flexible travel, particularly among millennials and Gen Z. Rising disposable incomes globally enable more people to invest in RVs. Furthermore, the increasing adoption of the "van life" and remote work trends, which necessitate a mobile living and working space, fuels demand for specialized chassis. Technological advancements in chassis design for improved fuel efficiency, safety features (like ADAS), and the push toward electric RV platforms also stimulate market expansion.

Q2. What are the main restraining factors for this market?

Major restraining factors include the high initial and maintenance costs associated with RV ownership, which deters budget-conscious consumers. Fluctuations in raw material prices, particularly for steel and aluminum used in chassis manufacturing, increase production costs and final vehicle prices. Additionally, an insufficient charging infrastructure for the emerging electric RV segment and the impact of economic downturns, which reduce discretionary spending on luxury items like RVs, pose significant market hurdles.

Q3. Which segment is expected to witness high growth?

The Motorhome Chassis segment, particularly for Class B and C motorhomes, is expected to witness high growth. Class B (camper van) chassis are highly sought after due to the "van life" trend, their compact size, and ease of driving and parking. The market is also seeing rapid growth in chassis designed for electric/hybrid RVs, driven by stringent emission regulations and growing consumer preference for sustainable travel, which necessitates specialized EV-ready chassis.

Q4. Who are the top major players for this market?

The RV Chassis market is dominated by a few major automotive and specialized chassis manufacturers that supply to RV builders. The top major players include Ford Motor Company (for their E-Series and Transit chassis), Fiat Chrysler Automobiles (Stellantis) (especially with the Fiat Ducato/Ram ProMaster chassis popular in Europe/North America), and Mercedes-Benz (with the Sprinter chassis). Specialized RV component suppliers like Freightliner Custom Chassis Corporation and Oshkosh Corporation are also key players for larger motorhomes.

Q5. Which country is the largest player?

The United States is the largest and most established country-level market player for the RV Chassis market, supported by a deep-rooted RV culture, vast road network, and a large population of outdoor enthusiasts. North America, as a whole (including the US and Canada), dominates in terms of overall RV sales and subsequent chassis demand. The region has the highest concentration of major RV manufacturers and a strong culture of using large motorhomes and towable RVs.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model