Get Complete Analysis Of The Report - Download Updated Free Sample PDF

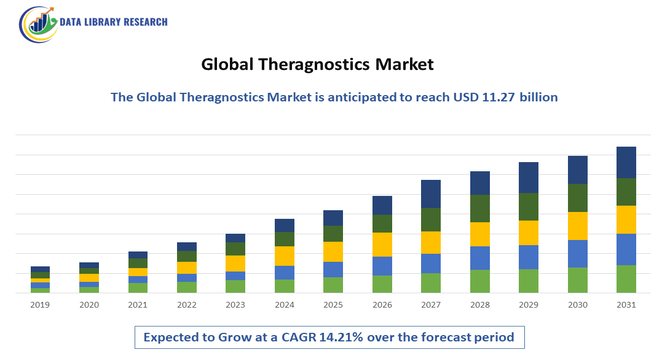

The global theragnostics market refers to the integrated field combining diagnostics and targeted therapy to enable personalized healthcare. It focuses on identifying specific biomarkers through advanced imaging, molecular diagnostics, and companion tests, then delivering therapies tailored to an individual patient’s disease profile. Widely applied in oncology, cardiology, neurology, and rare diseases, theragnostics improves treatment accuracy, reduces adverse effects, and enhances clinical outcomes. The market encompasses radiopharmaceuticals, imaging agents, diagnostic assays, and targeted therapeutics, supported by advances in genomics, artificial intelligence, and precision medicine.

The global theragnostics market is driven by rapid advancements in precision medicine, molecular imaging, and biomarker discovery. Integration of artificial intelligence and machine learning enhances diagnostic accuracy and treatment decision-making. Increasing R&D in radiopharmaceuticals, coupled with regulatory approvals of novel theragnostic agents, bolsters market growth. Personalized oncology remains a key focus, with expanding applications in cardiovascular and neurological disorders. Collaboration between pharmaceutical and diagnostic firms accelerates companion diagnostic development.

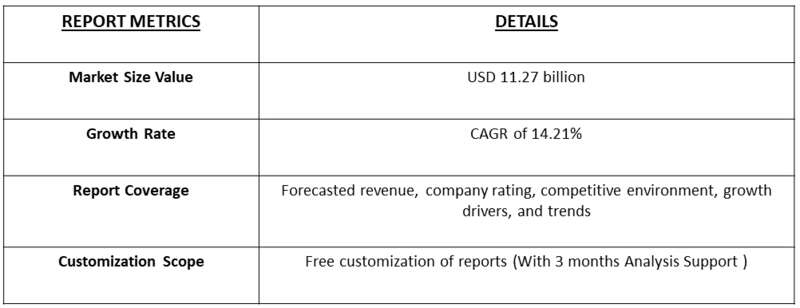

Segmentation: The global theragnostics market is segmented by Product Type (Diagnostic Agents, Therapeutic Agents, Radiopharmaceuticals and Companion Diagnostics), Technology (Nuclear Imaging (PET, SPECT), Molecular Imaging, Genomics & Proteomics and In-vitro Diagnostics), Application (Oncology, Cardiology, Neurology, Orthopedics, Infectious Diseases and Rare Diseases), End User (Hospitals, Diagnostic Imaging Centers, Specialty Clinics and Research Institutes & Academic Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing shift toward personalized medicine is a major driver of the global theragnostics market. Healthcare providers increasingly focus on tailoring treatments based on a patient’s genetic, molecular, or biomarker profile to improve clinical outcomes. Theragnostics enables precise disease identification and targeted therapy selection, particularly in oncology, where treatment response varies significantly among patients. This approach reduces trial-and-error prescribing, minimizes adverse effects, and improves treatment efficiency. Increasing awareness among clinicians and patients about the benefits of individualized care, along with supportive regulatory frameworks for precision medicine, continues to accelerate adoption of theragnostic solutions worldwide.

Rapid technological advancements in imaging systems, radiopharmaceuticals, genomics, and molecular diagnostics are strongly driving market growth. Innovations in PET and SPECT imaging, coupled with improved biomarkers and targeted radiotherapies, enhance diagnostic accuracy and therapeutic effectiveness. For instance, in December 2025, the collaboration between Telix and Varian advanced imaging and molecular technologies and boosted the global theragnostics market by integrating theranostics with radiation therapy, enhancing treatment precision, and supporting personalized oncology care.

Artificial intelligence and data analytics further support precise interpretation of complex diagnostic data. These advancements expand theragnostic applications beyond oncology into cardiology, neurology, and rare diseases. Continuous investment in research and development by pharmaceutical and biotechnology companies, along with academic collaborations, is accelerating innovation, improving clinical validation, and increasing the availability of advanced theragnostic products globally.

Market Restraints:

High development, production, and implementation costs remain a key restraint for the global theragnostics market. Advanced imaging equipment, radiopharmaceutical manufacturing, and specialized infrastructure require significant capital investment. Additionally, theragnostic procedures often involve complex regulatory approvals and skilled professionals, increasing overall healthcare costs. These factors limit adoption in low- and middle-income regions and smaller healthcare facilities. Reimbursement challenges and unequal access to advanced diagnostic technologies further restrict market penetration. Without broader insurance coverage and cost-effective solutions, the widespread adoption of theragnostics may remain uneven across different geographic and socioeconomic settings.

Theragnostics significantly influences healthcare outcomes and economic frameworks by promoting personalized treatment, reducing ineffective therapies, and improving patient quality of life. Earlier and more precise diagnoses lower overall treatment costs through targeted interventions and reduced hospital stays. This approach benefits aging populations and patients with chronic diseases, particularly in oncology where tailored treatments enhance survival rates. Economies with advanced healthcare infrastructure see increased investment in high-tech diagnostics and skilled workforce development. However, equitable access remains a concern in lower-income regions due to high technology costs. Policymakers and stakeholders must address affordability and infrastructure gaps to ensure widespread socioeconomic benefits of theragnostics.

Segmental Analysis

The radiopharmaceuticals segment is expected to witness the highest growth over the forecast period due to increasing adoption of targeted nuclear therapies and advanced diagnostic imaging. These agents enable precise tumor localization, real-time disease monitoring, and targeted treatment delivery, especially in oncology. Growing approvals of novel radioligand therapies, rising investments in nuclear medicine infrastructure, and expanding clinical applications drive segment growth. Additionally, technological advancements in isotope production and imaging modalities such as PET and SPECT enhance clinical efficiency. Increasing prevalence of cancer and demand for personalized, minimally invasive treatment options further accelerate growth of the radiopharmaceuticals segment globally.

The genomics and proteomics segment is expected to experience the highest growth over the forecast period due to its critical role in biomarker identification and precision medicine. Advances in sequencing technologies, bioinformatics, and molecular profiling enable accurate disease characterization and therapy selection. These tools support early diagnosis and prediction of treatment response, particularly in cancer and rare diseases. Declining sequencing costs, increasing research funding, and growing clinical adoption of companion diagnostics contribute to rapid expansion. Integration of genomics and proteomics with theragnostic platforms enhances personalized care, driving strong demand across healthcare and research settings.

The oncology segment is projected to witness the highest growth over the forecast period, driven by the rising global cancer burden and increasing demand for targeted therapies. Theragnostics plays a crucial role in cancer care by enabling accurate tumor detection, patient stratification, and personalized treatment planning. Radioligand therapies and molecular diagnostics significantly improve treatment outcomes while reducing side effects. Growing clinical evidence supporting theragnostic approaches, along with increased investment in oncology research, accelerates adoption. Additionally, favorable regulatory support for cancer diagnostics and therapeutics further strengthens the growth of the oncology segment worldwide.

The hospitals segment is expected to witness the highest growth over the forecast period due to the increasing integration of advanced diagnostic and therapeutic technologies within hospital settings. Hospitals serve as primary centers for cancer diagnosis, imaging, and treatment, making them key end users of theragnostic solutions. Availability of skilled professionals, advanced infrastructure, and multidisciplinary care teams supports effective implementation. Rising patient volumes, increasing preference for centralized care, and expansion of nuclear medicine departments further drive growth. Additionally, improved reimbursement policies and hospital investments in precision medicine technologies enhance adoption of theragnostics in hospitals.

North America is expected to witness the highest growth over the forecast period due to strong healthcare infrastructure, high adoption of advanced medical technologies, and significant investment in research and development. For instance, in October 2025, INITIO Medical’s recognition as the first ICPO Theranostics Clinical Center of Excellence in North America advanced imaging and molecular technologies by setting high standards in theranostic practices. This accreditation strengthened North America’s theragnostics market by promoting clinical excellence, supporting adoption of cutting-edge diagnostics and targeted therapies, and reinforcing the region’s leadership in precision, patient-centered cancer care.

The region benefits from early adoption of precision medicine, widespread availability of nuclear imaging facilities, and presence of leading market players. High cancer prevalence, favorable regulatory frameworks, and supportive reimbursement policies further drive market growth. For instance, in June 2025, The FDA granted RAD101 fast track designation to accelerate its development and review for distinguishing recurrent brain metastases from treatment effects, including leptomeningeal cases. Targeting fatty acid synthase (FASN), this approval advanced precision imaging, supporting faster clinical adoption and improving diagnostic accuracy in neuro-oncology theranostics.

Additionally, strong collaboration between pharmaceutical companies, research institutions, and healthcare providers accelerates innovation and commercialization of theragnostic solutions across the region.

To Learn More About This Report - Request a Free Sample Copy

The global theragnostics market features competition among pharmaceutical companies, diagnostic developers, and biotechnology firms specializing in targeted therapies and imaging agents. Leading players invest heavily in R&D, strategic collaborations, and mergers to expand product portfolios and secure regulatory approvals. Competition centers on innovation in radiopharmaceuticals, companion diagnostics, and integrated treatment platforms. Larger multinational corporations often partner with academic institutions and research organizations to accelerate clinical trials. Market entry barriers include stringent regulatory pathways and substantial development costs. Emerging companies focus on niche applications and regional markets to differentiate. Ultimately, companies that deliver clinically validated, cost-effective, and scalable theragnostic solutions gain competitive advantage.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the shift toward personalized medicine, where diagnosis and therapy are integrated into a single platform. Rising cancer prevalence and the success of radiopharmaceuticals in treating prostate and neuroendocrine tumors fuel growth. Additionally, advancements in molecular imaging and increased funding for precision oncology research accelerate market adoption.

Q2. What are the main restraining factors for this market?

Growth is hindered by the high cost of developing and implementing theragnostic procedures, which often require expensive specialized equipment and radionuclides. Complex regulatory pathways and the need for seamless coordination between diagnostic and therapeutic teams also pose challenges. Furthermore, limited availability of medical isotopes and specialized training for clinicians restricts widespread use.

Q3. Which segment is expected to witness high growth?

The Oncology segment, particularly Radiopharmaceuticals, is expected to see the highest growth. This is driven by the clinical success of "see-and-treat" pairings like Lutetium-177 for prostate cancer. As more targeted ligands are developed for various solid tumors, the demand for these precision-strike therapies continues to surge in clinical settings.

Q4. Who are the top major players for this market?

The market is led by global pharmaceutical and diagnostic giants. Key players include Novartis (Advanced Accelerator Applications), GE HealthCare, Siemens Healthineers, Thermo Fisher Scientific, and Lantheus Holdings. These companies dominate by securing patents for novel isotopes and integrating advanced imaging technology with innovative therapeutic drug delivery systems.

Q5. Which country is the largest player?

The United States is the largest player in the theragnostics market. Its dominance is supported by a highly advanced healthcare infrastructure, significant investment in biotechnology, and early adoption of FDA-approved radioligand therapies. The presence of leading research institutions and a strong focus on precision medicine keep the U.S. in the lead.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model