Get Complete Analysis Of The Report - Download Updated Free Sample PDF

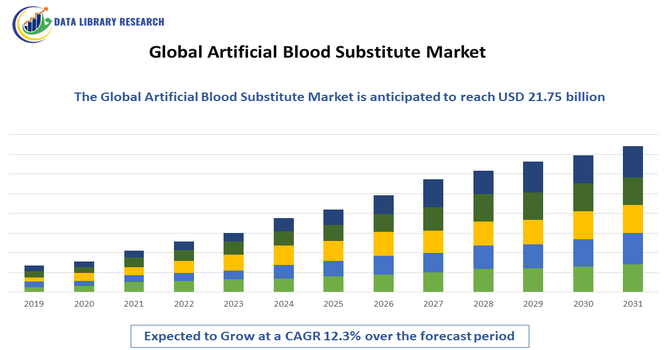

The Global Artificial Blood Substitute Market encompasses the development, production, and distribution of synthetic or biologically engineered products that mimic one or more functions of human blood—especially oxygen transport and volume replacement—when donor blood is unavailable or unsafe. These substitutes include haemoglobin-based oxygen carriers (HBOCs), perfluorocarbon emulsions, engineered red blood cell mimetics, and plasma expanders, used chiefly in emergency, surgical, trauma, and chronic care settings. Growth is driven by persistent blood shortages, increased surgical and trauma cases, ageing populations, and technological advances that improve safety, shelf life, and functionality of substitutes, while addressing limitations of traditional blood transfusions.

Key market trends include accelerating innovation in synthetic biology, nanoparticle-based oxygen carriers, and engineered red cell surrogates that more closely replicate natural blood functions and improve biological compatibility and circulation time. Freeze-dried and ambient-stable formulations are gaining traction, expanding use in emergency, military, and disaster medicine where cold chain limitations exist. Hemoglobin-based oxygen carriers remain dominant, while cell-derived substitutes show rapid growth due to enhanced performance profiles. Regional adoption patterns highlight North America’s substantial share supported by advanced healthcare infrastructure and Asia-Pacific’s fast growth due to urbanisation and expanding healthcare systems.

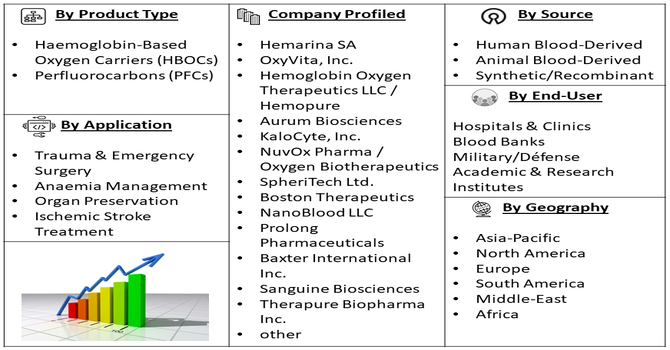

Segmentation: The Global Artificial Blood Substitute Market is segmented by Product Type (Haemoglobin-Based Oxygen Carriers (HBOCs) and Perfluorocarbons (PFCs)), Source (Human Blood-Derived, Animal Blood-Derived and Synthetic/Recombinant), Application (Trauma & Emergency Surgery, Anaemia Management, Organ Preservation and Ischemic Stroke Treatment), End-User (Hospitals & Clinics, Blood Banks, Military/Défense and Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver for the artificial blood substitute market is the persistent global shortage of donor blood. Blood donations in many regions are insufficient to meet rising demands from trauma cases, surgical procedures, chronic diseases, and emergency events, creating urgent supply constraints. Artificial blood substitutes provide universal, readily available alternatives that bypass blood-type matching and donor dependency, enhancing emergency responsiveness and critical care outcomes. Aging populations and increasing surgical volumes amplify demand, particularly in regions with limited blood bank infrastructure. Healthcare systems seeking to mitigate supply risks and improve patient safety further drive investments in artificial substitutes worldwide.

Another significant driver is rapid technological innovation in synthetic biology, nanotechnology, and biotechnology that enhances artificial blood substitute safety, efficacy, and functionality. Advancements in hemoglobin modification, encapsulation techniques, nanoparticle-based oxygen carriers, engineered red cell surrogates, and freeze-dried formulations improve oxygen delivery, circulation stability, and storage life. These improvements make substitutes viable for a broader range of clinical applications, including trauma, surgical support, neonatal care, and chronic anemia management. Increased research funding, clinical trials, and strategic collaborations between biotech firms, academic institutes, and healthcare organisations accelerate development and commercialisation of next-generation artificial blood products.

Market Restraints:

A notable restraint in the artificial blood substitute market is the high cost of development and regulatory hurdles. Manufacturing safe and effective artificial blood products involves complex biotechnological processes, extensive preclinical and clinical trials, and specialised facilities, leading to significant R&D and production expenses. Long and uncertain regulatory approval processes in various jurisdictions delay market entry and increase time-to-market, deterring smaller firms and investors. Safety concerns, including potential immune reactions and long-term effects, necessitate rigorous testing and regulatory scrutiny, further constraining adoption. High product prices may limit accessibility in price-sensitive healthcare systems, especially in low- and middle-income regions.

The artificial blood substitute market yields significant socioeconomic impact by potentially alleviating global blood shortages that burden healthcare systems and limit critical care delivery. By reducing dependence on donor blood, substitutes can lower transmission risks of blood-borne infections and improve outcomes in trauma, surgeries, and chronic diseases, especially in regions with inadequate blood bank infrastructure. Growth supports investments in biotech research, clinical trials, manufacturing, and specialised healthcare roles, creating jobs and advancing medical capabilities. Broader access in emerging markets improves emergency readiness and equity of care. However, high R&D costs and pricing may challenge affordability and access in low-income regions.

Segmental Analysis:

The Haemoglobin-Based Oxygen Carriers (HBOCs) segment is expected to witness the highest growth over the forecast period due to its advanced capability to transport oxygen efficiently without the need for blood-type matching. HBOCs are designed to replicate the oxygen-carrying function of red blood cells while offering longer shelf life and improved storage flexibility compared to donor blood. Their potential use in trauma care, emergency medicine, military settings, and surgical procedures significantly drives demand. Continuous research advancements aimed at improving safety profiles and reducing side effects further strengthen adoption. As regulatory pathways gradually evolve, HBOCs are positioned as the leading technology platform within artificial blood substitutes.

The animal blood-derived segment is projected to experience the highest growth during the forecast period due to its relative technological maturity and scalability compared to fully synthetic alternatives. Products derived from bovine or other animal hemoglobin offer effective oxygen delivery and have undergone more extensive clinical evaluation in certain regions. These substitutes often demonstrate stable performance and cost advantages in comparison to complex recombinant or cell-based technologies. Growing interest in addressing blood shortages, especially in emergency and surgical settings, supports their adoption. Improvements in purification techniques and pathogen inactivation processes have enhanced safety standards, further accelerating market acceptance of animal-derived artificial blood products globally.

The organ preservation segment is expected to witness the highest growth over the forecast period as transplantation procedures increase worldwide. Artificial blood substitutes play a crucial role in maintaining oxygen supply to organs during transport and storage, improving graft viability and patient outcomes. With rising cases of end-stage organ failure and expanding transplant programs, demand for advanced preservation solutions has intensified. Artificial oxygen carriers enhance perfusion quality and extend allowable preservation times compared to conventional solutions. Ongoing innovation in perfusion technologies and cold storage alternatives further supports adoption. As healthcare systems prioritize transplant success rates, this segment is anticipated to demonstrate strong and sustained expansion.

The hospitals and clinics segment is projected to register the highest growth owing to the increasing volume of surgeries, trauma cases, and critical care admissions globally. Artificial blood substitutes offer healthcare providers an alternative during blood shortages, emergency resuscitation, and situations where cross-matching is not feasible. Hospitals are at the forefront of clinical trials and early adoption of innovative oxygen carriers, driving institutional demand. Additionally, improvements in infrastructure, especially in emerging economies, have expanded hospital-based emergency services. As awareness of artificial blood technologies rises among clinicians, and regulatory approvals advance, hospitals and clinics are expected to remain the primary end users of these products.

The North American region is expected to witness the highest growth during the forecast period due to its advanced healthcare infrastructure, strong research ecosystem, and significant investment in biotechnology innovation.

The region experiences substantial trauma and surgical case volumes, driving demand for reliable blood substitutes. For instance, in July 2025, rising pre-hospital trauma deaths in the United States accelerated research into powdered, easily reconstituted artificial blood substitutes. Experimental studies, including hemorrhage simulations at the University of Maryland School of Medicine, advanced emergency-use applications, thereby strengthening innovation momentum and expanding growth prospects in the global artificial blood substitute market.

Supportive funding for clinical research, collaborations between biotech firms and academic institutions, and evolving regulatory frameworks contribute to market expansion. Additionally, preparedness initiatives for military and disaster response applications have encouraged development of shelf-stable oxygen carriers. Growing awareness of blood shortages and transfusion-related risks further strengthens the region’s leadership in artificial blood substitute adoption.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global artificial blood substitute market comprises established biotech firms, specialised oxygen carrier developers, and emerging players focused on next-generation substitutes. Companies compete through research, clinical development, regulatory approvals, and strategic collaborations with healthcare institutions and research organisations. Hemoglobin-based oxygen carriers and perfluorocarbon emulsions represent major technology platforms, with cell-derived engineered red blood cells emerging rapidly. Competitive differentiation hinges on safety, efficacy, circulation time, manufacturing scalability, and regulatory status. Market fragmentation and limited dominance allow innovation from small innovative firms alongside larger players investing in R&D, partnerships, and expanded geographic presence to address unmet clinical needs and regulatory hurdles.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the chronic global shortage of donor blood and the rising number of surgical procedures and trauma cases. Artificial blood substitutes offer advantages like universal compatibility without cross-matching and a longer shelf life. Additionally, the increasing prevalence of blood-borne diseases makes pathogen-free synthetic alternatives highly desirable.

Q2. What are the main restraining factors for this market?

Growth is primarily hindered by the immense technical difficulty of mimicking the complex functions of natural hemoglobin and the high cost of production. Stringent regulatory hurdles and a history of failed clinical trials have also slowed progress. Concerns regarding side effects, such as vasoconstriction and oxidative stress, remain significant challenges.

Q3. Who are the top major players for this market?

Top major players include companies like Hemopure (HbO2 Therapeutics), Nuvox Pharma, Hemarina, and Sphereson. Many are specialized biotech firms focusing on specific delivery mechanisms. Larger pharmaceutical entities and academic institutions also play a critical role through research partnerships, aiming to bring viable synthetic blood products to the commercial market.

Q4. Which country is the largest player?

The United States is the largest player in this market. Its dominance is driven by advanced healthcare infrastructure, high research and development spending, and a robust regulatory framework provided by the FDA. Furthermore, significant funding from the Department of Defense for battlefield applications accelerates the development of blood substitute technologies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model