Get Complete Analysis Of The Report - Download Updated Free Sample PDF

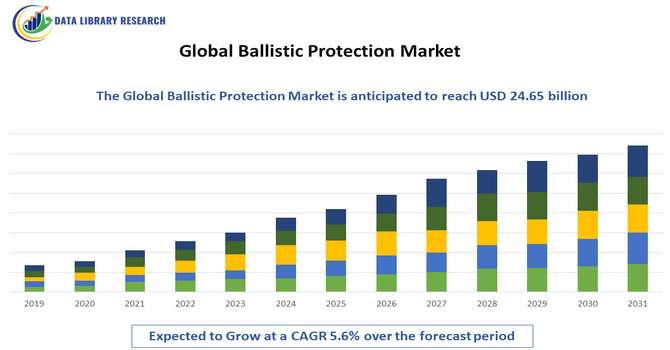

The Global Ballistic Protection Market encompasses products and systems designed to protect personnel, vehicles, and infrastructure from ballistic threats such as bullets, shrapnel, and explosive impacts. Key offerings include personal armour (body armour, helmets), vehicle armour, shields, ballistic glass, and stationary protective solutions used across military, law enforcement, private security, and civilian safety applications. Growth is driven by rising defence budgets, modernisation of armed forces, increasing internal security concerns, and technological innovations in lightweight and high-strength materials. Standards certification and evolving threat landscapes further shape procurement and product adoption worldwide.

Current trends in the Global Ballistic Protection Market include rapid adoption of lightweight composite materials like aramid fibres and UHMWPE to improve mobility without sacrificing protection, and modular armour systems that can be customised for mission profiles. Integration of smart sensors and data-enabled systems in wearable gear is emerging, enabling real-time health and threat monitoring. Civilian demand beyond traditional defence and law enforcement is rising, including private security and infrastructure protection. Regional defence modernisation—especially in Asia-Pacific—and increased investments in R&D to improve multi-threat capabilities and ergonomics remain prominent trends.

Segmentation: The Global Ballistic Protection Market is segmented by Product Type (Personal Protection Equipment, Vehicle Protection Equipment, Structural & Fixed Infrastructure Protection and Face Protection & Shields), Material Type (Composites, Aramid Fibers, UHMWPE (Ultra-High-Molecular-Weight Polyethylene), Ceramics, Metal Alloys & Others, and Bulletproof Glass), Technology Type (Hard Armor and Soft Armor), Application (Defense & Military, Law Enforcement & Homeland Security and Commercial Security & Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The demand for this market is propelled by escalating defence and homeland security budgets, driven by geopolitical tensions, asymmetric warfare, terrorism, and internal unrest. Nations prioritise modernising protective gear for armed forces and police, allocating significant portions of defence budgets to advanced ballistic systems. This spending drives procurement of high-performance body armour, helmets, vehicle armour, and integrated protective solutions. Increasing focus on soldier survivability and operational safety enhances market growth. In emerging markets, modernisation programmes and localisation mandates further boost demand, while civilian security requirements add another growth dimension.

Advancements in material science are a key driver, enabling stronger, lighter, and more versatile ballistic protection solutions. High-performance composites like aramid fibres (e.g., Kevlar), UHMWPE, hybrid ceramics, and nanotechnology-enhanced fabrics significantly improve impact resistance while reducing weight.

In November 2023, MKU Limited launched the Kavro Doma 360 ballistic helmet, offering strong protection against lethal rifles. The helmet featured customization options for night vision, communication devices, and masks, increasing operational versatility and functionality for military and law enforcement personnel in diverse mission environments. These materials support modular designs, ergonomic wearability, and multi-threat coverage, increasing adoption across military, law enforcement, and private security sectors. Continuous innovation enables manufacturers to meet evolving threat profiles, address end-user comfort concerns, and differentiate offerings, sustaining market growth through product upgrades and new segments.

Market Restraints:

A major restraint in the Global Ballistic Protection Market is the high production cost and manufacturing complexity associated with advanced materials and protective systems. Ultralight composites and hybrid armour require sophisticated fabrication processes, driving up expenses. Stringent testing and certification standards (such as NIJ or military criteria) add time and cost burdens, particularly for smaller manufacturers. Supply chain challenges for specialty raw materials can cause production delays and increase overheads. These factors limit market accessibility, especially in lower-income regions, and can slow adoption rates among budget-constrained defence and security agencies.

The ballistic protection industry significantly affects socioeconomic landscapes by enhancing national security, protecting military and law enforcement personnel, and reducing casualties in conflict zones. Expansion of this market supports high-tech manufacturing jobs, drives innovation in materials science, and stimulates R&D investments that often spill over into civilian sectors. Increased defence and homeland security spending can positively influence GDP in countries with strong defence-industrial bases. Conversely, high procurement costs may strain government budgets. Broader civilian safety applications, such as critical infrastructure protection, also contribute to public confidence and urban resilience against violent crime and terrorism.

Segmental Analysis:

The Structural & Fixed Infrastructure Protection segment is expected to witness the highest growth over the forecast period due to rising investments in safeguarding critical infrastructure such as government buildings, airports, power plants, and urban centres against ballistic threats and terrorism. Increasing global concerns about public safety and the protection of high value assets have led governments and private entities to prioritise armoured barriers, blast resistant walls, and bulletproof glass systems. Urbanisation and the expansion of smart cities further accelerate demand for advanced infrastructure protection solutions. Additionally, modernization initiatives in developed and developing economies are reinforcing infrastructure resilience, driving adoption of fixed ballistic armour products at a robust growth.

The UHMWPE (Ultra High Molecular Weight Polyethylene) segment is projected to witness the highest growth among material types over the forecast period owing to its exceptional strength to weight ratio, impact resistance, and durability. UHMWPE materials enable the development of lightweight yet highly protective armour suits, helmets, vehicle panels, and modular protective systems that reduce operator fatigue while enhancing performance. Defence and law enforcement agencies are increasingly adopting UHMWPE based solutions as they balance mobility with high ballistic resistance. The segment’s growth is further bolstered by ongoing research, innovation in polymer processing, and rising procurement in major military markets that seek advanced protective materials to meet evolving threat requirements.

The Hard Armor segment is expected to experience the highest growth across technology types during the forecast period as demand increases for rigid protective solutions capable of defeating higher threat levels, such as rifle and armour piercing rounds. Hard armour plates and ballistic inserts are integral in personal protective equipment for soldiers, tactical units, and security forces, and are seeing elevated adoption as military and law enforcement agencies modernize their armour inventories. Enhanced threat environments, counter terrorism operations, and a focus on survivability in hostile engagements drive procurement of hard armour systems. Additionally, technological improvements in ceramics, composites, and metal alloys enhance performance while managing weight, supporting long term segment expansion.

The Defense & Military end use segment is poised for the highest growth over the forecast period due to sustained government defence spending and ongoing global security challenges. Military modernization programs in major defence markets prioritise advanced ballistic protection to improve soldier survivability, vehicle armour, and force readiness. Rising geopolitical tensions, asymmetric warfare, and border security concerns increase procurement of ballistic helmets, body armour, vehicle appliqué armour, and infrastructure protection systems. Defence agencies’ long term contracts and budget allocations for protective gear further entrench this segment as the dominant growth driver. The breadth of applications—from infantry protection to armoured platforms—ensures ongoing investment and market expansion.

The North American Region is expected to witness the highest growth in the Global Ballistic Protection Market over the forecast period due to strong defence budgets, continuous modernization of armed forces, and significant law enforcement procurement.

North America accounts for a large share of global ballistic protection demand, driven by government investment in advanced armour systems, homeland security initiatives, and ongoing contracts for personal and vehicle protection. For instance, in 2025, Safe Pro Group Inc. secured a U.S. government contract to supply domestically manufactured ballistic and EOD protective equipment for Indo-Asia Pacific operations. The deal, coupled with in-theater demonstrations of its AI-driven SpotlightAI platform, highlighted North America’s leadership in advanced ballistic solutions and reinforced regional market growth.

The United States, in particular, leads regional demand through extensive R&D, domestic manufacturing capabilities, and early adoption of next generation materials like UHMWPE and composite ceramics. Stable defence funding, strategic military priorities, and alliance commitments support sustained market leadership and growth momentum.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Ballistic Protection Market is moderately concentrated, featuring multinational defence contractors and specialised protective gear manufacturers. Companies differentiate through advanced materials, integrated systems, and strategic defence contracts. Large players secure major military procurements, while mid-sized firms often focus on niche products like specialised body armour or vehicle applique kits. Strategic partnerships, R&D collaborations, and regional manufacturing expansions help drive competitiveness and market reach. With defence budgets increasing globally, leading firms compete on technological capability, production agility, and global supply chains to meet diverse end-user requirements across military, law enforcement, and private security sectors.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The ballistic protection market is growing rapidly due to rising geopolitical tensions and the modernization of military forces worldwide. Governments are increasing their defense budgets to equip soldiers with next-generation gear. Additionally, a surge in homeland security needs and the demand for lightweight, high-performance materials like graphene and advanced ceramics are pushing the market forward to ensure better mobility and safety.

Q2. What are the main restraining factors for this market?

A major challenge is the high cost of developing and manufacturing advanced ballistic materials. Strict regulatory standards and the lengthy certification processes required to meet safety levels also slow down the time-to-market for new products. Furthermore, economic fluctuations in developing nations can limit their ability to purchase expensive, high-tech armor, forcing them to rely on older, heavier equipment.

Q3. Which segment is expected to witness high growth?

The Hard Armor and Vehicle Protection segments are expected to witness the highest growth. As threats from high-velocity ammunition and improvised explosive devices (IEDs) increase, there is a massive demand for armored vehicles and heavy-duty plate inserts. Additionally, the Law Enforcement segment is growing fast as police departments prioritize officer safety during urban tactical operations and civil unrest.

Q4. Who are the top major players for this market?

The market is led by established defense giants and specialized material innovators. Key players include BAE Systems , Rheinmetall AG , and Honeywell International . Other major contributors are Point Blank Enterprises , Saab AB , and DuPont , which provides the famous Kevlar fiber. These companies focus on creating modular systems that allow users to customize their protection based on specific mission risks.

Q5. Which country is the largest player?

The United States is the largest player in the ballistic protection market. This dominance is driven by the massive US defense budget and continuous investments in "Soldier Modernization" programs. The presence of leading manufacturers and strict safety standards set by the National Institute of Justice (NIJ) also ensure that the US remains the primary hub for both innovation and consumption of protective gear.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model