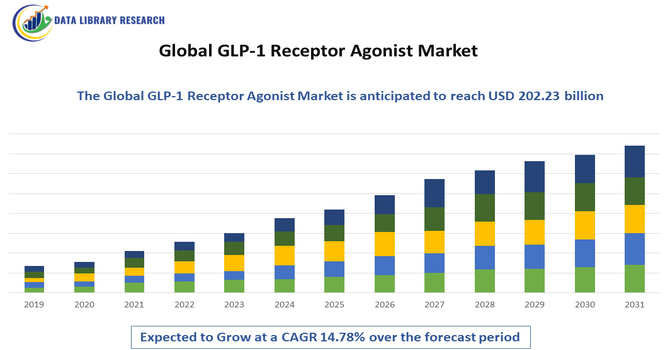

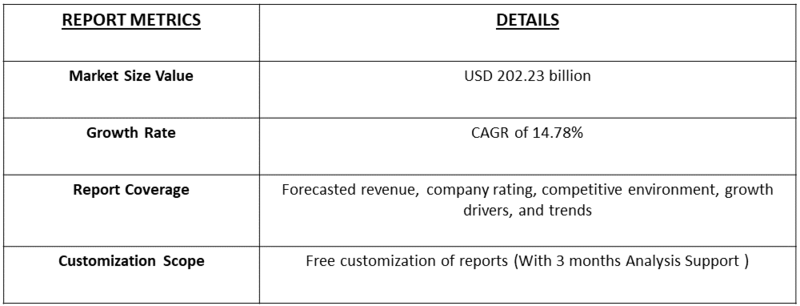

The GLP 1 (glucagon like peptide 1) receptor agonist market size was at USD 72.23 billion in 2026, is projected to reach USD 202.23 billion by 2033, at a CAGR of 14.78% from 2026 to 2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The GLP 1 (glucagon like peptide 1) receptor agonist market comprises pharmaceutical products that mimic the GLP 1 hormone to regulate blood sugar and appetite. These injectable and oral medications are primarily used for type 2 diabetes management and increasingly for obesity treatment. The market encompasses drug development, manufacturing, and commercialization by global biopharmaceutical companies. Growth is driven by rising diabetes and obesity prevalence, favorable clinical outcomes, and expanding indications. Healthcare providers, payers, and regulatory bodies influence adoption through clinical guidelines and reimbursement policies.

Key trends in the GLP 1 receptor agonist market include the shift toward oral formulations, improved patient adherence, and expanded indications beyond diabetes, particularly obesity and cardiovascular risk reduction. Biotech and pharmaceutical companies are investing in extended release formulations and combination therapies pairing GLP 1 with other hormones like GIP or glucagon for enhanced efficacy. Real world evidence from large patient populations is reinforcing clinical benefits, prompting guideline updates and increased payer coverage. Digital health tools that support treatment monitoring are also gaining traction. Geographic expansion into emerging markets and affordability initiatives are further shaping uptake, reflecting a broader emphasis on chronic disease management and preventive care.

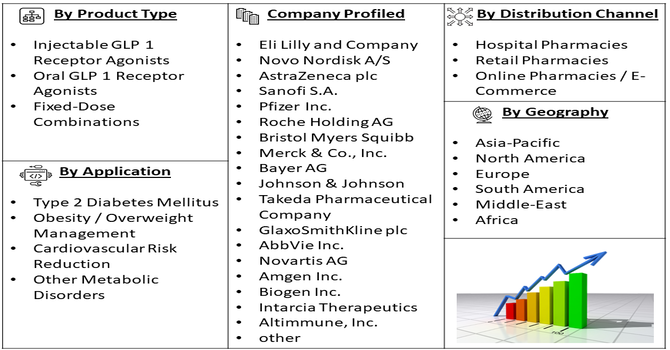

Segmentation: The GLP 1 (glucagon like peptide 1) receptor agonist market is segmented by Product Type (Injectable GLP 1 Receptor Agonists, Oral GLP 1 Receptor Agonists and Fixed-Dose Combinations), Application (Type 2 Diabetes Mellitus, Obesity / Overweight Management, Cardiovascular Risk Reduction and Other Metabolic Disorders), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and Online Pharmacies / E-Commerce), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A major driver of the GLP 1 receptor agonist market is the increasing global prevalence of type 2 diabetes and obesity. Sedentary lifestyles, aging populations, and unhealthy diets contribute to a surge in metabolic disorders, prompting greater clinical demand for effective therapies. For instance, in July 2023, an article published by The Lancet reported that prevalence of abdominal obesity in the India was found to be 40% in women and 12% in men. The findings show that 5–6 out of 10 women between the ages of 30–49 are abdominally obese.

GLP 1 receptor agonists not only improve glycemic control but also support weight loss, making them appealing for dual benefits. Public health focus on early intervention and disease prevention further amplifies uptake. Healthcare systems, particularly in developed and emerging economies, are prioritizing treatments that reduce long term complications, thereby propelling investment and research into this class of drugs.

Another key driver is the expansion of therapeutic indications for GLP 1 receptor agonists. Originally approved for glycemic control in type 2 diabetes, these agents have demonstrated benefits in weight management, cardiovascular risk reduction, and non alcoholic fatty liver disease, attracting broader clinical use.

Regulatory approvals for obesity treatment in multiple regions have significantly expanded the patient pool. For instance, in July 2024, Amylyx Pharmaceuticals acquired Avexitide, a GLP-1 receptor agonist, from Eiger Biopharmaceuticals. The therapy held FDA breakthrough designation for Postbariatric Hypoglycemia and congenital hyperinsulinism. Phase 2 trials showed strong reductions in severe hypoglycemic events, and the drug was scheduled to begin Phase 3 trials in 2025. Positive outcomes from cardiovascular outcome trials have strengthened clinician confidence and guideline recommendations. This broadened utility supports greater prescription volume, investment in new formulations, and enhanced payer reimbursement policies, driving overall market growth across diverse patient populations.

Market Restraints:

A major restraint for the GLP 1 receptor agonist market is the high cost of therapy, which limits patient access and insurance coverage in many regions. These biologic drugs often carry premium pricing due to complex manufacturing and research costs, leading to affordability concerns, especially in low and middle income countries. Out of pocket expenses can deter long term adherence. Payer restrictions and stringent reimbursement policies also restrict use to specific patient segments. Regulatory price controls and competitive pressure from biosimilars may mitigate costs over time, but current economic barriers remain a significant challenge to widespread adoption.

The GLP 1 receptor agonist market significantly impacts socioeconomic systems by addressing widespread chronic conditions like type 2 diabetes and obesity, which burden healthcare budgets globally. Effective therapies reduce complications such as cardiovascular disease, hospitalization rates, and long term disability costs, improving population health and productivity. However, pricing and access disparities remain challenges, influencing equity in treatment availability across different income groups and regions. Expanded use of GLP 1 drugs can decrease indirect costs by enabling healthier lifestyles and work participation, while stimulating economic activity through pharmaceutical innovation and employment. Public health initiatives often integrate these therapies to support preventive care and reduce long term societal healthcare expenditures.

Segmental Analysis:

The oral GLP 1 receptor agonists segment is expected to witness the highest growth over the forecast period due to increasing patient preference for non-invasive, convenient treatments. Unlike injectable formulations, oral medications improve adherence, especially among individuals managing chronic conditions such as type 2 diabetes and obesity. Pharmaceutical companies are investing in innovative oral formulations with extended-release properties and enhanced bioavailability, broadening treatment accessibility. Rising awareness of lifestyle management and growing acceptance among healthcare providers are further fueling adoption. Additionally, ongoing regulatory approvals in major markets are expanding the patient base, positioning oral GLP 1 receptor agonists as a preferred, high-growth segment within the global metabolic disease therapy market.

The obesity and overweight management segment is expected to experience the highest growth during the forecast period. Increasing global prevalence of obesity, driven by sedentary lifestyles and poor dietary habits, has created strong demand for effective weight management therapies. GLP 1 receptor agonists, initially developed for type 2 diabetes, have demonstrated significant weight reduction benefits, leading to expanded indications and regulatory approvals for obesity treatment. Rising awareness of the health risks associated with obesity, including cardiovascular disease and metabolic disorders, is driving patient adoption. Healthcare providers are increasingly prescribing GLP 1 therapies for weight management, making this segment a key growth driver in the global GLP 1 receptor agonist market.

The hospital pharmacies segment is projected to witness the highest growth over the forecast period, driven by the widespread adoption of GLP 1 receptor agonists in clinical settings. Hospitals remain the primary point of care for patients requiring prescription-based chronic disease management, including type 2 diabetes and obesity. The availability of specialist consultation, monitoring, and administration support within hospitals enhances treatment adherence and clinical outcomes. Additionally, hospital pharmacies offer bulk procurement advantages, ensuring consistent supply for high-cost biologics. Rising awareness among healthcare providers about the benefits of GLP 1 therapies and inclusion in hospital formularies further supports adoption. This makes hospital pharmacies a dominant channel in the market.

The North American region is expected to witness the highest growth in the GLP 1 receptor agonist market over the forecast period. High prevalence of type 2 diabetes and obesity, coupled with advanced healthcare infrastructure, favorable reimbursement policies, and strong patient awareness, drives market expansion. For instance, the Government of Canada, published the recent data that highlighted with 5,805,000 people (15%) affected by diagnosed and undiagnosed diabetes, projected to reach 7,304,000 (16%). Diagnosed cases stood at 4,007,000 (10%), expected to rise to 5,301,000 (12%). Type 1 accounted for 5–10% of prevalence. Combined diabetes and prediabetes affected 11,918,000 (30%), forecasted to grow to 14,123,000 (32%). Diagnosed cases were projected to increase 32% by 2034, while total diagnosed and undiagnosed cases were expected to rise 26%.

Leading pharmaceutical companies actively invest in research, development, and regulatory approvals within the region, ensuring early access to innovative GLP 1 therapies. For instance, in January 2024, Novo Nordisk announced research collaborations with two U.S.-based biotechnology companies to advance treatments for cardiometabolic disorders. The partnerships aimed to accelerate innovation, expand its therapeutic pipeline, and maintain a competitive edge in next-generation metabolic drug development.

Similarly, in 2024, Eli Lilly indicated plans to launch Mounjaro in India, pending regulatory approval. The company expected the diabetes and obesity therapy to strengthen its presence in the Indian market and contribute positively to market growth following successful clearance from authorities.

Moreover, the growing adoption of oral formulations and combination therapies further boosts demand. Government initiatives targeting chronic disease management and widespread insurance coverage enhance accessibility. These factors collectively position North America as the fastest-growing and most lucrative market for GLP 1 receptor agonists globally.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the GLP 1 receptor agonist market is characterized by intense innovation, strong patent portfolios, and strategic alliances. Major pharmaceutical players compete through differentiated efficacy, safety profiles, delivery formats (injectable vs. oral), and frequency of dosing. Biotech startups collaborate with larger firms for development and commercialization, while established companies invest heavily in clinical trials to expand indications and extend exclusivity. Pricing strategies and market access negotiations with payers are crucial competitive levers. Regulatory approvals across global markets and intellectual property protections influence product lifecycles. Mergers, acquisitions, and licensing agreements continue to reshape the market, driving consolidation and enhancing global reach.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary drivers include the global surge in obesity and type 2 diabetes cases. Increasing clinical evidence supporting cardiovascular benefits, alongside the "off-label" popularity of these drugs for weight loss, has spiked demand. Furthermore, improved health insurance coverage and the shift toward convenient, once-weekly injectable formulations are accelerating market adoption.

Q2. What are the main restraining factors for this market?

High treatment costs and limited affordability in developing regions significantly hinder market expansion. Supply chain bottlenecks and manufacturing shortages have also prevented companies from meeting unprecedented demand. Additionally, potential side effects such as gastrointestinal distress and long-term safety concerns regarding thyroid or pancreatic health remain notable barriers to widespread usage.

Q3. Which segment is expected to witness high growth?

The obesity and weight management segment is projected to experience the most rapid growth. While originally developed for diabetes, the approval of GLP-1s specifically for chronic weight management has opened a massive consumer demographic. Oral formulations are also gaining traction as a high-growth alternative to traditional needle-based subcutaneous injections.

Q4. Who are the top major players for this market?

Novo Nordisk and Eli Lilly dominate the landscape, holding the majority share with blockbusters like Ozempic, Wegovy, Mounjaro, and Zepbound. Other key players include Sanofi, AstraZeneca, and Amgen, who are aggressively developing next-generation assets. These companies focus on clinical trials to expand indications and increasing their manufacturing capacity worldwide.

Q5. Which country is the largest player?

The United States is the largest player, accounting for the highest revenue share globally. This dominance is fueled by high healthcare spending, a large population living with obesity or diabetes, and premium pricing. The U.S. market also benefits from rapid regulatory approvals and aggressive direct-to-consumer marketing campaigns by major pharmaceutical firms.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model