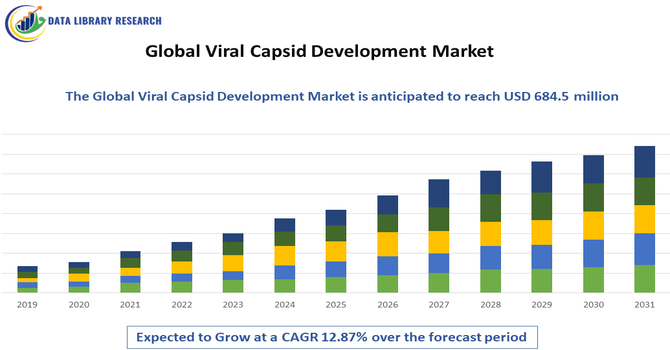

The Global Viral Capsid Development Market size was estimated at USD 314.3 million in 2026 and is projected to reach USD 684.5 million by 2033 growing with a CAGR of 12.87% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Viral Capsid Development Market refers to the economic and scientific ecosystem dedicated to designing, engineering, and producing viral capsids — protein shells that encase genetic material in viruses — for therapeutic, vaccine, and biotechnology applications. These capsids serve as delivery vehicles in gene therapy, viral vector vaccines, and biomedical research tools. Market activities include capsid discovery, optimization, scalable production, quality control, and regulatory compliance. Growth is propelled by rising demand for advanced gene-based therapies, innovations in viral vector platforms, and increasing investment in biologics. Key stakeholders encompass biotechnology firms, contract development and manufacturing organizations (CDMOs), academic institutions, and pharmaceutical companies supporting clinical translation and commercialization.

Current trends in the viral capsid development market highlight precision engineering of capsids to enhance tissue targeting and evade the immune system, improving safety and therapeutic outcomes. The integration of AI and computational biology into capsid design accelerates discovery and reduces development time. Platform technologies that enable modular capsid customization are becoming strategic assets. Demand for next-generation viral vectors in oncology, rare diseases, and immunization stimulates innovation. Collaborative ventures between pharma and biotechnology firms are increasing to share expertise and investments. Additionally, scalable manufacturing and quality assurance solutions are evolving to meet stringent regulatory standards and support global clinical pipelines.

Segmentation:The Global Viral Capsid Development Market is segmented by Product Type (Adeno-Associated Virus (AAV) Capsids, Lentiviral Capsids, Adenoviral Capsids, Retroviral Capsids and Others), Technology (Natural Capsid Platforms, Engineered/Modified Capsids, Synthetic Capsid Technologies, Computational/AI-based Capsid Design, and High-Throughput Screening Platforms), Application (Gene Therapy, Vaccine Development & Delivery, Oncology Therapeutics, Rare & Genetic Disease Treatments, Biomedical Research & Diagnostics and Drug Delivery Systems), Therapeutic Area (Neurological Disorders, Oncological Diseases, Cardiovascular Diseases, Infectious Diseases and Metabolic & Genetic Disorders), End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Contract Development & Manufacturing Organizations (CDMOs), Academic & Research Institutes and Hospitals & Clinical Research Centres), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The major driver of the viral capsid development market is the rapid expansion of gene therapy research and clinical programs. Viral capsids are core components of gene delivery systems, facilitating targeted insertion of therapeutic genes.

As prevalence of genetic disorders and unmet medical needs grow, so does investment in curative and durable treatments. Regulatory approvals of gene therapies reinforce confidence and attract funding across biotech and pharma sectors. For instance, in February 2026, Sarepta Therapeutics launched ELEVIDYS in Japan through Chugai Pharmaceutical Co., Ltd. following National Health Insurance listing, marking the country’s first approved gene therapy for Duchenne muscular dystrophy. The launch expanded global gene therapy adoption, strengthened commercial validation of AAV-based treatments, and stimulated growth in the global viral capsid development market.

Personalized medicine trends further emphasize tailored delivery vehicles, boosting demand for novel capsid technologies. Advances in capsid design that improve specificity and reduce immune responses accelerate development cycles and broaden therapeutic applicability globally.

Technological innovation significantly fuels the global viral capsid development market. Breakthroughs in computational design, high-throughput screening, and synthetic biology enable creation of capsids with enhanced stability, specificity, and manufacturability, reducing development timelines and costs. Machine learning assists in predicting capsid behavior and immune interactions, facilitating efficient lead optimization.

In 2024, Dyno Therapeutics announced a collaboration with NVIDIA that significantly advanced computational AI-based capsid design. By integrating generative AI with scalable BioNeMo infrastructure, the partnership accelerated in vivo–validated viral vector optimization, strengthened technological innovation in sequence engineering, and expanded growth opportunities across the global viral capsid development market. Platform technologies allow modular engineering of capsid components, broadening application scopes across gene therapies and vaccines. Improvements in scalable production systems and quality control processes support commercialization and regulatory readiness. These advancements help companies differentiate offerings, attract partnerships, and address complex biological challenges, fostering rapid market growth and sustained innovation.

Market Restraints:

A key restraint in the viral capsid development market is regulatory complexity and safety concerns. Viral vectors require rigorous preclinical and clinical evaluation to address immunogenicity, off-target effects, insertional mutagenesis, and long-term safety, leading to extended development timelines and high costs. Regulatory agencies across regions maintain stringent requirements, which can vary internationally, complicating global approval strategies. Smaller companies often lack the resources to navigate complex regulatory pathways, delaying market entry. Additionally, public and ethical scrutiny regarding viral technologies can influence policy and adoption. These challenges can constrain investment, slow innovation, and increase barriers for new entrants competing with established players.

The viral capsid development market produces profound socioeconomic benefits by enabling advanced treatments for genetic disorders, cancer, and infectious diseases. These technologies underpin gene therapies that can reduce lifetime healthcare costs by offering durable or curative outcomes versus chronic care, improving patient quality of life. Expansion of research and manufacturing creates skilled employment in life sciences, attracts investment, and fosters biotechnology hubs worldwide. However, high treatment costs risk accessibility gaps between high-income and low-income regions, necessitating policy frameworks for equitable access. Public and private funding in this sector can strengthen healthcare infrastructure, spur innovation, and improve global health equity when aligned with inclusive strategies.

Segmental Analysis:

The Adeno-Associated Virus (AAV) capsids segment is expected to witness the highest growth over the forecast period due to expanding adoption in gene therapy and long-term therapeutic delivery. AAVs exhibit favorable safety profiles, low immunogenicity, and stable transgene expression, making them ideal for rare and chronic disease treatments. Continuous technological advancements in AAV serotype engineering and manufacturing scalability are improving targeting efficiency and vector yield. Regulatory approvals of AAV-based therapies have strengthened industry confidence, attracting investment and pipeline expansion. Increasing clinical success rates, coupled with rising prevalence of genetic disorders requiring durable therapeutic solutions, further accelerate demand. Consequently, AAV capsids are poised to dominate growth within viral capsid development markets.

The engineered/modified capsids segment is projected to experience the highest growth over the forecast period as precision design becomes central to viral vector performance. Engineered capsids improve tissue specificity, evade host immune responses, and enable tailored therapeutic delivery, directly addressing limitations of natural viral vectors. Integration of computational design tools and AI accelerates identification of optimized capsid variants while enhancing safety and efficacy profiles. Research initiatives increasingly focus on novel capsid libraries and customizable platforms that support diverse applications, from gene therapy to targeted vaccines. The demand for next-generation delivery solutions across multiple therapeutic areas, including rare diseases and oncology, strengthens the case for engineered capsids as a rapidly expanding market segment.

The vaccine development & delivery segment is expected to record the highest growth over the forecast period as viral capsids become integral to advanced vaccine platforms. Viral capsid vectors enable efficient antigen presentation and immune priming with robust safety profiles, accelerating vaccine efficacy. The global focus on pandemic preparedness, including rapid response to emerging infectious diseases, has amplified demand for versatile vector technologies. Investments in capsid-based vaccine delivery systems, including adjuvant optimization and mucosal delivery approaches, are gaining traction. Furthermore, public-private partnerships and regulatory support for innovative vaccine platforms enhance commercialization prospects. Overall, expanding immunization programs and ongoing research into capsid-mediated delivery drive notable segment growth.

The oncological diseases segment is anticipated to witness the highest growth over the forecast period as viral capsid technologies play an increasingly critical role in targeted cancer therapies. Capsid-based vectors facilitate gene delivery to malignant tissues, enabling therapeutic modalities like oncolytic virotherapy and gene-directed enzyme prodrug therapy. Advances in capsid design enhance tumor tropism and reduce off-target effects, improving clinical outcomes. Rising global cancer incidence rates and heightened investment in precision oncology fuel demand for innovative delivery mechanisms. Additionally, combination strategies integrating capsid vectors with immunotherapies and checkpoint inhibitors expand treatment potential. With oncology research pipelines rapidly evolving, this segment is poised for accelerated expansion in viral capsid applications.

The pharmaceutical & biotechnology companies’ segment is expected to witness the highest growth over the forecast period, driven by escalating investments in gene therapy and viral vector platform development. Large biopharma organizations and emerging biotech firms are increasingly prioritizing novel viral capsid technologies to advance therapeutic pipelines and improve competitive positioning. Strategic collaborations, licensing agreements, and acquisitions augment internal research capabilities and accelerate time to market. Investment in proprietary capsid platforms and scalable manufacturing infrastructure further amplifies capability development. Heightened focus on rare disease treatments, personalized medicine, and targeted delivery systems supports sustained sector growth. As R&D intensity rises and regulatory pathways evolve, pharmaceutical and biotech companies remain the principal growth engines in this market.

The North American region is anticipated to witness the highest growth over the forecast period due to a strong innovation ecosystem, robust funding, and advanced healthcare infrastructure.

The United States and Canada are global leaders in biomedical research, with an extensive concentration of biotechnology firms, academic institutions, and clinical facilities driving viral capsid development. For instance, in May 2021, Biogen Inc. and Capsigen Inc. formed a strategic research collaboration to engineer novel AAV capsids using the TRADE platform. The partnership accelerated CNS and neuromuscular gene therapy innovation, strengthened regional R&D capabilities, and stimulated investment, competitiveness, and technological advancement across North America’s viral capsid development market.

Substantial public and private investment in gene therapy, biologics, and vaccine programs accelerates pipeline progression and commercialization. Favourable regulatory frameworks, intellectual property protections, and strategic collaborations enhance market confidence. Additionally, high disease prevalence rates and growing adoption of precision medicine heighten demand for advanced capsid technologies. For instance, an article published by National Institute of Health, reported that in 2022, NF1 is a genetic disorder that affects approximately 1 in 3,000 people in US. The disease can lead to the development of disfiguring, disabling, and painful benign and malignant tumors, called plexiform neurofibromas (PNs). These factors collectively position North America at the forefront of market expansion.

| Report Matrics | Details |

| Market Size Value | USD 684.5 million |

| Growth Rate | CAGR of 12.87% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of viral capsid development comprises large pharmaceutical corporations, specialized biotech innovators, and contract development/manufacturing organizations. Competition centers on proprietary capsid libraries, engineering platforms, intellectual property portfolios, and scalable production capabilities. Companies differentiate through advanced design technologies, regulatory expertise, and strategic collaborations across research institutions and industry partners. Mergers, acquisitions, and licensing deals are common as firms seek to expand pipelines and market reach. Startups with breakthrough capsid technologies can disrupt traditional players, while established firms leverage financial resources and global footprints. North America and Europe currently lead market activity, while Asia-Pacific is rapidly emerging with increased R&D investment and production capacity.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary drivers include the rising prevalence of genetic disorders and the expanding pipeline of cell and gene therapies. Significant investments in biotechnology, breakthroughs in recombinant AAV engineering, and the increasing demand for targeted drug delivery systems fuel market expansion. Furthermore, the shift toward personalized medicine necessitates advanced capsid development.

Q2. What are the main restraining factors for this market?

Growth is primarily hindered by high development costs and complex regulatory hurdles associated with viral vector safety. Immunogenicity concerns, where the human immune system rejects certain viral capsids, also pose a significant challenge. Additionally, technical difficulties in scaling up production while maintaining high purity and titer levels limit widespread adoption.

Q3. Which segment is expected to witness high growth?

The Adeno-associated virus (AAV) segment is projected to experience the highest growth due to its low toxicity and ability to infect both dividing and non-dividing cells. Within applications, the oncology and neurology sectors are leading, driven by a surge in clinical trials for rare diseases and various terminal cancers.

Q4. Who are the top major players for this market?

Key industry leaders include Thermo Fisher Scientific, Danaher Corporation (Cytiva), and Lonza Group. Other significant contributors are Merck KGaA, Charles River Laboratories, and specialized firms like WuXi AppTec and Oxford Biomedica. These players focus on strategic partnerships, capacity expansions, and proprietary capsid engineering platforms to maintain their competitive market positions.

Q5. Which country is the largest player?

The United States is the largest player in the market, holding a dominant share due to its robust healthcare infrastructure and extensive R&D spending. The presence of major biopharmaceutical hubs, a favorable regulatory environment for orphan drugs, and high concentration of clinical-stage gene therapy companies solidify its global leadership position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model