Get Complete Analysis Of The Report - Download Updated Free Sample PDF

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Coated Microneedle Drug Delivery System Market refers to the rapidly evolving sector focused on the development and commercialization of minimally invasive microneedle technologies coated with therapeutic agents for efficient, painless, and targeted drug delivery. These systems utilize microscopic needles coated with active pharmaceutical ingredients to penetrate the skin’s outer layer, enabling controlled release of drugs without the discomfort associated with traditional injections. Driven by increasing demand for patient-friendly drug administration methods, rising prevalence of chronic diseases, and advancements in biocompatible materials and coating techniques, this market is witnessing significant growth. Applications span vaccines, insulin delivery, cosmetic treatments, and chronic disease management, with key players innovating to improve drug efficacy, safety, and patient compliance across global healthcare sectors.

The key trends in the Global Coated Microneedle Drug Delivery System Market include growing adoption of painless and minimally invasive drug delivery methods as alternatives to conventional injections, driven by patient preference and improved compliance. Advances in coating technologies, such as polymer coatings and nanoparticle formulations, are enhancing drug stability and controlled release profiles. The market is also seeing increased focus on vaccine delivery, especially in response to global immunization needs, alongside expansion in chronic disease treatments like diabetes and cancer. Additionally, ongoing research into biodegradable and dissolvable microneedles is boosting safety and reducing medical waste. Collaborations between pharmaceutical companies and technology developers are accelerating product innovation, while regulatory bodies are gradually establishing clearer guidelines, supporting faster commercialization of microneedle systems worldwide.

Segmentation: The Global Coated Microneedle Drug Delivery System Market is by Type (Solid Coated Microneedles and Dissolvable Coated Microneedles), Material (Silicon, Metal, Polymer, and Carbohydrate-Based Microneedles), Application (Vaccine Delivery, Insulin Delivery, Oncology Treatments, Dermatology, and Pain Management), End-User (Hospitals & Clinics, Homecare Settings, and Research Institutes), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers: For Detailed Market Segmentation - Get a Free Sample PDF

The increasing demand for painless, minimally invasive drug delivery methods is a major driver of the coated microneedle drug delivery system market. Traditional hypodermic injections often cause pain, fear, and discomfort, leading to poor patient compliance, particularly in chronic disease management and pediatric care. Coated microneedles, designed to deliver drugs through the skin without reaching nerve-rich deeper tissues, offer a virtually pain-free experience. This technology is especially attractive for vaccinations, insulin delivery, and biologic therapies. As healthcare systems shift toward patient-centric approaches, the appeal of self-administered, easy-to-use microneedle patches continues to grow. Additionally, the reduced risk of infection and needle-stick injuries further supports the adoption of coated microneedle systems across clinical and homecare settings.

The technological advancements in microneedle fabrication and drug-coating techniques are significantly driving market growth. Innovations in biocompatible and biodegradable polymers, nanomaterials, and sugar-based compounds have improved the safety, efficiency, and dissolution profiles of coated microneedles.

In parallel, advancements in 3D printing, micro-molding, and laser cutting technologies have enhanced the precision and scalability of microneedle production, making commercial manufacturing more feasible. For instance, in September 2025, Medtronic plc announced FDA clearance of its SmartGuard™ algorithm as an interoperable automated glycemic controller (iAGC) for integration with Abbott’s Instinct sensor for type 1 diabetes. Additionally, the FDA approved the MiniMed™ 780G system for adults with insulin-requiring type 2 diabetes. These FDA approvals underscored the growing demand for automated, user-friendly insulin delivery systems, reinforcing the potential of coated microneedles as a minimally invasive alternative. The advancement also encouraged innovation in smart, integrated drug delivery platforms within the diabetes care segment. These improvements lower production costs and support mass customization, enabling companies to bring innovative microneedle-based therapies to market faster, while ensuring compliance with strict medical safety standards.

Market Restraints:

Despite their potential, coated microneedle drug delivery systems face significant challenges related to high development costs and complex regulatory pathways. The need for specialized materials, advanced manufacturing processes, and precision coating technologies makes product development expensive and time-consuming. Moreover, regulatory bodies such as the FDA and EMA require comprehensive data on safety, efficacy, biocompatibility, and long-term stability, which can delay market entry. Since microneedle systems are relatively new in the medical field, standardized testing protocols and classification guidelines are still evolving, adding further uncertainty. Smaller companies and startups, in particular, face barriers in securing funding and navigating regulatory approvals. These challenges hinder large-scale commercialization and limit the accessibility of microneedle-based products in lower-income or resource-constrained regions.

The Global Coated Microneedle Drug Delivery System Market is poised to significantly improve healthcare accessibility and patient quality of life by offering painless, easy-to-use drug administration alternatives that reduce dependency on healthcare professionals and clinics. This technology supports increased vaccination coverage, especially in remote or underserved regions, helping to control infectious diseases more effectively. By enhancing patient compliance and reducing complications associated with traditional injections, coated microneedles can lower overall treatment costs and healthcare burdens. Moreover, the market stimulates economic growth by driving innovation, creating jobs in biotech and manufacturing sectors, and encouraging investments in research and development, ultimately contributing to more efficient and equitable healthcare delivery worldwide.

Segmental Analysis:

The dissolvable coated microneedles segment is anticipated to experience significant growth due to their safety, biocompatibility, and ease of use. Unlike solid or hollow microneedles, dissolvable microneedles are made from biodegradable materials that fully dissolve in the skin, releasing the coated drug without leaving any sharp waste behind. This minimizes the risk of infection and enhances patient compliance, especially in self-administered therapies. These microneedles are gaining popularity in vaccine delivery, chronic disease management, and dermatological applications. As regulatory bodies increasingly favor safe, low-risk drug delivery alternatives, and the demand for needle-free administration grows, dissolvable microneedles are emerging as a key innovation. Continuous advancements in materials science and coating techniques further support the scalability and commercial viability of this segment.

Carbohydrate-based microneedles are projected to witness strong growth owing to their high biocompatibility, natural biodegradability, and ability to safely deliver drugs through the skin. Made from materials like hyaluronic acid, maltose, or chitosan, these microneedles dissolve after skin insertion, making them ideal for single-use applications such as vaccine delivery and cosmetic therapies. Their natural origin reduces the risk of adverse reactions, which is crucial for sensitive applications like pediatric or dermatological use. Additionally, carbohydrate-based microneedles offer enhanced drug stability and controlled release properties, making them a preferred choice for complex biologics and peptides. Ongoing R&D focused on optimizing mechanical strength and dissolution rates is helping to bring more of these innovative solutions into mainstream healthcare and regulatory approval pipelines.

The insulin delivery segment is expected to grow significantly, driven by the global rise in diabetes prevalence and the need for more patient-friendly alternatives to traditional injections. Coated microneedles offer a less invasive, pain-free, and self-administered method of insulin delivery, which improves patient adherence and overall disease management. These microneedle systems can deliver insulin directly through the skin in a controlled manner, reducing the risk of hypoglycemia and enhancing therapeutic outcomes. They are particularly appealing to needle-phobic patients and pediatric or elderly populations who struggle with frequent injections. As healthcare shifts toward personalized and wearable drug delivery systems, coated microneedles are gaining traction as a safer, more convenient option. Advances in smart coatings and patch-based delivery systems further boost this segment’s growth potential.

Hospitals and clinics are expected to remain key end-users in the coated microneedle drug delivery system market, with growing adoption fueled by their ability to handle high patient volumes and complex treatments. These facilities are increasingly incorporating microneedle technology for vaccinations, local anesthesia, dermatological treatments, and chronic disease management due to its ease of use, reduced infection risk, and patient comfort. Coated microneedles allow healthcare providers to deliver precise dosages with minimal training, improving workflow efficiency and patient outcomes. As the healthcare system pushes toward reducing needle-stick injuries and medical waste, microneedle adoption in clinical settings continues to rise. Moreover, the integration of microneedle patches into outpatient care and ambulatory services enhances their appeal in both urban and rural healthcare infrastructure.

North America is projected to witness substantial growth in the coated microneedle drug delivery system market due to its advanced healthcare infrastructure, strong R&D ecosystem, and early adoption of innovative medical technologies. The region is home to leading biotech and pharmaceutical companies actively investing in microneedle development for applications such as vaccine delivery, insulin administration, and cosmetic treatments. Supportive regulatory frameworks, such as FDA fast-track designations and increasing clinical trial activity, are accelerating product approvals and commercialization. Furthermore, high awareness among healthcare professionals and patients regarding minimally invasive treatments is driving demand. The region’s growing burden of chronic diseases, including diabetes and cancer, also fuels the adoption of next-generation drug delivery solutions like coated microneedles, positioning North America as a key growth hub.

| Report Matrics | Details |

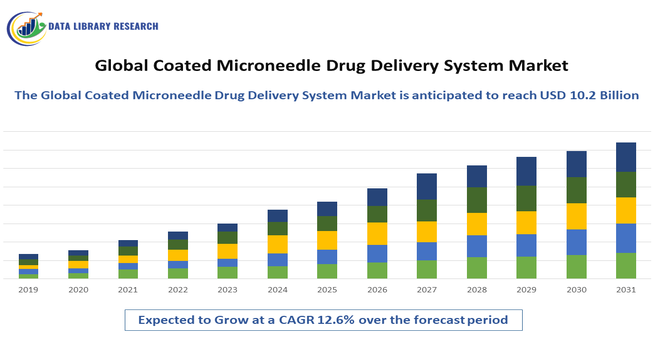

| Market Size Value | USD 10.2billion |

| Growth Rate | CAGR of 12.6% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Coated Microneedle Drug Delivery System Market is characterized by a mix of established pharmaceutical giants, specialized biotech firms, and emerging startups focused on microneedle technology innovations. Leading players invest heavily in R&D to develop proprietary coating technologies, improve drug formulations, and secure regulatory approvals. Strategic partnerships and collaborations between device manufacturers, pharmaceutical companies, and research institutions are common, accelerating product development and market entry. Companies compete on parameters such as safety, efficacy, manufacturing scalability, and cost-effectiveness. Key market players are also expanding their geographic footprint to capitalize on growing demand in emerging markets, intensifying competition and fostering continuous innovation in this rapidly evolving sector.

The 20 major players for above market are:

Recent News:

Q1. What are the main growth driving factors for this market?

The primary driver is the surging demand for patient-friendly and minimally invasive drug delivery alternatives to traditional injections, which greatly enhances patient compliance. Other significant factors include the rising global prevalence of chronic diseases like diabetes, necessitating convenient self-administration methods (e.g., insulin patches). Additionally, the application of microneedles in vaccination is expanding, leveraging patches that can offer improved thermal stability (bypassing the cold-chain) and be administered by individuals with minimal training, thereby simplifying mass immunization efforts. Finally, continuous technological advancements in microneedle materials and design, coupled with favorable regulatory pathways, are propelling market growth.

Q2. What are the main restraining factors for this market?

Several factors restrict the market's growth. A key challenge is the limited drug-loading capacity of current microneedle patches, which restricts their use for high-dose therapies. The intricate and expensive manufacturing processes, particularly high capital expenditure (CAPEX) for roll-to-roll fabrication lines, present an economic hurdle. Furthermore, the market faces stringent regulatory hurdles and a general lack of specific, harmonized guidance for these novel combination products, which can slow down commercialization. Lastly, issues like potential drug degradation on the patch and variations in skin microflora affecting dose accuracy remain technical concerns.

Q3. Which segment is expected to witness high growth?

While the entire microneedle market is expanding, the Dissolving Microneedles segment is projected to witness particularly high growth. This is primarily due to their superior safety profile, as they eliminate the generation of hazardous sharps waste and are biodegradable. Furthermore, in terms of application, the Vaccine Delivery and Insulin Delivery segments are expected to show robust growth. Vaccine delivery is driven by thermostable patch innovations and global immunization campaigns, while insulin delivery is advancing rapidly due to demand for less painful, non-invasive systems for managing diabetes.

Q4. Who are the top major players for this market?

The Global Microneedle Drug Delivery Systems market features strong competition from established pharmaceutical and medical device giants, alongside innovative specialized firms. Top major players profiled in market reports include: Becton, Dickinson and Company (BD), 3M, Johnson & Johnson Services Inc., NanoPass Technologies Ltd., and Vaxess Technologies, Inc. Other prominent companies accelerating R&D and commercialization efforts are Raphas Co. Ltd., Corium International Inc., and AbbVie Inc. These companies are focusing on strategic collaborations and integrating advanced microfabrication and polymer technologies.

Q5. Which country is the largest player?

North America, primarily driven by the United States, currently dominates the global microneedle drug delivery systems market with the largest revenue share. This leadership is attributed to a robust and well-established pharmaceutical industry, high healthcare expenditure, significant investment in research and development for advanced transdermal delivery systems, and a favorable, supportive regulatory environment from agencies like the FDA for microneedle-based products.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model