Get Complete Analysis Of The Report - Download Updated Free Sample PDF

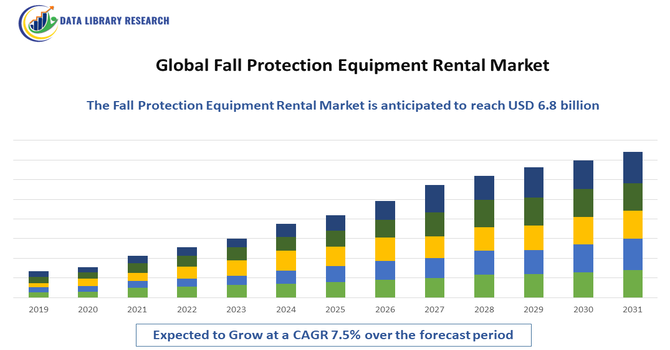

The Global Fall Protection Equipment Rental Market is experiencing steady growth, driven primarily by the rising emphasis on worker safety across industries such as construction, oil & gas, utilities, manufacturing, and mining. Increasing regulatory pressure from OSHA, ISO, and national safety bodies is pushing companies to adopt certified fall protection systems, including harnesses, lifelines, anchor points, guardrails, and rescue devices. Since many fall protection needs are project-based or short-term—especially in construction sites, shutdowns, and maintenance operations—renting equipment has become a cost-efficient alternative to ownership.

The Global Fall Protection Equipment Rental Market is evolving rapidly, driven by a few key trends. One major trend is the integration of IoT-enabled and smart safety gear, such as harnesses and lanyards outfitted with sensors that detect falls, monitor usage, and stream data to safety management systems for real-time alerts and compliance tracking. There is also a strong push toward lightweight, ergonomic, and custom-fit fall protection equipment—manufacturers are designing harnesses with breathable padding, better weight distribution, and body-specific fits to improve comfort and encourage consistent use.

Segmentation: Global Fall Protection Equipment Rental Market is segmented by Equipment Type (Full-body harnesses, Lanyards, Self-retracting lifelines, Anchorage connectors, Guardrails, Horizontal and vertical lifeline systems, Fall arrest systems), Height Safety System (Fall arrest, Fall restraint, Confined space entry systems), Material Type (Webbing-based gear, Metal components, High-strength synthetic fibers, Lightweight composite materials), End-Use Industry (Construction, Oil & gas, Mining, Utilities, Telecom, Manufacturing, Transportation), Application (Rooftop work, Tower climbing, Scaffolding operations, Industrial maintenance, Confined space entry), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Regulatory bodies such as OSHA, NIOSH, ISO, and various national safety authorities mandate the use of certified fall protection systems in industries like construction, oil & gas, utilities, telecom, and manufacturing. For instance, in 2024, the U.S. Department of Labor released comprehensive OSHA data on over 890,000 workplace injuries and illnesses across more than 91,000 workplaces, detailing incident conditions and circumstances. Employers complied with federal electronic reporting requirements via OSHA’s Injury Tracking Application. This data reinforced regulatory oversight, increased emphasis on worker safety, and supported demand in the fall protection equipment rental market by highlighting the need for safer practices and protective solutions.

Many companies prefer renting equipment rather than purchasing it outright, as rentals provide access to up-to-date, certified, and well-maintained safety gear that meets evolving standards. This approach allows organizations to remain compliant without incurring the high capital expenditure associated with purchasing and maintaining full fleets of advanced fall protection systems.

The increasing number of construction projects, industrial maintenance shutdowns, and high-risk operations is another key driver of market growth. Projects such as high-rise building construction, infrastructure development, oil & gas facility maintenance, and tower or wind energy installations often involve temporary or project-specific fall protection needs. For instance, in March 2025, Siemens launched the Industrial Copilot, which enabled customers to apply generative AI across design, planning, engineering, operations, and services. The AI assistant allowed engineering teams to generate PLC code in their native language, accelerating development, reducing errors, and lowering the need for specialized expertise. This innovation improved efficiency and quality, supporting growth in construction, industrial maintenance, and high-risk operations, while driving increased demand in the fall protection equipment rental market.

Market Restraints:

One major challenge is the high cost of advanced fall protection equipment and its maintenance, including harnesses, self-retracting lifelines, anchor systems, and rescue devices. Rental providers must invest in regular inspection, recertification, and maintenance to ensure compliance with stringent safety standards, which can increase rental prices and deter small and medium-sized enterprises from adopting these solutions. Another significant restraint is the lack of awareness and inadequate safety training in emerging markets, where many organizations still rely on outdated or improvised safety measures to reduce costs.

Segmental Analysis:

Full-body harnesses are among the most rented fall protection equipment due to their critical role in preventing severe injuries or fatalities in high-risk work environments. They distribute the force of a fall across the body, ensuring safety during operations at heights. Companies prefer renting harnesses for short-term projects, industrial shutdowns, and construction tasks because rental services provide access to certified, regularly inspected, and updated equipment without the capital burden of ownership.

Fall arrest systems are essential for stopping a worker’s fall in case of a slip or misstep during high-elevation tasks. These systems include lifelines, anchor points, and shock-absorbing lanyards. Renting fall arrest systems is particularly attractive to industries conducting temporary operations such as rooftop work, tower climbing, and scaffolding, as it ensures compliance with stringent safety regulations while avoiding long-term investment in specialized equipment.

High-strength synthetic fibers are widely used in fall protection equipment such as harnesses, lanyards, and lifelines because they provide excellent tensile strength, durability, and resistance to wear while remaining lightweight. Rental providers often supply gear made from these materials to ensure maximum safety, comfort, and performance for short-term or project-based applications, reducing the need for clients to invest in durable, high-cost equipment.

The construction industry is a leading consumer of rented fall protection equipment due to its inherently high-risk work environments, including high-rise buildings, scaffolding, and rooftop operations. Short-term projects and frequent site changes make rental solutions ideal for contractors, enabling them to access compliant and well-maintained safety systems without large capital expenditure. The sector’s focus on regulatory compliance and worker safety further drives the adoption of rental fall protection equipment.

North America is expected to witness the highest growth over the forecast period in the Global Fall Protection Equipment Rental Market, driven by stringent enforcement of occupational safety regulations, widespread awareness of workplace hazards, and the presence of a large number of industrial, construction, and oil & gas operations.

The region benefits from established rental service providers offering certified, technologically advanced fall protection equipment, including harnesses, lifelines, and anchor systems. For instance, in October 2024, FallTech announced the launch of AXIS, a Minimum Required Fall Clearance and Work Zone Calculator that modernized safety planning. The tool replaced outdated paper charts, providing precise and reliable calculations for fall clearance. According to FallTech’s VP of Business Development, Alex Dancyger, AXIS simplified complex safety calculations for professionals. Its introduction enhanced operational efficiency and accuracy on job sites, supporting growth in the North American fall protection equipment rental market.

Additionally, frequent industrial maintenance, high-rise construction projects, and tower climbing activities create strong demand for temporary, flexible, and compliant fall protection solutions, further supporting market expansion in North America. For instance, in June 2025, VINCI Construction finalized the acquisition of Peters Bros Construction Ltd, a British Columbia-based paving company generating approximately CAD 90 million. The acquisition strengthened VINCI’s capabilities, driving demand for fall protection equipment in North America by supporting safer operations on high-rise and large-scale construction projects.

Thus, such factors are driving factors of above market in the above region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Fall Protection Equipment Rental Market includes a diverse range of providers—from major safety equipment manufacturers offering rental programs to specialist rental and inspection service companies. Providers compete on equipment quality, fleet size (harnesses, lifelines, anchor systems, rescue gear), regulatory compliance, inspection and recertification services, training, and value added monitoring or IoT-enabled safety solutions. Key strategies in the market include forging partnerships with large industrial contractors, expanding regional rental networks, and maintaining up-to-date fleets to meet evolving safety standards.

Key Players:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is increasingly strict government safety regulations globally, mandating the use of certified fall protection on all elevated work sites. Growth is also fueled by construction and industrial companies preferring to rent specialized equipment rather than purchase it, avoiding high maintenance and storage costs. This rental model offers greater cost flexibility for short-term projects and ensures compliance with minimal capital expenditure.

Q2. What are the main restraining factors for this market?

A key constraint is the high cost of specialized maintenance and inspection required for rental equipment after every job, which adds to operating expenses for rental companies. The market also suffers from quality control and liability concerns, as wear and tear on rental gear can pose risks if not meticulously checked. Customers sometimes prefer owning simpler equipment for perceived long-term reliability.

Q3. Which segment is expected to witness high growth?

The Construction Industry Segment is projected to witness the highest growth. Construction sites are dynamic, with projects ranging greatly in duration and scale, making equipment rental highly practical. The frequent need for temporary safety solutions like guardrails, nets, and harnesses, combined with the industry’s strict safety audits and fluctuating workforce size, ensures that the flexible rental model remains the preferred choice over outright purchase.

Q4. Who are the top major players for this market?

The market is dominated by equipment rental giants and specialized safety equipment manufacturers who also offer rental services. Top major players include United Rentals, Inc., Ashtead Group PLC (Sunbelt Rentals), Honeywell International Inc., and 3M. Competition centers on offering the broadest inventory of high-quality, certified gear, extensive geographic coverage for quick delivery, and integrated compliance and training services alongside the equipment rental.

Q5. Which country is the largest player?

The United States is the largest country player in this market. Its dominance is due to the massive size of its commercial and residential construction sectors, combined with some of the world's most stringent occupational safety regulations enforced by OSHA. The presence of huge national rental chains and a culture of renting specialized construction tools ensures the U.S. remains the market leader in revenue and total rental volume.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model