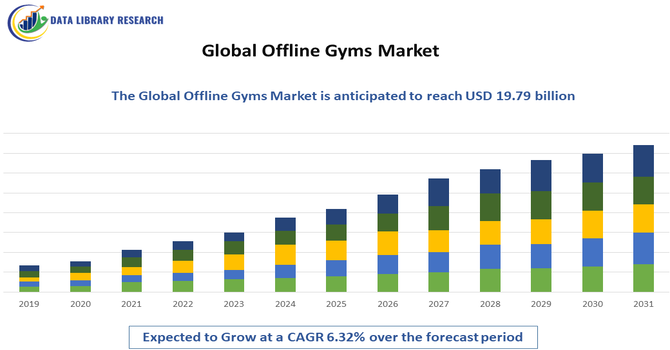

The global home fitness equipment market size is projected to grow from $12.88 billion in 2025 to $19.79 billion by 2032, exhibiting a CAGR of 6.32%.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The global offline gyms market includes physical fitness centers where people work out in person using equipment, group classes, and personal training services. These gyms range from large health clubs to smaller neighborhood fitness centers and specialized studios. Despite the growth of digital fitness, offline gyms remain important because they offer hands-on guidance, social interaction, and structured environments that many people prefer. They serve individuals with different fitness goals, from general wellness to strength training and rehabilitation. The market continues to evolve as gyms focus on creating engaging, supportive spaces that motivate people to maintain consistent and healthy exercise routines.

The current trends in the offline gyms market focus on experience, personalization, and community. Many gyms are moving beyond basic equipment to offer group classes, wellness programs, and lifestyle coaching. There is growing interest in functional training, strength-based workouts, and mind–body activities such as yoga and stretching. Gyms are also adopting technology for scheduling, progress tracking, and member engagement while keeping in-person training central. Flexible memberships and hybrid options are becoming common to meet changing consumer expectations.

Segmentation: The Global Offline Gyms Market is Segmented by Gym Type (Traditional Gyms & Health Clubs, Boutique Fitness Studios, and Specialized Training Centers), Membership Model (Monthly Memberships, Annual Memberships, Pay-Per-Visit Options, and Corporate/Group Plans), Service Offering (General Gym Access, Personal Training, Group Classes, Wellness Programs, and Lifestyle Coaching), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing awareness of physical health, mental wellbeing, and preventive care is a major driver of the global offline gyms market. People across age groups are increasingly prioritizing active lifestyles to manage stress, improve immunity, and prevent lifestyle-related conditions.

Offline gyms provide structured environments, professional guidance, and social motivation that encourage consistency in fitness routines. Campaigns promoting wellness, social media influence, and workplace health initiatives further support this shift.

As fitness becomes part of everyday life rather than a short-term goal, demand for accessible and well-equipped physical gyms continues to rise worldwide. For instance, the data published in August 2025, by MMCG Invest, reported U.S. gym density averages about 13 gyms per 100,000 people, and the memberships rebounded to 72.9 million in 2023, a 13% increase since 2019.

Many consumers prefer offline gyms for the personal interaction, hands-on coaching, and sense of community they provide. In-person training allows better form correction, personalized workout plans, and real-time motivation that digital platforms cannot fully replicate. Group classes and community-based workouts foster accountability and social connection, enhancing long-term engagement. This demand is especially strong among beginners and individuals seeking structured fitness guidance. As people increasingly value social experiences alongside physical activity, offline gyms remain attractive as shared spaces that support both fitness goals and social wellbeing.

Market Restraints:

The growth of home fitness equipment and online workout platforms poses a significant restraint on the offline gyms market. Consumers seeking convenience and flexibility often opt for at-home workouts that require less time commitment and eliminate travel. Digital fitness apps and virtual training programs also offer personalized guidance at lower perceived effort. This shift challenges gyms to maintain membership retention and justify in-person value. As a result, offline gym operators must invest more in experience, service quality, and differentiation to compete with increasingly accessible home-based fitness alternatives.

Offline gyms play an important role in improving public health by encouraging active lifestyles and reducing the risk of chronic diseases. They contribute to local economies by creating jobs for trainers, instructors, administrative staff, and maintenance workers. Gyms also support related industries such as fitness equipment, apparel, and nutrition services. On a social level, they provide spaces for interaction, motivation, and community building, which can positively affect mental health. As awareness of fitness grows, gyms help individuals build long-term healthy habits, supporting productivity and overall wellbeing across different segments of society.

Segmental Analysis:

Boutique fitness studios are expected to witness the highest growth over the forecast period due to their personalized, experience-driven approach. These studios focus on specialized workout formats such as yoga, cycling, functional training, and high-intensity programs, appealing to consumers seeking targeted results and professional attention. Their smaller class sizes foster stronger trainer–member relationships and a sense of community, which improves engagement and loyalty. Boutique studios also emphasize atmosphere, branding, and lifestyle alignment, making fitness feel more social and aspirational. As consumers increasingly value quality, specialization, and immersive experiences, boutique fitness studios continue to gain popularity across urban and suburban markets.

The annual memberships segment is expected to witness the highest growth over the forecast period as consumers seek cost-effective and commitment-based fitness solutions. Annual plans offer convenience, stability, and perceived value, encouraging members to maintain consistent workout routines. For gym operators, these memberships provide predictable revenue and improved customer retention. Many gyms enhance annual packages with added benefits such as personal training sessions, wellness programs, and priority access to classes, making them more attractive. As fitness becomes a long-term lifestyle choice rather than a temporary goal, more consumers are opting for annual memberships to support sustained health and wellness habits.

The group classes segment is expected to witness the highest growth over the forecast period due to rising demand for social and motivational workout environments. Group classes create a sense of accountability, energy, and community that encourages regular participation. Activities such as strength training, dance-based workouts, yoga, and functional fitness appeal to diverse fitness levels and preferences. Led by professional instructors, these sessions provide structure and variety, reducing workout monotony. As individuals increasingly seek interactive and engaging fitness experiences, group classes remain a key differentiator for gyms aiming to attract and retain members.

The North American region is expected to witness the highest growth over the forecast period due to strong fitness awareness, established gym culture, and high demand for structured wellness solutions. Consumers in the region actively invest in physical health, mental wellbeing, and preventive care, supporting consistent gym participation.

The presence of major gym chains, boutique studios, and innovative fitness concepts further strengthens market expansion. For instance, in April 2025, the strategic investment by Leonard Green & Partners in Crunch Fitness strengthened North America’s offline gyms market by accelerating expansion, enhancing operational capabilities, and increasing competitive intensity. The transaction supported greater capital infusion for club growth, brand development, and innovation, reinforcing investor confidence and contributing to consolidation and long-term stability within the region’s physical fitness industry.

Similarly, in December 2025, Planet Fitness’s share repurchase action positively impacted North America’s offline gyms market by signaling strong financial stability and management confidence. The move reinforced investor trust in the brick-and-mortar fitness model, supported long-term growth expectations, and strengthened Planet Fitness’s market position, indirectly encouraging capital flow and competitive confidence across the regional offline fitness indust.

Additionally, employers and communities increasingly promote fitness as part of daily life. With a focus on experience, personalization, and community-driven workouts, North America continues to lead growth in the offline gyms market.

| Report Matrics | Details |

| Market Size Value | USD 19.79 billion |

| Growth Rate | CAGR of 6.32% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the offline gyms market is diverse and dynamic. Large international gym chains compete with regional brands, boutique studios, and independent fitness centers. Budget gyms attract cost-conscious members, while premium clubs focus on high-quality facilities and personalized services. Boutique studios differentiate themselves through specialized training and strong community appeal. Competition encourages gyms to improve customer experience, introduce new programs, and maintain high service standards. Customer retention, brand loyalty, and location convenience are key competitive factors, pushing operators to continuously adapt to changing fitness preferences and lifestyle trends.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary drivers include rising health consciousness and a global increase in lifestyle-related chronic diseases. Consumers are prioritizing physical fitness and social interaction following pandemic lockdowns. Additionally, corporate wellness programs and the integration of high-tech equipment, such as biometric tracking and personalized AI coaching, are attracting a broader demographic to facilities.

Q2. What are the main restraining factors for this market?

Growth is hindered by high operational costs, including expensive urban real estate and energy consumption. The market also faces intense competition from digital fitness platforms and home-workout equipment, which offer lower-cost alternatives. Furthermore, a shortage of certified personal trainers and fluctuating consumer spending due to economic inflation can negatively impact membership.

Q3. Which segment is expected to witness high growth?

The boutique fitness studio segment is expected to witness the highest growth. These specialized facilities offer community-focused, high-intensity interval training (HIIT), yoga, or cycling classes. Their appeal lies in providing a premium, personalized experience and a strong sense of community, which traditional big-box gyms often lack, attracting younger, high-spending urban populations.

Q4. Who are the top major players for this market?

The market is led by global giants such as Anytime Fitness, 24 Hour Fitness, and Planet Fitness, which benefit from extensive franchising models. Other significant players include Gold’s Gym, Equinox Holdings, and Basic-Fit in Europe. These companies maintain dominance through aggressive geographic expansion, tiered membership pricing, and strategic brand partnerships.

Q5. Which country is the largest player?

The United States remains the largest player in the offline gyms market. This dominance is due to a mature fitness culture, high disposable income, and a vast network of established health clubs. The presence of major industry headquarters and a strong trend toward specialized boutique fitness further solidifies its market leadership.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model