Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Oral Insulin Therapies Market focuses on the development, production, and commercialization of insulin formulations administered orally, offering an alternative to conventional injections for diabetes management. Oral insulin aims to improve patient compliance, reduce needle-associated discomfort, and enhance quality of life while maintaining effective glycemic control. The market is driven by rising diabetes prevalence, growing awareness of non-invasive therapies, and advancements in drug delivery technologies such as nanoparticles and bioencapsulation.

The Global Oral Insulin Therapies Market is witnessing rapid innovation driven by advancements in drug delivery technologies, including nanoparticles, encapsulation techniques, and enzyme inhibitors that enhance insulin stability and absorption. Rising diabetes prevalence, particularly type 2 diabetes, and increasing patient preference for non-invasive treatments are accelerating adoption. Pharmaceutical companies are focusing on combination therapies and personalized oral insulin formulations to optimize glycemic control.

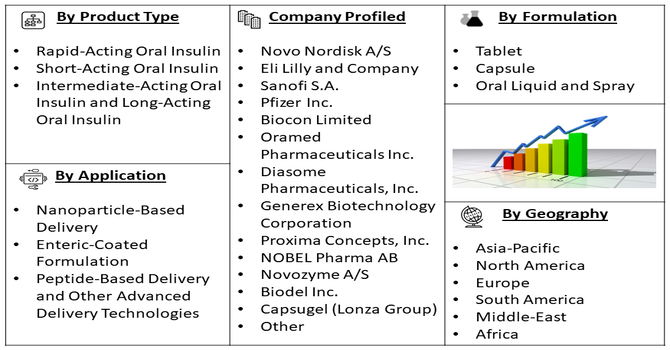

Segmentation: The Global Oral Insulin Therapies Market is segmented by Type (Rapid-Acting Oral Insulin, Short-Acting Oral Insulin, Intermediate-Acting Oral Insulin and Long-Acting Oral Insulin), Formulation (Tablet, Capsule, Oral Liquid and Spray), Technology (Nanoparticle-Based Delivery, Enteric-Coated Formulation, Peptide-Based Delivery and Other Advanced Delivery Technologies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The rising prevalence of diabetes worldwide has significantly fueled the demand for patient-friendly insulin delivery systems. For instance, in 2025, CDC reported that Type 2 Diabetes cases are rising globally, affecting over 460 million adults, with projections reaching 853 million by 2050.

Oral insulin therapies offer a non-invasive alternative to traditional subcutaneous injections, improving adherence and reducing discomfort associated with frequent injections. This convenience encourages patients to maintain regular treatment regimens, thereby supporting better glycemic control. Additionally, oral insulin formulations can potentially mimic physiological insulin absorption through the liver, providing more natural glucose regulation. These factors have driven research, development, and commercialization of oral insulin therapies, expanding their adoption across hospitals, homecare settings, and diabetes care centers globally.

Advancements in drug delivery technologies, such as nanoparticle-based carriers, enteric coatings, and peptide stabilization, have significantly enhanced the bioavailability and efficacy of oral insulin. These innovations address challenges of insulin degradation in the gastrointestinal tract, making oral administration feasible and effective. Increased investment in R&D by pharmaceutical and biotech companies, combined with supportive regulatory frameworks, has accelerated product launches. The integration of smart formulations with patient-friendly dosing regimens has further increased clinician and patient acceptance. Consequently, these technological advancements have strengthened market growth by offering safer, convenient, and efficient alternatives to conventional injectable insulin therapies.

Market Restraints:

Despite significant progress, oral insulin therapies face challenges related to inconsistent absorption and limited bioavailability in patients, which can compromise therapeutic outcomes. The gastrointestinal environment—acidic pH, digestive enzymes, and mucosal barriers—can degrade insulin before it reaches systemic circulation, necessitating higher or repeated doses. Additionally, high research and manufacturing costs and stringent regulatory requirements hinder large-scale commercialization. Patient variability in gastrointestinal physiology further complicates dosing precision. These limitations slow widespread adoption, especially in developing regions, and continue to restrain market growth, as healthcare providers and patients may remain cautious about switching from well-established injectable insulin treatments.

Oral insulin therapies have the potential to significantly improve the quality of life for diabetes patients by eliminating the need for daily injections, reducing needle-related anxiety, and promoting treatment adherence. Improved glycemic control can decrease long-term complications, hospitalizations, and healthcare costs, easing the economic burden on individuals and healthcare systems. Greater accessibility of oral insulin could enhance treatment equity, particularly in underserved regions with limited healthcare infrastructure. Additionally, the growing market supports employment in research, manufacturing, and distribution sectors. Societal acceptance of non-invasive diabetes management may lead to improved productivity, reduced absenteeism, and overall public health benefits.

Segmental Analysis:

The long-acting oral insulin segment was expected to witness the highest growth over the forecast period due to its ability to provide stable, extended glycemic control with fewer daily doses. Patients and clinicians increasingly preferred formulations that reduce the frequency of administration while maintaining consistent plasma insulin levels, improving adherence and quality of life. Advances in sustained-release formulations and protective coatings enhanced bioavailability and absorption. Additionally, growing prevalence of diabetes requiring basal insulin therapy, coupled with ongoing R&D in long-acting oral insulin, drove adoption across hospitals, home care, and outpatient settings globally, supporting robust market growth.

The capsule solutions segment was projected to register significant growth as capsules provide a convenient, patient-friendly, and non-invasive route for insulin administration. Capsule-based oral insulin formulations protect insulin from degradation in the gastrointestinal tract, improving bioavailability and ensuring more predictable therapeutic effects. Patients preferred capsules over traditional injections due to ease of use, pain-free administration, and portability. Technological innovations in enteric coatings, nanocarriers, and mucoadhesive systems further enhanced insulin stability and absorption. The increasing focus on patient-centric diabetes care, combined with rising awareness of oral insulin alternatives, contributed to strong adoption and growth of the capsule solutions segment.

The peptide-based delivery segment was anticipated to witness the highest growth due to its capacity to deliver insulin efficiently through non-invasive oral routes. Peptide engineering and encapsulation technologies improved insulin stability against enzymatic degradation and acidic gastrointestinal conditions, enabling effective absorption. These delivery systems also allowed better mimicry of natural insulin kinetics, supporting controlled glucose regulation. Rising investment in peptide-based oral therapeutics and collaborations between biotech and pharmaceutical companies accelerated clinical trials and market entry. Growing patient demand for innovative, injection-free diabetes therapies further supported adoption, making peptide-based delivery a key driver of growth within the global oral insulin therapies market.

North America was expected to witness the highest growth over the forecast period owing to a high prevalence of diabetes, strong healthcare infrastructure, and early adoption of innovative therapeutics. For instance, the U.S. Department of Health and Human Services (HHS) launched the Healthy People 2030 initiative to lower diabetes prevalence, prevent complications, and reduce related mortality, aiming to lessen the overall diabetes burden and enhance the quality of life for affected individuals.

Additionally, the rising prevalence of diabetes, particularly among Type 2 patients, drives demand for advanced insulin delivery solutions. For instance, in 2025, CDC reported that more than 38 million Americans have diabetes (about 1 in 10), and about 90% to 95% of them have type 2 diabetes. Similarly, in 2025, Diabetes Canada reported that 90% of Canadians with diabetes are living with type 2 diabetes.

The region benefited from significant R&D investment in oral insulin development, supportive regulatory frameworks, and well-established reimbursement policies. For instance, in 2025, Biocon Biologics Ltd. (BBL), expanded its strategic collaboration with Civica, Inc. to include a new Insulin Glargine product. The partnership aimed to increase the supply of high-quality, affordable insulin in the U.S., enhancing accessibility for patients and addressing critical demand for essential diabetes therapies.

Patient awareness and preference for non-invasive insulin therapies, along with collaborations between biotech companies and research institutes, accelerated commercialization. Additionally, North America’s focus on improving patient adherence and quality of life through advanced oral formulations and digital health integration further strengthened market growth, establishing the region as a key hub for oral insulin therapy adoption.

| Report Matrics | Details |

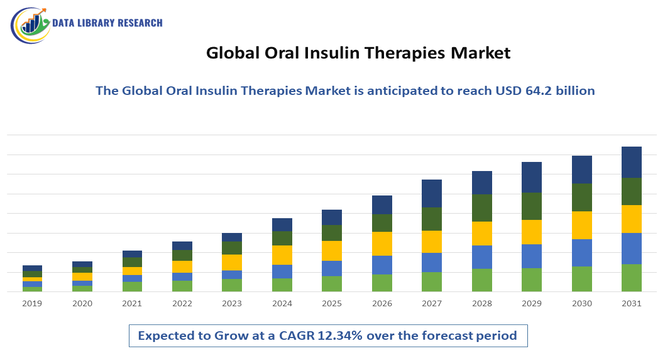

| Market Size Value | USD 64.2 billion |

| Growth Rate | CAGR of 12.34% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global oral insulin therapies market is highly competitive, with a mix of established pharmaceutical companies and emerging biotech innovators. Key players focus on research and development of stable, bioavailable oral formulations and engage in strategic alliances, licensing agreements, and clinical collaborations to accelerate commercialization. Differentiation is achieved through patent-protected delivery technologies, combination therapies, and region-specific regulatory approvals. Market entrants face high R&D costs and clinical trial challenges, while leading companies leverage extensive distribution networks and regulatory expertise.

The major players for the above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the global "needle-phobia" among diabetes patients, which leads to poor treatment compliance. Oral insulin offers a painless alternative to daily injections, significantly improving the patient experience. Additionally, rising rates of Type 2 diabetes and the demand for early insulin intervention to prevent long-term complications fuel research.

Q2. What are the main restraining factors for this market?

Growth is hindered by the biological challenge of protecting insulin from being destroyed by stomach acid and digestive enzymes. Ensuring the body absorbs a consistent, predictable amount of insulin through the gut is technically difficult. High development costs and the long path to winning strict regulatory approval also slow progress.

Q3. Which segment is expected to witness high growth?

The Enteric-Coated Capsules segment is expected to see the highest growth. These specialized coatings are designed to bypass the stomach and only release insulin once they reach the small intestine. This technology is currently the most promising way to ensure the medicine remains effective and safe for daily oral use.

Q4. Who are the top major players for this market?

The market is led by pharmaceutical giants and innovative biotech startups focusing on drug delivery. Key players include Novo Nordisk, Oramed Pharmaceuticals, Biocon, Eli Lilly and Company, and Sanofi. These companies are investing heavily in clinical trials to prove that their oral versions are as effective as traditional shots.

Q5. Which country is the largest player?

The United States is the largest player in the oral insulin therapies market. This is due to its massive diabetes population and the presence of leading biotech research hubs. High healthcare spending and a strong desire for innovative, user-friendly medical treatments make the U.S. the primary driver for oral insulin development.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model