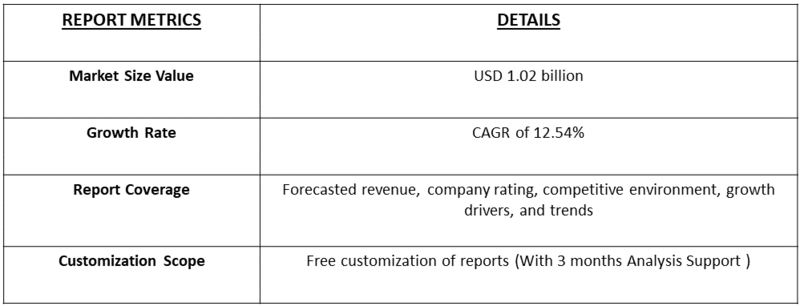

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

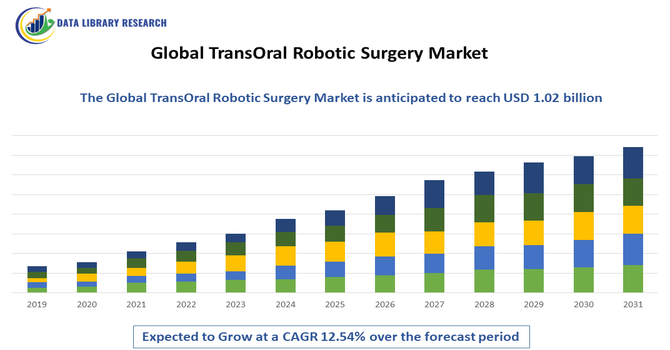

The Global TransOral Robotic Surgery (TORS) Market refers to the industry focused on the development, manufacturing, and adoption of robotic surgical systems designed specifically for minimally invasive procedures performed through the mouth. TORS technology enables surgeons to access hard-to-reach areas in the throat, mouth, and upper respiratory tract with enhanced precision, flexibility, and control compared to traditional surgery. This market is driven by the increasing prevalence of head and neck cancers, advancements in robotic technology, and growing demand for less invasive surgical options that reduce recovery time and complications. As hospitals and surgical centers worldwide adopt these systems for improved patient outcomes, the TORS market continues to expand, supported by innovation, rising healthcare investments, and growing awareness among medical professionals.

The Global TransOral Robotic Surgery (TORS) market is witnessing rapid advancements driven by improvements in robotic precision, imaging, and miniaturization of surgical instruments. Integration of artificial intelligence (AI) and augmented reality (AR) is enhancing surgical planning and real-time navigation, improving outcomes. Additionally, expanding indications beyond head and neck cancers to include benign tumors and sleep apnea treatments are broadening market applications. Increasing adoption of minimally invasive procedures and growing awareness among surgeons about the benefits of TORS, such as reduced recovery times and fewer complications, are further fueling market growth. Furthermore, collaborations between medical device companies and healthcare providers are accelerating the development and accessibility of next-generation robotic surgery platforms.

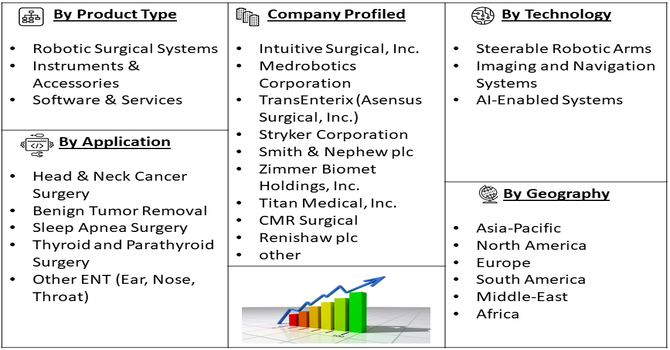

Segmentation: The Global TransOral Robotic Surgery (TORS) market is Segmented by Product Type (Robotic Surgical Systems, Instruments & Accessories and Software & Services), Application (Head & Neck Cancer Surgery, Benign Tumor Removal, Sleep Apnea Surgery, Thyroid and Parathyroid Surgery and Other ENT (Ear, Nose, Throat) Procedures), Technology (Steerable Robotic Arms, Imaging and Navigation Systems and AI-Enabled Systems), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The global rise in the incidence of Human Papillomavirus (HPV)-associated oropharyngeal squamous cell carcinoma (OPSCC) is a primary market driver. TORS is becoming the preferred initial treatment modality for select patients due to its minimally invasive nature and high oncological control rates. For instance, in September 2025, the recent report published by UCI Health, reported that incidence for Oropharyngeal cancer was reported to be more than 21,000 U.S, cases yearly. These cancers, often found in the tonsils and base of the tongue, are easily accessed by robotic platforms, allowing for complete tumor removal while preserving adjacent healthy tissue. This shift in surgical approach, driven by better patient outcomes compared to traditional open surgery or primary chemo-radiation, fuels the demand for new TORS systems, disposable instruments, and specialized surgical training worldwide.

A major advantage of TORS is the significant improvement in patient quality of life post-procedure compared to non-surgical treatment alternatives like high-dose radiation and chemotherapy. TORS minimizes long-term side effects by avoiding external neck incisions and preserving critical structures essential for swallowing and speech. Reduced morbidity translates to shorter hospital stays and quicker returns to normal function and diet. This focus on maximizing functional outcomes is highly valued by patients and is increasingly supported by clinical data, pushing hospitals, particularly in North America and Europe, to invest in robotic platforms to offer TORS as a standard-of-care option for suitable head and neck lesions.

Market Restraints

The substantial cost associated with acquiring and maintaining TransOral Robotic Surgery platforms severely restrains market growth, especially in emerging economies and smaller health systems. The initial capital investment for a robotic system can range from $1.5 million to over $2.5 million. Furthermore, the operational expenses are high, driven by costly disposable instruments specific to each procedure and mandatory service contracts for maintenance. This high cost of ownership necessitates high surgical volumes to achieve a positive return on investment (ROI). Coupled with the limited pool of specialized TORS-trained surgeons, this financial barrier restricts widespread adoption, preventing TORS technology from being implemented in numerous hospitals globally.

The socio-economic impact of the Global TORS market is significant, as the adoption of robotic surgery enhances patient quality of life by offering less invasive treatment options with quicker recovery and reduced hospital stays. This leads to lower overall healthcare costs and decreased loss of productivity due to shorter recovery periods. The market’s growth also contributes to job creation in high-tech manufacturing, software development, and healthcare services, promoting skilled workforce development. However, the high costs associated with robotic systems limit accessibility in low-income regions, potentially widening healthcare disparities. Continued innovation and cost reduction efforts are critical to making these advanced surgical options more affordable and widely available globally.

Segmental Analysis:

The Software & Services segment in the Global TransOral Robotic Surgery (TORS) market is projected to grow significantly due to increasing demand for advanced surgical planning, real-time navigation, and postoperative data analysis. Software enhancements, including AI-driven analytics and augmented reality integration, are improving surgical precision and outcomes. Additionally, ongoing maintenance, training, and support services are becoming essential for hospitals to maximize robotic system efficiency and safety. As healthcare providers adopt robotic surgeries more widely, the need for customized software solutions and comprehensive service packages is rising. This trend is driven by the complexity of robotic platforms, the necessity for continual upgrades, and growing emphasis on data-driven decision-making in surgical care, making software and services a critical growth area in the TORS market.

The Benign Tumor Removal segment within the TransOral Robotic Surgery market is expected to experience significant growth as robotic systems offer minimally invasive, precise options for excising benign tumors in difficult-to-reach areas of the mouth and throat. Unlike traditional open surgeries, robotic procedures reduce patient trauma, minimize blood loss, and shorten recovery times. Increasing awareness among clinicians about these benefits is expanding the use of TORS beyond cancer treatment to address benign tumors such as papillomas and cysts. Advances in robotic instrumentation and enhanced visualization are enabling safer, more effective surgeries, attracting a broader patient base. As healthcare providers seek better patient outcomes and reduced hospital stays, the benign tumor removal segment is set to become a vital contributor to market expansion.

The Steerable Robotic Arms segment is projected to witness substantial growth in the TransOral Robotic Surgery market due to their critical role in enhancing surgical dexterity and precision. These arms provide surgeons with improved flexibility and control when navigating complex anatomical regions within the oral cavity and throat.

Technological advancements have led to smaller, more maneuverable robotic arms capable of performing delicate procedures with minimal invasiveness. For instance, in October 2025, ClearPoint Neuro has developed a proprietary robotic neuro-navigation system. The Solana Beach, California-based company stated that its new product category enabled its navigation software to operate the Kuka LBR robotic arm, supporting various minimally invasive cranial surgical procedures. Growing demand for minimally invasive surgeries, combined with continuous innovation in robotic arm design, is driving adoption in hospitals worldwide, positioning steerable robotic arms as a key growth segment in the TORS market.

North America is expected to experience significant growth in the TransOral Robotic Surgery market, driven by high healthcare expenditure, early adoption of advanced medical technologies, and a strong presence of leading robotics manufacturers. The region’s well-established healthcare infrastructure and increasing prevalence of head and neck cancers support growing demand for minimally invasive surgical solutions like TORS.

Additionally, favorable reimbursement policies and government initiatives promoting robotic-assisted surgeries further boost market growth. The availability of skilled surgeons trained in robotic techniques and rising patient awareness about the benefits of robotic surgery contribute to accelerating adoption. For instanvce, in September 2025, Walter Reed National Military Medical Center, surgeons completed the Department of Defense’s first Transoral Robotic Laryngectomy to remove a non-functioning larynx caused by radiation-induced chondronecrosis. This pioneering procedure highlights the expanding clinical applications of robotic surgery in complex head and neck conditions.This groundbreaking procedure underscored the expanding capabilities of transoral robotic surgery (TORS) in addressing complex and rare conditions, boosting confidence in its clinical applications. It highlights the market’s potential for growth as more advanced and delicate surgeries become feasible using robotic systems, encouraging wider adoption by healthcare institutions in North American region.

Thus, as research and development activities continue to advance in this region, North America is poised to maintain its leadership position in the TORS market over the forecast period.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global TransOral Robotic Surgery market is dominated by a few key players who lead in innovation, technology, and market reach. Companies like Intuitive Surgical, Medrobotics Corporation, and TransEnterix have established strong positions with their advanced robotic platforms and continuous product development. Intuitive Surgical’s da Vinci system remains the market leader due to its extensive clinical adoption and strong brand reputation. Smaller players focus on niche innovations and specialized instruments to differentiate themselves. Strategic partnerships, mergers, and collaborations with hospitals and research institutions are common as companies strive to expand their clinical applications and geographic presence. The market remains highly competitive, with ongoing R&D investments critical for maintaining technological leadership.

The 20 major players for the above market are:

Recent Development

Q1. What the main growth driving factors for this market?

The primary growth drivers are the surging global demand for minimally invasive surgical (MIS) procedures, which offer superior patient outcomes, reduced recovery times, and less post-operative pain compared to traditional methods. Further accelerating growth are continuous technological advancements, including the integration of AI and enhanced 3D visualization in robotic systems, which boost surgeon precision and confidence. Additionally, the increasing global prevalence of chronic diseases, particularly head and neck cancers, creates a larger patient pool requiring complex TORS interventions. Favorable reimbursement policies in developed economies also support wider system adoption.

Q2. What are the main restraining factors for this market ?

The market's expansion is significantly constrained by the substantial initial investment required for procuring robotic systems, such as the da Vinci platform, which can cost millions of dollars. These high costs are compounded by recurring annual maintenance fees and the expense of specialized instruments and accessories. Furthermore, a crucial limiting factor is the lack of a sufficient number of surgeons trained and proficient in TORS techniques, coupled with the steep learning curve required to master these complex robotic platforms, hindering widespread adoption, especially in developing regions.

Q3. Which segment is expected to witness high growth?

The Services segment, which encompasses comprehensive maintenance, technical support, software upgrades, and mandatory specialized training for surgical teams, is projected to witness the highest growth rate. This segment provides continuous revenue streams for manufacturers and is essential for maximizing the longevity and effectiveness of high-cost TORS systems across hospitals. Furthermore, from an application perspective, the broader General Surgery application, which includes many of the procedures suitable for TORS, is also forecasted to experience rapid expansion due to platform versatility.

Q4. Who are the top major players for this market?

The TransOral Robotic Surgery market is dominated by Intuitive Surgical, Inc., which manufactures the highly prevalent da Vinci Surgical System. This system is the benchmark for robotic-assisted surgery and currently holds the largest installed base globally, including for TORS procedures. Other major competitive players rapidly increasing their presence in the broader surgical robotics landscape include Medtronic plc with its modular Hugo RAS system, Johnson & Johnson (developing the Ottava platform), and Stryker Corporation (focusing primarily on orthopedic robotics), all vying for market share.

Q5. Which country is the largest player?

The United States is overwhelmingly the largest and most dominant country in the TransOral Robotic Surgery market, reflecting its leadership in the overall surgical robotics industry. This dominance is driven by a combination of factors: a highly advanced healthcare infrastructure, significant investment in medical technology research and development, and a high rate of adoption of innovative medical devices. Crucially, the presence of established and favorable reimbursement policies for robotic-assisted procedures further solidifies the U.S.'s market supremacy.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model