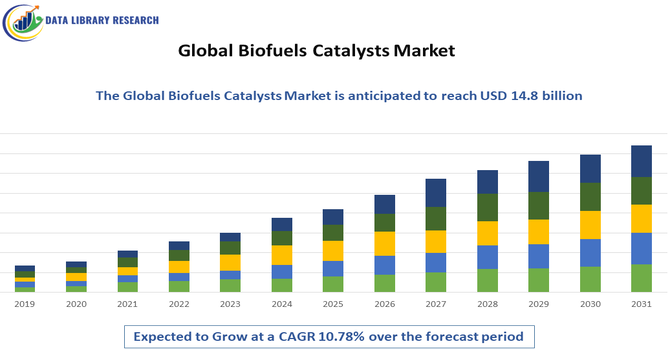

The Global Biofuels Catalysts Market, valued at USD 6.09 billion in 2026, and is projected to reach USD 14.8 billion by 2033, expanding at a CAGR of 10.78% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Biofuels Catalysts Market consists of catalytic materials and systems used to accelerate chemical reactions in the production of biofuels such as biodiesel, bioethanol, and advanced biofuels. Catalysts improve conversion efficiency, selectivity, and production yield while lowering energy consumption and operational costs. They are crucial for transesterification, hydrogenation, and dehydration processes in biofuel manufacturing. The market spans heterogeneous, homogeneous, and enzymatic catalysts applied across refining, oil processing, and renewable energy sectors. Global renewable energy policies, environmental regulations, and expanding biofuel mandates are driving adoption of advanced catalysts to make biofuel production more sustainable and cost effective.

The key trends in the Global Biofuels Catalysts Market include a shift toward advanced and enzymatic catalysts that handle diverse biomass feedstocks with higher efficiency and milder reaction conditions. Nanotechnology and green chemistry principles are increasingly applied to develop catalysts with improved activity, longevity, and environmental performance. Collaborations between catalyst manufacturers and biofuel producers are rising to co develop tailored solutions for complex feedstocks such as algae and agricultural residues. Digital tools like IoT and process simulation are being used to optimize catalyst utilization and lower operational costs. Government biofuel mandates and sustainability initiatives further reinforce technology adoption across global value chains.

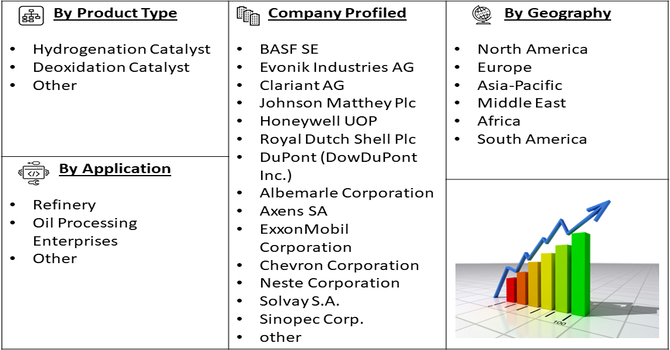

Segmentation: The Global Biofuels Catalysts Market is segmented by Type (Hydrogenation Catalyst, Deoxidation Catalyst, and Other), Application (Refinery, Oil Processing Enterprises, and Other), Feedstock Type (Vegetable Oils (Edible), Non-Edible Oils, Algae, Agricultural Residues and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver of the Global Biofuels Catalysts Market is the global push for renewable energy adoption and stricter environmental standards. Governments worldwide are implementing biofuel blending mandates and incentives to reduce carbon emissions, which directly increases demand for efficient catalysts in biodiesel, bioethanol, and advanced biofuel production. For instance, the Indian Ministry of Petroleum and Natural Gas announced that during July 2025, India achieved an 19.93% ethanol blending rate, with an average of 19.05% for the ongoing ESY 2024–25 as of July 31, 2025.

Renewable fuel policies in major regions such as the U.S. Renewable Fuel Standard (RFS) and the EU’s Renewable Energy Directive compel refiners and producers to integrate biofuels into the energy mix, promoting catalyst demand. This regulatory framework stimulates investment in advanced catalytic technologies that enhance production efficiency and sustainability while enabling compliance with stringent emission norms.

Another key driver is rapid technological innovation in catalyst design and materials. Continuous R&D in heterogeneous and enzymatic catalysts has improved reaction efficiency, feedstock versatility, and catalyst longevity.

Nanocatalysts and bio based catalytic systems offer enhanced surface area and activity, reducing catalyst consumption and production costs. For instance, in 2026, BTG Bioliquids BV and NanosTech signed an MOU to develop integrated solutions for advanced drop-in biofuels. The collaboration accelerated adoption of nanocatalysts and bio-based catalytic systems, enhanced process efficiency, and strengthened innovation and growth across the Global Biofuels Catalysts Market.

Collaborations between catalyst manufacturers, research institutions, and biofuel producers facilitate tailored solutions that meet complex feedstock challenges, including lignocellulosic biomass. Digital manufacturing and process control technologies also enhance catalyst performance and lifecycle management. These innovations support broader application of biofuels across sectors and drive adoption of next generation catalysts that improve biofuel production economics and environmental outcomes.

Market Restraints:

A significant restraint for the Biofuels Catalysts Market is the high cost of catalyst production and raw materials. Advanced catalysts often require expensive metals, specialized chemical compounds, or complex manufacturing processes, which raise upfront production costs and limit widespread adoption, especially in cost sensitive developing regions. Price volatility in precious metals and feedstock chemicals also impacts catalyst producers’ pricing strategies and profit margins. Additionally, supply chain disruptions and geopolitical constraints on critical raw materials can hinder production scalability and increase lead times. These cost pressures may delay biofuel facility expansion and slow catalyst market growth compared to alternative clean energy technologies like electric mobility and green hydrogen.

The Biofuels Catalysts Market contributes to socioeconomic progress by supporting renewable energy infrastructure and reducing dependence on fossil fuels, leading to job creation in R&D, manufacturing, and renewable energy sectors. Catalysts enable efficient biofuel production, which helps lower greenhouse gas emissions and improve air quality, delivering societal health benefits. Expansion of biofuel industries supports rural economies through increased feedstock demand, especially in agriculture and biomass processing. Additionally, government incentives and bioenergy mandates stimulate investments and technological development. However, reliance on specific raw materials and fluctuating feedstock prices impact rural supply chains and investment stability, creating localized economic challenges.

Segmental Analysis:

The Hydrogenation Catalyst segment is expected to witness the highest growth in the Global Biofuels Catalysts Market due to its essential role in converting vegetable oils, fats, and other feedstocks into biodiesel with high efficiency. Hydrogenation catalysts enhance reaction rates, improve selectivity, and reduce by-product formation, resulting in higher-quality biofuels and increased operational efficiency. Rising demand for sustainable fuel alternatives and stricter emissions regulations are driving adoption of hydrogenation catalysts in industrial biodiesel production. Continuous advancements in noble-metal and non-noble-metal catalysts further improve performance and cost-effectiveness. Growing awareness of environmental sustainability and renewable energy mandates ensures strong market expansion for hydrogenation catalysts globally.

The Oil Processing Enterprises segment is projected to witness the highest growth as biofuel production increasingly integrates with large-scale vegetable oil, palm oil, and waste oil processing industries. These enterprises require efficient catalytic systems to convert feedstocks into biodiesel, bioethanol, and other biofuels at scale. Adoption of advanced heterogeneous and hydrogenation catalysts reduces processing time, increases yield, and ensures compliance with quality and environmental standards. Rising government mandates for renewable fuel blending and emission reduction further incentivize large oil processors to invest in high-performance catalysts. The combination of scale, efficiency, and regulatory alignment positions oil processing enterprises as key growth drivers in the biofuels catalysts market.

The Agricultural Residues segment is expected to witness the highest growth due to the increasing use of lignocellulosic biomass, crop residues, and agro-waste as feedstock for second-generation biofuels. Catalysts play a crucial role in breaking down complex cellulose, hemicellulose, and lignin structures into fermentable sugars or biodiesel intermediates. Growing awareness of waste-to-energy solutions and circular economy principles has accelerated investment in technologies that convert agricultural residues into renewable fuels. Catalytic innovations, including enzymatic and nanostructured catalysts, enable efficient conversion with minimal environmental impact. As biofuel production diversifies beyond traditional oils, agricultural residues are emerging as a cost-effective, sustainable feedstock, boosting global catalyst demand.

The Asia-Pacific region is projected to witness the highest growth in the Global Biofuels Catalysts Market due to rising renewable energy initiatives, rapid industrialization, and increasing government support for biofuel production.

Countries such as China, India, Japan, and Southeast Asian nations are expanding biofuel mandates, blending requirements, and investment in advanced catalytic technologies. For instance, in July 2023, Equilon Enterprises LLC and Green Plains Inc. formed a technological collaboration combining Shell Fiber Conversion Technology with Fluid Quip Technologies’ processing systems. The partnership enhanced Green Plains’ biorefinery capabilities, improving efficiency, product yield, and overall biofuel production value.

Abundant availability of feedstocks, including vegetable oils and agricultural residues, further supports market expansion. Additionally, regional catalyst manufacturers are innovating cost-effective solutions to meet local industrial needs while adhering to environmental regulations. Increasing awareness of sustainability and energy security positions Asia-Pacific as the fastest-growing region in the biofuels catalysts sector globally.

| Report Matrics | Details |

| Market Size Value | USD 14.8 billion |

| Growth Rate | CAGR of 10.78% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Biofuels Catalysts Market is moderately consolidated around major chemical and specialty catalyst producers with strong global presence, manufacturing capabilities, and R&D investments. Leaders like BASF SE, Evonik Industries AG, Clariant AG, and Johnson Matthey dominate through broad portfolios and technological leadership in catalyst formulation and process optimization. Other significant firms, such as Honeywell UOP, Royal Dutch Shell, DuPont (Dow), and Albemarle, compete with advanced materials and strategic collaborations with biofuel producers. Mid size and niche technology companies focusing on enzymatic catalysts and eco friendly innovations are gaining traction by offering specialized solutions tailored to evolving environmental regulations and feedstock trends.

The major players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

The primary drivers include the rising consumer demand for "beauty-from-within" products and a holistic approach to wellness. This trend is fuelled by Millennials and Gen-Z, who show a high propensity to pay for science-backed products. Additionally, continuous innovation in ingredients like collagen peptides and the influence of social media in accelerating product discovery are significant growth factors

Q2. What are the main restraining factors for this market?

The most significant challenge is the stringent and fragmented regulatory framework across different regions (e.g., FDA, EFSA), which complicates global product launches and requires costly compliance. Closely related is the need for robust claims substantiation to avoid rising class-action lawsuits and build consumer trust, as skepticism about supplement efficacy can hinder adoption.

Q3. Which segment is expected to witness high growth?

The hydrogenation catalyst segment is projected to experience the highest growth in the global biofuels catalysts market, driven by its critical role in upgrading renewable feedstocks. These catalysts are essential for converting bio-oils and biomass intermediates into high-quality sustainable fuels through hydrotreating and hydroprocessing . Growth is further accelerated by stringent environmental regulations mandating cleaner fuels and the global surge in bio-based chemical production, which requires efficient catalytic hydrogenation for refining fatty acids and other renewable materials.

Q4. Who are the top major players for this market?

The market features a mix of large multinational corporations and specialized brands. Key players consistently identified include Amway Corporation, Herbalife Nutrition Ltd., Nestle Health Science, Shiseido Company Ltd., and Suntory Holdings Ltd.. Other prominent companies are GNC, Kirin Holdings, Unilever (with Nutrafol), and Blackmores.

Q5. Which country is the largest player?

The Asia-Pacific (APAC) region is the largest market, holding nearly half (over 48%) of the global revenue share. This leadership is built on deep-rooted consumer acceptance of functional foods and beauty-from-within concepts, particularly in countries like Japan and South Korea. Within APAC, China is a leading country, holding a significant market share.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model