Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Brachytherapy Market refers to the worldwide industry involved in the development, manufacturing, and commercialization of medical devices, radioactive sources, treatment planning software, and accessories used in brachytherapy—a form of internal radiation therapy used primarily to treat cancer. In this procedure, radioactive materials are placed directly inside or near the tumour, enabling highly targeted radiation delivery with minimal exposure to surrounding healthy tissues. The market includes products such as applicators, afterloaders, seeds, isotopes, and electronic brachytherapy systems used for treating cancers like prostate, cervical, breast, and skin cancers. Growth in the market is driven by increasing cancer incidence and technological advancements in radiation therapy.

The brachytherapy market is witnessing several technological and clinical trends that are reshaping cancer treatment. A key trend is the shift toward high-dose-rate (HDR) brachytherapy, which enables shorter treatment times and improved dose precision compared with traditional low-dose techniques. Integration of artificial intelligence and advanced imaging in treatment planning systems is also improving treatment accuracy and workflow efficiency. Another important trend is the development of electronic brachytherapy, which eliminates the need for radioactive isotopes and simplifies shielding requirements in hospitals. Additionally, the growing adoption of outpatient cancer care and the expansion of brachytherapy applications in breast, prostate, and skin cancers are strengthening market demand globally.

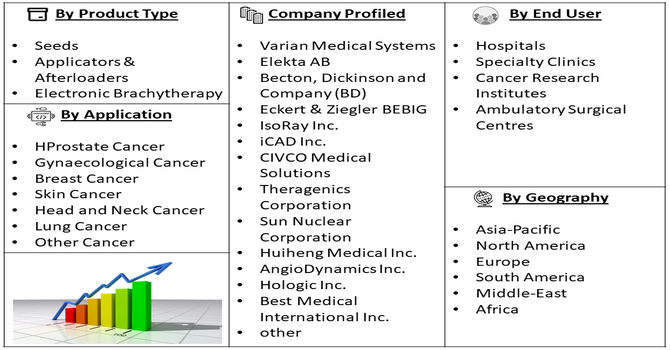

Segmentation: The Global Brachytherapy Market is segmented by Product Type (Brachytherapy Seeds and Applicators and After loaders (Intracavitary applicators, Interstitial applicators, Vaginal applicators, Skin applicators, Remote after loaders and Manual after loaders), and Electronic Brachytherapy Systems), Dosage Type (High-Dose Rate (HDR) Brachytherapy, Low-Dose Rate (LDR) Brachytherapy and Pulse-Dose Rate (PDR) Brachytherapy), Application (Prostate Cancer, Gynaecological Cancer, Breast Cancer, Skin Cancer, Head and Neck Cancer, Lung Cancer and Other Cancer), End User (Hospitals, Specialty Clinics, Cancer Research Institutes and Ambulatory Surgical Centres), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The most significant drivers of the brachytherapy market is the rapid increase in global cancer cases. According to global health organizations, millions of new cancer diagnoses occur each year, with numbers expected to rise significantly in the coming decades. Brachytherapy is widely used to treat cancers such as prostate, cervical, breast, and skin cancer, which are among the most commonly diagnosed cancers worldwide. Because the therapy delivers radiation directly to the tumor site, it offers improved tumor control while reducing damage to surrounding tissues. As healthcare systems focus on early detection and effective treatment options, demand for localized radiotherapy methods like brachytherapy continues to increase globally.

Technological innovation is another key factor driving growth in the brachytherapy market. Advances in imaging technologies, treatment planning software, and radioactive seed implantation techniques have improved treatment accuracy and patient outcomes.

Modern brachytherapy systems integrate imaging modalities such as CT, MRI, and ultrasound to guide precise placement of radiation sources. For instance, in October 2025, the opening of a new brachytherapy suite at the University of Alabama at Birmingham’s Department of Radiation Oncology and O’Neal Cancer Center strengthened the global brachytherapy market by promoting advanced treatment infrastructure. It also accelerated technological progress in radiation therapy, enhancing safety, efficiency, and patient experience, while encouraging wider adoption of specialized brachytherapy techniques.

The development of electronic brachytherapy devices and AI-assisted treatment planning has further enhanced efficiency and reduced procedure complexity. These innovations enable clinicians to deliver higher radiation doses to tumors while minimizing exposure to healthy tissues. As hospitals and cancer centers adopt advanced oncology technologies, the demand for next-generation brachytherapy equipment continues to expand worldwide.

Market Restraints:

A major restraint affecting the growth of the brachytherapy market is the shortage of skilled healthcare professionals trained in advanced radiation therapy procedures. Brachytherapy requires precise placement of radioactive sources and specialized expertise in radiation physics, imaging guidance, and treatment planning. Many hospitals, particularly in developing regions, lack trained radiation oncologists, physicists, and technicians capable of performing complex brachytherapy procedures safely. This shortage limits the adoption of brachytherapy technologies even in regions with high cancer prevalence. In addition, training programs and infrastructure investments are often expensive and time-consuming, which slows the expansion of brachytherapy services and restricts market growth in several emerging healthcare systems.

Brachytherapy plays a significant socioeconomic role in global healthcare by improving access to effective cancer treatment while reducing overall healthcare costs. Compared with conventional external beam radiation therapy, brachytherapy often requires fewer treatment sessions, shorter hospital stays, and lower long-term treatment expenses. These advantages reduce the financial burden on healthcare systems and patients. The technology also contributes to improved survival rates and better quality of life for patients because it minimizes damage to surrounding healthy tissues. In low- and middle-income countries, expanding access to brachytherapy can address gaps in cancer care infrastructure and help manage the growing burden of cancer-related morbidity and mortality worldwide.

Segmental Analysis:

The interstitial applicators segment is expected to witness the highest growth over the forecast period due to its increasing use in delivering precise internal radiation therapy for several cancer types. These applicators enable the direct placement of radioactive sources within tumor tissues, ensuring highly localized radiation while minimizing damage to surrounding healthy cells. Interstitial brachytherapy is widely used in treating prostate, breast, head and neck, and soft tissue cancers. Growing preference for minimally invasive oncology procedures and advancements in image-guided placement techniques are also driving adoption. In addition, improved treatment outcomes, shorter hospital stays, and increasing cancer incidence globally are encouraging healthcare providers to adopt interstitial applicators in brachytherapy procedures.

The Low-Dose Rate (LDR) brachytherapy segment is anticipated to witness significant growth during the forecast period due to its effectiveness in treating localized cancers, particularly prostate cancer. LDR brachytherapy involves the implantation of small radioactive seeds that continuously emit radiation at a low dose over an extended period. This method allows precise radiation delivery directly to the tumor while limiting exposure to surrounding tissues. The procedure is minimally invasive, often performed on an outpatient basis, and offers long-term tumor control with fewer treatment sessions. Increasing awareness of effective prostate cancer therapies, rising patient preference for targeted treatment options, and improvements in radioactive seed technologies are supporting the growth of the LDR brachytherapy segment.

The prostate cancer segment is expected to experience the highest growth in the brachytherapy market during the forecast period due to the rising global incidence of prostate cancer and the increasing adoption of targeted radiation therapies. Brachytherapy is widely recognized as an effective treatment option for localized prostate tumors, offering precise radiation delivery with reduced damage to nearby organs such as the bladder and rectum. The procedure provides high cure rates, fewer side effects, and shorter recovery times compared to some traditional treatment methods. Additionally, advancements in imaging technologies, treatment planning software, and seed implantation techniques are improving clinical outcomes, further encouraging physicians and patients to choose brachytherapy for prostate cancer management.

The hospitals segment is projected to witness the highest growth in the brachytherapy market over the forecast period, primarily due to the availability of advanced medical infrastructure and specialized oncology departments. Hospitals serve as the primary centers for cancer diagnosis and treatment, providing comprehensive care that includes imaging, radiation therapy, surgery, and post-treatment monitoring. The adoption of brachytherapy systems in hospitals is increasing as healthcare providers aim to offer precise and minimally invasive cancer treatments. Additionally, hospitals often have the necessary equipment, trained radiation oncologists, and multidisciplinary teams required to perform complex brachytherapy procedures safely. Growing patient admissions for cancer treatment and rising investments in hospital-based oncology facilities are further driving segment growth.

The North America region is expected to witness the highest growth in the global brachytherapy market during the forecast period due to the strong presence of advanced healthcare infrastructure and high adoption of innovative cancer treatment technologies.

The region experiences a significant burden of cancer cases, which increases the demand for effective and targeted radiation therapies such as brachytherapy. For instance, in September 2025, IDEAYA Biosciences, Inc. reported positive interim results from the Phase 2 OptimUM-09 trial of darovasertib for primary uveal melanoma. The findings reduced radiation exposure during plaque brachytherapy and improved vision outcomes, strengthening North America’s brachytherapy market while advancing precision-guided radiation therapy through integrated targeted therapy and dose-optimization strategies.

Furthermore, the favourable reimbursement policies, ongoing research activities, and continuous technological advancements in radiation therapy systems also support market expansion. Additionally, the presence of leading medical device manufacturers and specialized cancer treatment centres contributes to the rapid adoption of brachytherapy procedures across the United States and Canada, strengthening regional market growth.

| Report Matrics | Details |

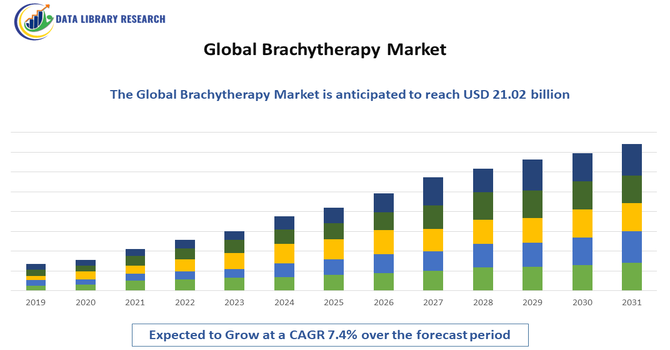

| Market Size Value | USD 21.02 billion |

| Growth Rate | CAGR of 7.4% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months of analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The global brachytherapy market is moderately consolidated, with several multinational medical technology companies dominating product innovation and distribution. Major firms focus on developing advanced afterloaders, applicators, radioactive seeds, and treatment planning software. Companies are pursuing strategies such as mergers, partnerships, and research collaborations to strengthen their portfolios and expand geographic reach. Leading players are also investing in AI-based planning systems and electronic brachytherapy solutions to improve clinical outcomes and workflow efficiency. While North America and Europe remain key markets due to strong oncology infrastructure, companies are increasingly targeting emerging markets in Asia-Pacific and Latin America where cancer incidence and demand for advanced radiotherapy solutions are rapidly increasing.

The major players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

Market growth is primarily driven by the rising global incidence of cancer, particularly prostate, cervical, and breast cancers. The increasing preference for minimally invasive procedures over traditional surgery, coupled with technological advancements like image-guided brachytherapy (IGBT) and AI-driven treatment planning, significantly enhances precision and patient outcomes.

Q2. What are the main restraining factors for this market?

Growth is hindered by high capital investment and operational costs required for specialized radiation equipment and shielding. A global shortage of trained oncologists and medical physicists limits the procedure's accessibility. Additionally, stringent regulatory requirements and competition from alternative treatments, such as robotic surgery and external beam radiation, challenge adoption.

Q3. Which segment is expected to witness high growth?

The Low-Dose Rate (LDR) brachytherapy segment was projected to witness the highest growth over the forecast period due to its effectiveness in delivering continuous, localized radiation with minimal damage to surrounding tissues. Increasing adoption in prostate and gynaecological cancers, improved seed implantation techniques, and rising preference for minimally invasive treatments further supported its expanding clinical utilization.

Q4. Who are the top major players for this market?

The competitive landscape is dominated by leaders in radiation oncology, including Elekta AB, Varian Medical Systems (Siemens Healthineers), and Eckert & Ziegler BEBIG. Other significant players include Becton, Dickinson and Company (BD), Theragenics Corporation, iCAD, Inc., and Isoray, Inc., who focus on innovative radioactive seeds and afterloaders.

Q5. Which country is the largest player?

The United States is the largest market player, accounting majority of global revenue. Its leadership is sustained by a sophisticated oncology infrastructure, high healthcare spending, and favorable reimbursement frameworks. The presence of major industry players and a strong focus on advanced, personalized cancer care further solidify its position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model