Get Complete Analysis Of The Report - Download Updated Free Sample PDF

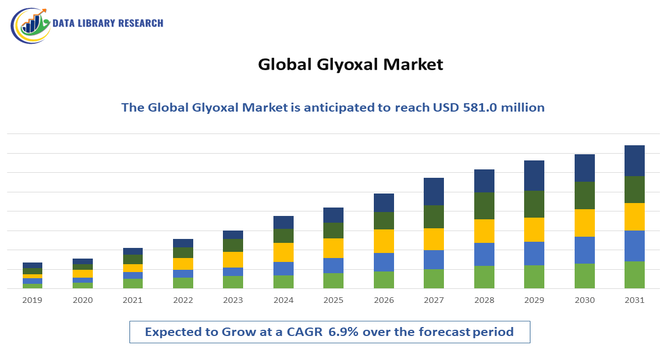

The Global Glyoxal Market refers to the worldwide industry involving the production, distribution, and consumption of glyoxal, a dialdehyde organic chemical primarily supplied as aqueous solutions used as cross-linking agents and intermediates across multiple industrial sectors. It serves essential functions in textile finishing to enhance wrinkle resistance, in paper packaging for improved wet strength and surface properties, and in resins and polymers to boost adhesion and stability. Glyoxal also finds applications in leather processing, cosmetics, and oilfield chemicals. Market growth is driven by expanding industrial use, sustainability trends favoring low-formaldehyde chemicals, and rising infrastructure and manufacturing activity globally.

Key trends in the global glyoxal market include a strong shift toward sustainable and eco-friendly glyoxal formulations as end-use industries emphasize reduced environmental impact. Demand continues to expand in textiles, paper packaging, and resin production segments, with textile finishing remaining the largest application due to growing apparel production worldwide. Technological innovation in high-purity and solid/powder glyoxal grades supports expanded use in pharmaceuticals, coatings, and specialty polymers. Additionally, the Asia Pacific region maintains market leadership in both production and consumption, while North America reflects fast growth owing to advanced manufacturing and regulatory compliance requirements. Increased use in cross-linking agents supports long-term market momentum.

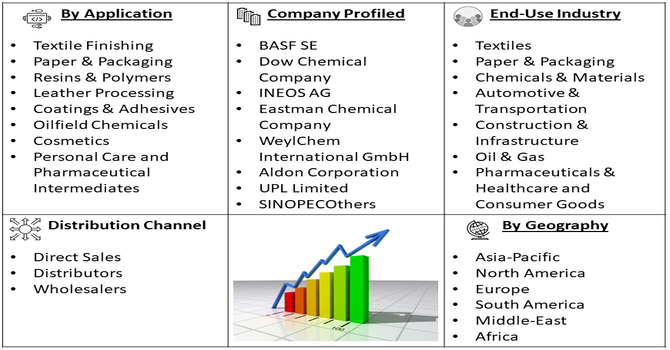

Segmentation: The Global Glyoxal Market is segmented by Product Type (Liquid Glyoxal Solutions and Solid/Powder Glyoxal Forms), Purity Grade (Standard/Industrial Grade Glyoxal and High-Purity/Specialty Grade Glyoxal), Application (Textile Finishing, Paper & Packaging, Resins & Polymers, Leather Processing, Coatings & Adhesives, Oilfield Chemicals, Cosmetics & Personal Care and Pharmaceutical Intermediates), End-Use Industry (Textiles, Paper & Packaging, Chemicals & Materials, Automotive & Transportation, Construction & Infrastructure, Oil & Gas, Pharmaceuticals & Healthcare and Consumer Goods), Formulation (Liquid Grade (Solutions) and Powder/Solid Grade), Distribution Channel (Direct Sales and Distributors & Wholesalers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The glyoxal market is propelled by growing emphasis on green chemistry and low-formaldehyde formulations, as industries adopt environmentally compliant chemical solutions. Regulatory pressures and corporate sustainability goals incentivize use of glyoxal in place of higher-toxicity alternatives, particularly in textiles and consumer products.

Eco-friendly grades and innovations in renewable feedstock production help manufacturers meet environmental standards while appealing to sustainability-minded clients. For instance, in December 2023, INEOS’s acquisition of LyondellBasell’s ethylene oxide and derivatives assets strengthened its raw material supply, supporting sustainable glyoxal production. This enhanced capacity facilitated development of low-formaldehyde formulations, boosting INEOS’s competitiveness in the global glyoxal market.

This shift not only broadens glyoxal’s industrial acceptance but also stimulates research into improved formulations, supporting long-term growth and value creation across sectors seeking both performance and reduced ecological impact.

A key driver of the global glyoxal market is the expansion of industrial applications across textiles, paper packaging, resin production, and leather processing. Glyoxal’s effectiveness as a cross-linking agent enhances wrinkle resistance, moisture stability, and mechanical properties, supporting quality requirements in textile manufacturing and paper strength enhancement. Growth of consumer goods industries, e-commerce-driven packaging demand, and increased use of glyoxal in adhesives and coatings contribute to robust demand globally. Additionally, rising construction, automotive, and electronics sectors boost consumption of glyoxal-derived polymers and specialty chemicals, reinforcing sustained market expansion.

Market Restraints:

A primary restraint faced by the glyoxal market is regulatory and safety concerns related to health and environmental impacts. Glyoxal can pose toxicity and handling challenges, prompting stringent regulations from bodies such as the European Chemicals Agency (ECHA) and U.S. EPA. Compliance with safety, emissions, and discharge standards increases production and operational costs, particularly for small and medium-sized manufacturers. Moreover, volatility in raw material prices—such as ethylene glycol and acetaldehyde—can affect profitability. These factors can restrict investment in capacity expansion and slow market adoption in regions with strict chemical safety regulations, limiting short-term growth potential.

The global glyoxal market influences socioeconomic development by enabling enhanced industrial productivity and value addition across multiple sectors. By improving textile quality, strengthening packaging materials, and contributing to high-performance resins, glyoxal supports industrial diversification and competitiveness, especially in emerging economies. This correlation strengthens export-oriented manufacturing clusters and fosters job creation in chemical production, downstream processing, and industrial services. The rising adoption of lower-toxicity and sustainable glyoxal solutions also aligns with societal demands for safer consumer goods and environmentally responsible chemistry. Additionally, investments in infrastructure, retail, and industrial goods markets result in increased demand for glyoxal derivatives, driving economic activity across the supply chain.

Segmental Analysis:

The liquid glyoxal solutions segment was expected to witness the highest growth over the forecast period due to its wide industrial applicability and ease of handling. Liquid formulations offered superior solubility, uniform dispersion, and compatibility with textile finishing, paper processing, and resin manufacturing systems. Manufacturers preferred aqueous glyoxal solutions because they reduced dust formation and simplified transportation and storage compared to powder forms. Expanding demand from packaging, apparel, and specialty chemical industries further accelerated adoption. Additionally, improvements in stabilized liquid formulations enhanced shelf life and performance efficiency, supporting broader industrial acceptance and driving sustained expansion of this segment globally.

The high-purity and specialty grade glyoxal segment was projected to record the fastest growth owing to rising demand from pharmaceuticals, cosmetics, and advanced material applications. These grades offered controlled impurity levels and consistent chemical performance, making them suitable for sensitive synthesis processes and regulated industries. Increasing quality standards and stricter environmental and safety regulations encouraged manufacturers to shift toward premium-grade glyoxal. Growth in specialty polymers, electronic chemicals, and high-performance coatings also contributed to higher consumption of refined formulations. As innovation intensified across end-use industries, the need for customized, high-purity glyoxal solutions significantly strengthened this segment’s growth trajectory.

The pharmaceutical intermediates segment was anticipated to experience the highest growth as glyoxal gained importance in the synthesis of active pharmaceutical ingredients and specialty compounds. Expanding global drug manufacturing, rising healthcare expenditure, and increasing generic drug production stimulated demand for reliable chemical intermediates. Glyoxal’s role in heterocyclic compound synthesis and antimicrobial formulations enhanced its value in pharmaceutical processing. Additionally, growth in research and development activities, particularly in emerging markets, supported higher consumption of specialty intermediates. Stringent quality requirements further encouraged adoption of refined glyoxal grades, reinforcing sustained expansion within pharmaceutical chemical supply chains.

The pharmaceuticals and healthcare end-use segment was projected to witness robust growth due to increasing demand for advanced chemical intermediates and disinfectant applications. Rising prevalence of chronic diseases, expanding access to medicines, and growth in global pharmaceutical production strengthened glyoxal consumption. Healthcare infrastructure development in emerging economies further accelerated market expansion. Glyoxal’s application in sterilization agents and specialty formulations enhanced its relevance in medical settings. Moreover, heightened focus on quality control and regulatory compliance promoted the use of high-grade chemical inputs. These factors collectively supported significant growth of glyoxal usage within the healthcare and pharmaceutical industries.

The liquid grade (solutions) segment was expected to dominate growth due to operational efficiency, cost-effectiveness, and broad compatibility with industrial processing systems. Liquid glyoxal reduced additional dissolution steps, minimized handling risks, and improved process control in textiles, resins, and paper applications. Industries favored solution-based formats because they streamlined manufacturing workflows and enhanced reaction consistency. Expanding production capacities in Asia and growing demand for eco-friendly cross-linking agents further stimulated adoption. Improved packaging and storage technologies also extended product stability, strengthening global trade flows and reinforcing the liquid grade segment’s leading growth outlook.

The distributors and wholesalers segment was forecast to register the fastest growth as global supply chains became more diversified and regionally interconnected. Small and medium-scale manufacturers increasingly relied on third-party distributors to ensure consistent product availability and localized technical support. Expansion of chemical trading networks across emerging economies enhanced accessibility to glyoxal products in fragmented markets. Distributors also played a key role in regulatory compliance management, warehousing, and customized order fulfillment. As cross-border trade volumes increased and end-use industries expanded geographically, the importance of efficient wholesale channels significantly strengthened overall market penetration and growth.

The Asia-Pacific region was projected to witness the highest growth in the global glyoxal market due to rapid industrialization, expanding textile manufacturing, and strong packaging demand.

Countries such as China and India experienced rising investments in chemical production and downstream industries. For instance, in October 2024, Otto Chemie Pvt. Ltd. expanded its high-purity chemical portfolio and strengthened distribution across India and international markets. This expansion boosted supply reliability and market reach, significantly enhancing growth and demand for glyoxal products in the Asia-Pacific region.

Similarly, in February 2024, Multichem Specialities Private Limited took part in Vitafoods India, enhancing its position in the nutraceuticals and specialty ingredients market and connecting with customers and partners to highlight its growing chemical product range.

Growing consumer markets, infrastructure development, and export-oriented manufacturing supported higher glyoxal consumption across multiple applications. Favorable government policies and cost-competitive production capabilities further attracted capacity expansions in the region. Additionally, increasing pharmaceutical manufacturing and specialty chemical output reinforced regional demand, positioning Asia-Pacific as the fastest-growing contributor to global market revenues.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global glyoxal market is a blend of major international chemical manufacturers and regional specialty producers, with moderate concentration at the top alongside active competition from diversified players. Industry leaders such as BASF SE, Dow Chemical, INEOS AG, and Eastman Chemical Company leverage extensive production networks, broad application portfolios, and robust distribution channels to secure global reach and market share. Regional players in China, India, and Europe focus on cost-competitive glyoxal grades tailored to textile, paper, and chemical intermediate sectors. Competitive strategies include capacity expansion, sustainability investments, product customization, and distribution partnerships to address diverse industrial demand and regulatory frameworks.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The global glyoxal market is primarily driven by rising demand in the textile and paper industries, where it serves as an effective cross-linking agent. Its growing application as a chemical intermediate in pharmaceuticals and agrochemicals also fuels growth. Additionally, the shift toward glyoxal-based resins as formaldehyde-free alternatives stimulates adoption across various manufacturing sectors.

Q2. What are the main restraining factors for this market?

Market growth is restrained by the volatile prices of raw materials, particularly ethylene glycol and acetaldehyde. Environmental and health regulations regarding chemical emissions also pose challenges for manufacturers. Furthermore, the availability of substitute cross-linking agents and the high energy requirements during the production process can limit the overall profit margins for producers.

Q3. Which segment is expected to witness high growth?

The pharmaceutical and agrochemical segments are expected to witness high growth. Glyoxal is increasingly used as a building block for synthesized active ingredients, such as imidazole and pyrazine derivatives. Furthermore, the demand for glyoxal 40% solutions remains dominant due to their widespread utility in leather tanning and textile finishing processes.

Q4. Who are the top major players for this market?

The top major players in the global glyoxal market include BASF SE, Dow Chemical Company, and Huntsman International. Other significant contributors are Silverline Chemicals, WeylChem Group, and Merck KGaA. These companies focus on production capacity expansions and developing high-purity grades to meet the specific requirements of the pharmaceutical and cosmetic industries.

Q5. Which country is the largest player?

China is the largest player in the global glyoxal market, acting as both a leading producer and consumer. This dominance is attributed to the country's massive textile and paper manufacturing hubs. Additionally, significant investments in chemical infrastructure and lower production costs compared to Western regions have solidified China’s position as the market leader.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model