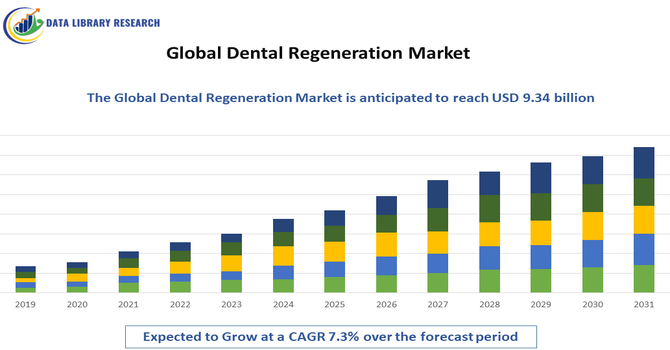

The Global Dental Regeneration Market, valued at approximately USD 6.08 billion in 2026, is projected to reach over USD 9.34 billion by 2033, growing at a CAGR of 7.3% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Dental Regeneration Market refers to the worldwide industry focused on developing, manufacturing, and commercializing products and therapies that biologically repair or regenerate dental tissues such as enamel, dentin, bone, and soft periodontal tissue. It includes biomaterials (bioresorbable scaffolds, membranes), stem cell based products, growth factors, and advanced surgical techniques designed to restore natural dental structure and function. Market growth is driven by the rising prevalence of dental disorders, aging populations, and technological innovation in tissue engineering and biomaterials. The market spans clinical applications in implantology, periodontal regeneration, pulp repair, and guided tissue regeneration across geographic regions.

Key trends shaping the global dental regeneration market include rapid technological advancements in biomaterials and tissue engineering, accelerating adoption of minimally invasive regenerative procedures, and integration of 3D bioprinting for customized scaffolds. Innovative materials such as hydroxyapatite, bioactive glass composites, and stem cell matrices are improving clinical outcomes, boosting success rates in bone and soft tissue regeneration. There is a growing shift toward therapies that restore function rather than merely repair damage, supported by rising demand for aesthetic, long lasting dental solutions. North America currently leads in per patient expenditure on regenerative treatments, while emerging regions like Asia Pacific offer high growth potential due to expanding dental care access.

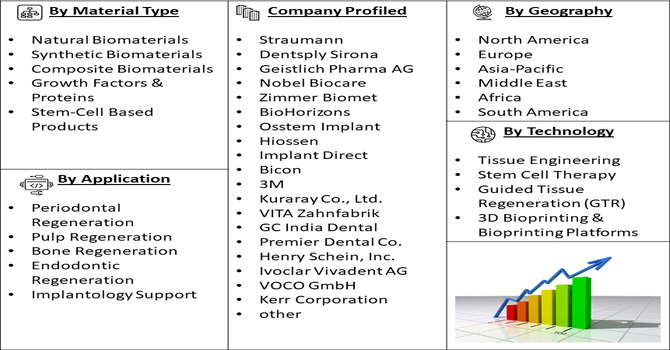

Segmentation: The Global Dental Regeneration Market is segmented by Tissue Segment (Hard Tissue (Enamel, Dentin and Cementum), and Soft Tissue (Gum / Periodontal tissue and Dental Pulp)), Technology (Tissue Engineering, Stem Cell Therapy, Guided Tissue Regeneration (GTR), 3D Bioprinting & Bioprinting Platforms, Nanotechnology-assisted Materials and Others), Material Type (Natural Biomaterials, Synthetic Biomaterials, Composite Biomaterials, Growth Factors & Proteins and Stem-Cell Based Products), Application (Periodontal Regeneration, Pulp Regeneration, Bone Regeneration, Endodontic Regeneration, Implantology Support and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

An aging global population is a primary driver of the dental regeneration market. As life expectancy rises worldwide, the prevalence of age related dental disorders, such as periodontal disease, tooth loss, and alveolar bone degeneration, has increased substantially. For instance, a 2025 published study published by NCBI, reported that in 2021, global estimates indicated 89.6 million cases periodontal diseases cases were reported globally.

These conditions often require regenerative interventions that traditional restorative techniques cannot adequately address. Simultaneously, lifestyle factors and increasing awareness of oral health further fuel demand for advanced regenerative procedures that restore natural tissue rather than replace it. Healthcare systems and providers are responding by integrating biologically oriented therapies into standard practice, driving market expansion and spurring continued investment in innovation across regions.

Technological innovation is another major driver of the dental regeneration market. Advancements in biomaterials science, tissue engineering, and regenerative biology have led to the development of high performance scaffolds, bioactive glass materials, and stem cell based therapies that enhance healing and tissue restoration. For instance, in March 2024, 3Shape and Dentsply Sirona formed a strategic alliance to combine 3Shape’s digital dentistry solutions with Dentsply Sirona’s dental units and software platforms, enhancing workflow integration and improving clinical efficiency through a more connected dental technology ecosystem.

The adoption of 3D bioprinting allows customized scaffolds tailored to individual patient anatomy, improving surgical outcomes. Additionally, growth factor delivery systems and smart biomaterials that mimic native dental tissue properties are driving clinical adoption. These technologies not only improve treatment effectiveness but also attract dental professionals seeking advanced options, thereby expanding the market’s clinical and commercial footprint.

Market Restraints:

A significant restraint on the global dental regeneration market is the high cost of advanced regenerative treatments and limited insurance coverage. Regenerative procedures often involve expensive biomaterials, stem cell processing, and specialized surgical techniques that can cost significantly more than conventional dental therapies. In many countries, insurance providers classify these procedures as elective or cosmetic, resulting in limited reimbursement and high out of pocket expenses for patients. Cost barriers are particularly acute in developing regions where public health systems provide minimal dental coverage. These financial constraints restrict broader market adoption, slowing penetration beyond affluent patient populations and developed markets.

The dental regeneration market significantly influences global healthcare and socioeconomic conditions by enhancing oral health outcomes and reducing long term treatment costs. Improved regenerative therapies decrease reliance on conventional prosthetics and invasive surgeries, leading to faster recovery and higher patient quality of life. Growing awareness of oral health’s link to overall well being has elevated demand for regenerative solutions. Aging populations with higher prevalence of periodontal issues require advanced care, boosting employment opportunities in clinical practice, R&D, and manufacturing. However, high treatment costs and limited insurance reimbursement pose socioeconomic challenges, particularly in lower income regions, potentially exacerbating disparities in access to cutting edge dental care.

Segmental Analysis:

The gum / periodontal tissue segment of the dental regeneration market is expected to witness the highest growth over the forecast period due to the rising global prevalence of periodontal diseases, such as gingivitis and periodontitis, which require advanced regenerative solutions rather than conventional therapies. Increasing patient awareness of oral health, heightened demand for minimally invasive periodontal treatments, and improved access to periodontal care options are driving adoption of soft-tissue regenerative products like collagen membranes and bioactive scaffolds. Growth in this segment is also supported by technological advances that enhance tissue healing and integration outcomes, and by expanding dental services in both developed and emerging regions.

The stem cell therapy segment is projected to experience the fastest growth within the dental regeneration market over the forecast period. This expansion is driven by increasing research and clinical adoption of stem cell-based approaches that enable true biological repair of damaged dental tissues, rather than passive replacement. Mesenchymal stem cells derived from dental pulp, periodontal ligament tissue, and other sources exhibit robust regenerative potential, attracting investment and clinical trials globally. Furthermore, growing R&D efforts and favorable reimbursement trends in key regions are accelerating integration of stem cell protocols into periodontal, pulp, and bone regeneration therapies. The segment’s growth reflects a broader shift toward personalized and biologically oriented dental treatment modalities.

The composite biomaterials segment is expected to witness strong growth over the forecast period as dental professionals increasingly favor materials combining the advantages of natural biocompatibility and engineered performance. Composite biomaterials—often blending polymers with bioactive ceramics or glass—offer enhanced mechanical strength, controlled biodegradation, and improved support for cell attachment and tissue ingrowth. These properties make them particularly attractive for applications in periodontal regeneration, guided tissue frameworks, and implant support. Rising demand for multifunctional regenerative solutions that balance durability with biological integration, along with ongoing innovations in material science, are key factors fuelling this segment’s expansion within the dental regeneration market.

The periodontal regeneration application segment is expected to experience the highest growth over the forecast period, driven by rising incidence of periodontal disease and an aging global population that increasingly requires advanced regenerative dental therapies. Periodontal regeneration focuses on restoring the support structures of teeth, including alveolar bone, periodontal ligament, and gingival tissue, to preserve natural dentition and improve oral function. Breakthroughs in biomaterials, growth factors, and scaffold technologies are enhancing clinical outcomes, encouraging greater adoption. Additionally, increased patient awareness of long-term oral health benefits and greater availability of regenerative treatments in dental clinics worldwide are propelling this segment’s growth.

The North America region is projected to witness the highest growth in the global dental regeneration market over the forecast period.

This leadership is attributed to advanced dental care infrastructure, high per-capita healthcare spending, and widespread adoption of cutting-edge regenerative technologies including biologically active materials and stem cell therapies. For instance, in January 2024, Colossus Dental Technologies introduced its Bio3D Regeneration System, leveraging advanced 3D bioprinting to produce customized dental implants. The launch strengthened North America’s dental regeneration market by accelerating adoption of personalized therapies, enhancing clinical outcomes, stimulating technological competition, and driving investment in next-generation regenerative dentistry solutions.

Similarly, in May 2025, the U.S. Food and Drug Administration approved Biodentical Materials Corporation’s Bio-Oss Collagen for commercial use, advancing collagen-based regenerative solutions. The decision accelerated adoption of biocompatible implant materials, strengthened regulatory confidence, stimulated competitive innovation, and expanded growth opportunities across North America’s dental regeneration market.

The region’s large geriatric population, which has a higher prevalence of periodontal disease and tooth loss, is driving clinical demand. Strong presence of key market players, robust regulatory frameworks, and supportive reimbursement policies further accelerate market expansion. Additionally, investment in dental research and innovation continually introduces new regenerative solutions, reinforcing North America’s dominant position.

| Market Size Value | USD 9.34 billion |

| Growth Rate | CAGR of 7.3% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The global dental regeneration market features a dynamic competitive landscape with multinational medical device and biomaterials firms dominating share through broad product portfolios and strategic collaborations. Key players like Straumann, Dentsply Sirona, and Geistlich Pharma AG lead due to extensive R&D, global distribution networks, and continuous product innovation. Companies are investing heavily in next generation scaffolds, stem cell technologies, and bioactive materials to meet rising clinical demand. Smaller biotechnology firms also compete by specializing in niche regenerative solutions. Market strategies include acquisitions, partnerships with research institutions, and geographic expansion to capture emerging market growth opportunities.

The major players are:

Recent Development

Q1. What is the main growth-driving factors for this market?

Growth is primarily fuelled by the rising prevalence of dental disorders, such as periodontitis and tooth decay, alongside an aging global population prone to tooth loss. Advancements in biotechnology, including stem cell therapy, tissue engineering, and bioactive scaffolds, are also shifting the industry from synthetic implants toward natural biological restoration.

Q2. What are the main restraining factors for this market?

The market faces hurdles such as high treatment costs and limited insurance coverage for advanced regenerative procedures. Strict regulatory requirements for clinical approval of biological materials can delay product launches. Additionally, a shortage of specialized dental professionals trained in regenerative techniques and the high cost of R&D remain significant barriers.

Q3. Who are the top major players for this market?

The market is led by global dental and life sciences giants, including Straumann Group, Dentsply Sirona, and Geistlich Pharma AG. Other key players driving innovation through biomaterials and regenerative products include Zimmer Biomet, Henry Schein, Integra LifeSciences, and Envista Holdings. These companies lead through strategic acquisitions and advanced clinical research.

Q4. Which country is the largest player?

The United States is the largest player in the dental regeneration market, commanding a significant global share. This dominance is supported by its advanced healthcare infrastructure, high per capita dental expenditure, and strong presence of leading biotech firms. A well-established regulatory framework and high adoption rates of new dental technologies further solidify its position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model