Get Complete Analysis Of The Report - Download Updated Free Sample PDF

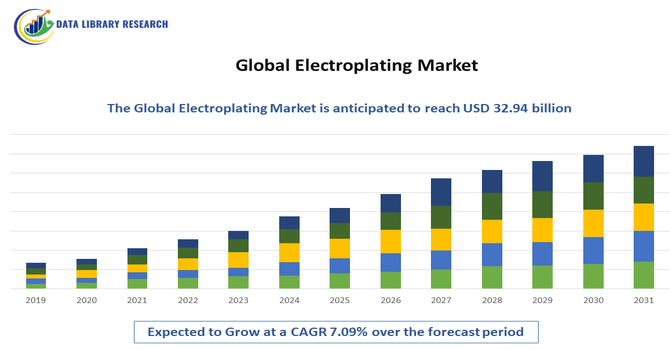

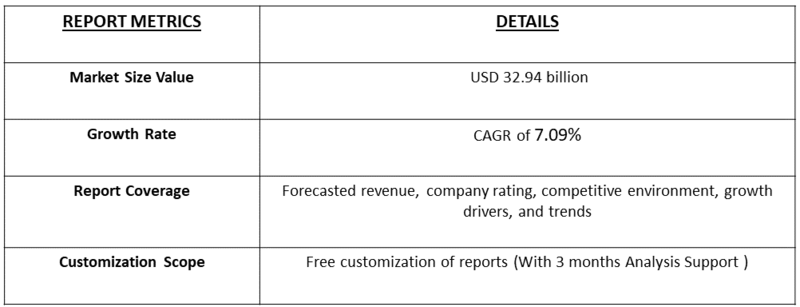

The Global Electroplating Market encompasses the worldwide industry for applying thin metal coatings onto substrates (such as steel, aluminum, and plastics) through an electrochemical process to enhance surface properties like corrosion resistance, wear protection, conductivity, and aesthetics. Electroplating is essential across automotive, electronics, aerospace, industrial machinery, and consumer goods sectors, improving performance and longevity of components. Growing manufacturing activities, rising electronics production, and stringent quality requirements support its adoption. Electroplating technologies include nickel, chrome, copper, and precious metal coatings, with ongoing innovation toward eco friendly processes.

Key trends in the electroplating market include a shift toward sustainable and eco friendly plating processes, such as non cyanide chemistries and trivalent chromium alternatives to reduce hazardous emissions and regulatory risk. Adoption of automation and smart monitoring systems improves precision and efficiency, while digital control and robotics enhance throughput and quality. Demand for high performance coatings for miniaturized electronics, EV components, and advanced industrial parts is increasing. Additionally, waste treatment and closed loop effluent systems are prioritized, driving investment in improved environmental infrastructure. Emerging use of nanocoatings and advanced deposition techniques expands electroplating into new industrial applications.

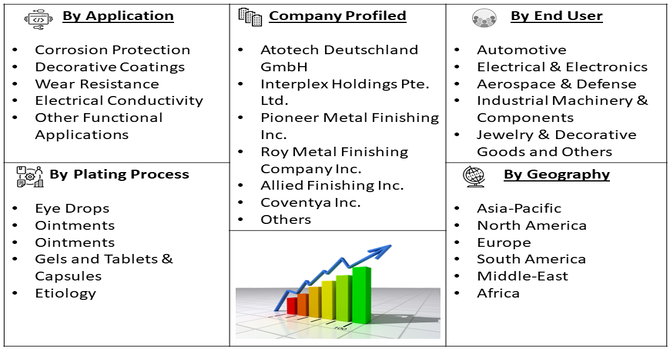

Segmentation: The Global Electroplating Market is segmented by Plating Process (Hard Chrome Plating, Electroless Plating, Zinc Plating, Nickel Plating, Copper Plating, Gold Plating, and Others), Application (Corrosion Protection, Decorative Coatings, Wear Resistance, Electrical Conductivity and Other Functional Applications), Substrate (Base Metals (e.g., steel, aluminum), Plastics & Polymers and Glass & Other Non Metallic Substrates), End Use Industry (Automotive, Electrical & Electronics, Aerospace & Defense, Industrial Machinery & Components, Jewelry & Decorative Goods and Others) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A major driver of the electroplating market is the expanding electronics and electric vehicle (EV) sectors, which require electroplated components to meet performance and reliability standards. In electronics, plating improves electrical conductivity, solderability, and corrosion resistance for connectors, circuit boards, and microcomponents essential in smartphones, 5G infrastructure, and consumer devices, fueling sustained demand. Parallel growth in EV production increases the need for electroplated battery connectors, bus bars, and thermal management parts with superior conductivity and durability. These high growth end use applications amplify the importance of advanced electroplating processes, boosting overall market value and encouraging investment in plating technologies tailored to sophisticated modern components.

Another key driver is the widespread need for electroplated coatings to improve corrosion resistance and extend component life across industrial machinery, automotive parts, infrastructure hardware, and consumer products.

Electroplated zinc, nickel, copper, and other metal layers protect substrates against environmental degradation, wear, and chemical exposure, reducing maintenance costs and downtime for manufacturers and end users. For instance, in February 2025, Oerlikon Surface Solutions reported CHF 1.5 billion (USD 1.69 billion) in 2024 organic sales, driven by PVD growth in aerospace.

As global industry and infrastructure projects expand, demand for durable, high performance coatings grows, making electroplating indispensable to steel fasteners, structural components, and functional assemblies. This enduring requirement supports stable market growth and underpins long term demand across mature and emerging economies.

Market Restraints:

A significant restraint on the electroplating market is the stringent environmental and regulatory framework governing chemical usage, wastewater discharge, and worker safety, which increases compliance costs and operational complexity for manufacturers. Regulations such as REACH in Europe and similar standards globally restrict hazardous plating chemicals like hexavalent chromium, pushing companies to invest heavily in alternative chemistries, effluent treatment systems, and monitoring infrastructure. Smaller plating facilities may struggle with capital requirements for environmental upgrades, limiting expansion.

The electroplating market supports global manufacturing by enhancing product durability, safety, and performance, which in turn stimulates job creation across metal finishing, fabrication, and supply chain services. Electroplated components are foundational to automotive, electronics, aerospace, and infrastructure industries, contributing to industrial competitiveness and export capacity, especially in emerging economies. Improvements in surface finish increase product lifetime, lowering replacement costs for consumers and businesses. However, environmental and safety regulations have socioeconomic implications, driving investments in cleaner technologies and workforce upskilling. The market’s evolution reflects broader industrialization, technological adoption, and rising standards for product quality and sustainability worldwide.

Segmental Analysis:

The Zinc Plating segment is expected to witness the highest growth over the forecast period due to its extensive use for corrosion protection and functional coatings in major industries such as automotive, industrial equipment, and construction. Zinc electroplating provides a cost effective sacrificial barrier that protects steel and iron components from rust and degradation, which is critical for durable end products. The segment’s growth is further supported by rising manufacturing activities in emerging economies and increased demand for rust resistant coatings in heavy duty applications. Additionally, variants like zinc nickel plating are gaining traction for enhanced corrosion resistance, enhancing the appeal of zinc based coatings across global electroplating markets.

The Wear Resistance segment is anticipated to register the highest growth as manufacturers increasingly adopt electroplating solutions that enhance durability and extend the lifespan of components. Electroplating processes such as hard chrome, nickel, and specialized alloy coatings significantly improve surface hardness and resistance to abrasion, friction, and mechanical stress. Industries such as automotive, aerospace, heavy machinery, and tooling heavily rely on wear resistant coatings to maintain equipment performance and reduce maintenance costs. With the demand for longer lasting parts rising alongside automated and high speed manufacturing, wear resistant electroplating solutions are becoming essential for quality assurance. This functional segment’s uptake is driven by performance requirements across industrial sectors and shifting emphasis toward efficiency and product reliability.

The Plastics & Polymers segment is forecasted to witness significant growth as industries increasingly incorporate electroplating on plastic components to enhance aesthetic appeal, conductivity, and surface functionality. Electroplating on plastics enables lightweight, cost effective, and corrosion resistant parts that meet performance and design requirements in automotive, electronics, consumer goods, and appliances. Rapid adoption of lightweight materials to reduce weight in vehicles and portable electronics further boosts demand for plating on polymer substrates. Technological advancements improving adhesion and finish quality on plastics are enabling broader application, making this segment a key driver of overall electroplating market expansion. Growth is strongest in regions focused on electronics and automotive production, reflecting rising plastics plating adoption worldwide.

The Electrical & Electronics end use segment is projected to witness the highest growth over the forecast period as global demand for high performance and durable electronic devices surges. Electroplating plays a vital role in producing connectors, circuit board components, and micro parts with enhanced conductivity, corrosion resistance, and solderability, which are crucial for smartphones, computers, and telecommunications hardware. Increasing consumer electronics production, expansion of 5G infrastructure, and advancements in semiconductor packaging further underscore the need for precise, reliable electroplated finishes. The sector’s rapid innovation cycle and adoption of miniaturized components ensure continuous uptake of advanced electroplating technologies. As electronics manufacturers prioritize performance and quality, this segment’s growth broadly supports the global electroplating market.

The Asia Pacific region is expected to witness the highest growth in the global electroplating market owing to its large manufacturing base, rapid industrialization, and expanding automotive, electronics, and industrial sectors.

Countries such as China, India, Japan, and South Korea drive demand due to cost effective production capacities, strong OEM presence, and significant export volumes of electroplated components. For instance, in March 2023, DuPont Electronics & Industrial unveiled ULTRAFILL 6001 dual damascene copper, enhancing BEOL electroplating for nanoscale copper interconnects. This innovation boosted Asia-Pacific’s electroplating market by increasing demand for advanced semiconductor plating solutions, supporting high-precision electronics manufacturing and driving regional adoption of cutting-edge plating technologies.

Investment in infrastructure development, electric vehicles, and consumer electronics further fuels regional growth. For instance, in April 2025, ACM research expanded its horizontal ECP tool suite, securing about 30% domestic market share in China. Similarly, in May 2025, DYCONEX invested CHF 7 million to upgrade copper and gold lines for 7-µm subtractive-process boards, enhancing production capabilities.

Supportive government initiatives and a skilled workforce also enhance competitive advantage, making Asia Pacific a dominant and fast growing market. With robust demand from high volume plating applications and continued industrial expansion, the region is projected to maintain leadership in electroplating market growth throughout the forecast period.

To Learn More About This Report - Request a Free Sample Copy

The global electroplating market is moderately consolidated, with major multinational surface finishing and chemical suppliers holding significant share alongside numerous regional job shops and service providers. Industry leaders compete by integrating advanced chemistry portfolios, automated equipment, and digital process control to differentiate beyond price based offerings. Strategic acquisitions, such as mergers enhancing key capabilities, are part of competitive dynamics. Many companies emphasize sustainable chemistries, process innovation, and compliance with environmental regulations, which are increasingly essential for winning contracts in automotive, aerospace, and electronics sectors. Smaller, specialized firms maintain strong positions in local markets by offering customized plating solutions and responsive service.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is surging demand from the automotive and electronics industries. Electroplating provides essential corrosion resistance, aesthetic appeal, and electrical conductivity for modern components. The rapid shift toward electric vehicles requires specialized plating for battery connectors and charging infrastructure, while the miniaturization of electronic devices further fuels consistent market expansion.

Q2. What are the main restraining factors for this market?

Strict environmental regulations regarding the disposal of hazardous chemical waste and toxic heavy metals act as a major restraint. High energy consumption and volatile raw material prices for precious metals like gold and palladium also squeeze profit margins. Additionally, the emergence of alternative coating technologies, such as physical vapor deposition.

Q3. Which segment is expected to witness high growth?

The Electrical & Electronics segment is expected to witness the highest growth due to increasing demand for durable, high-performance components. Electroplating enhances conductivity, corrosion resistance, and solderability in connectors and circuit boards, driven by expanding consumer electronics, 5G infrastructure, and semiconductor advancements, boosting market growth significantly.

Q4. Who are the top major players for this market?

Key global participants include Atotech (now part of MKS Instruments), Umicore, DuPont, MacDermid Enthone Industrial Solutions, and Tanaka Holdings. These companies lead through advanced chemical formulations and sustainable plating processes. They focus heavily on research and development to create eco-friendly electrolytes that comply with increasingly stringent international environmental safety standards.

Q5. Which country is the largest player?

China is the largest player in the global electroplating market. Its dominance is supported by a massive manufacturing infrastructure, particularly in the automotive and consumer electronics sectors. Low labor costs, favorable government industrial policies, and the presence of numerous small-to-medium enterprises make it the world’s central hub for plating services.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model