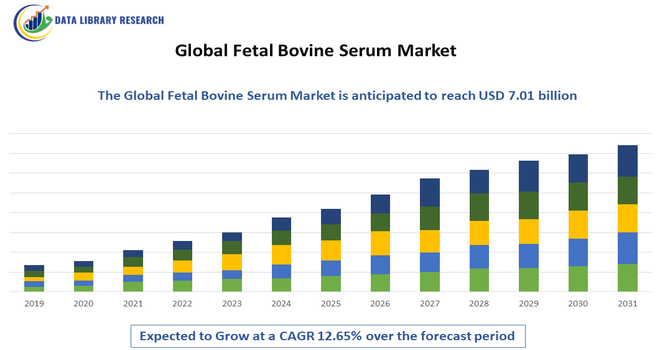

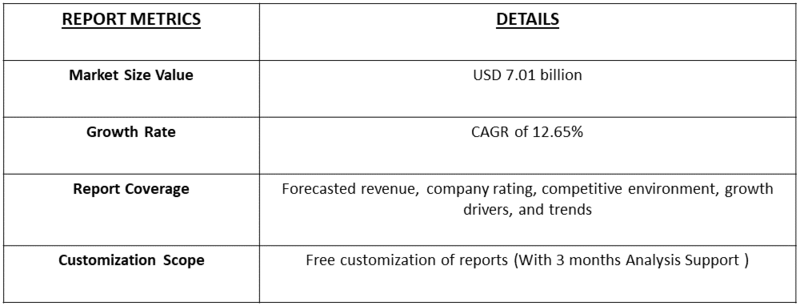

The Global Fetal Bovine Serum Market size was estimated at USD 2.98 billion in 2026 and is projected to reach USD 7.01 billion by 2033, growing at a CAGR of 12.65% from 2026 to 2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Fetal Bovine Serum Market refers to the worldwide industry involved in the production, distribution, and sale of fetal bovine serum — a nutrient-rich component derived from bovine fetuses used as a supplement in mammalian cell culture media. FBS is essential for cell proliferation in research, biopharmaceutical production, vaccine manufacturing, and regenerative medicine due to its growth factors and proteins that support in vitro cell growth. The market spans academic research labs, pharmaceutical and biotechnology companies, contract research organizations (CROs), and diagnostics firms. Growth is driven by biotechnology expansion and the rising demand for biologics, despite ethical and regulatory constraints around animal derived products.

Current market trends emphasize quality certified, traceable, and ethically sourced FBS products, reflecting increased regulatory and ethical scrutiny. Researchers and manufacturers are prioritizing high purity and specialized variants such as stem cell qualified and exosome depleted FBS to meet specific application needs in advanced therapies, vaccine research, and bioproduction. Geographic expansion in Asia Pacific, particularly China and India, is driving new demand, while ongoing innovations in serum alternatives, like chemically defined media and serum free supplements, are influencing product portfolios. Partnerships, vertical integration, and enhanced quality control practices are also shaping competitive dynamics as market players adapt to evolving scientific expectations.

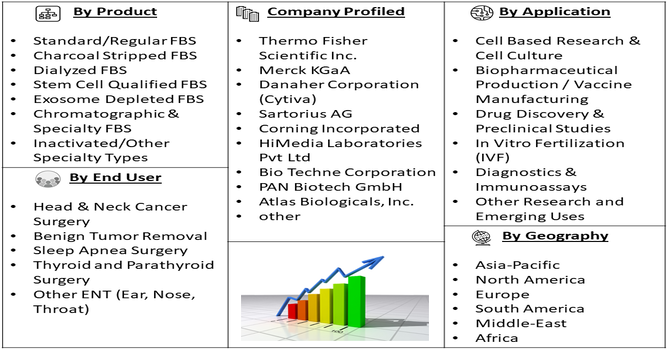

Segmentation: The Global Fetal Bovine Serum Market is segmented by Product (Standard/Regular FBS, Charcoal Stripped FBS, Dialyzed FBS, Stem Cell Qualified FBS, Exosome Depleted FBS, Chromatographic & Specialty FBS and Inactivated/Other Specialty Types), Application (Cell Based Research & Cell Culture, Biopharmaceutical Production / Vaccine Manufacturing, Drug Discovery & Preclinical Studies, In Vitro Fertilization (IVF), Diagnostics & Immunoassays and Other Research and Emerging Uses), Form (Liquid FBS and Powdered / Lyophilized FBS), End User (Pharma & Biotechnology Companies, Contract Research Organizations (CROs) / CMOs, Academic & Research Institutes, Hospitals & Clinical Research Centers, Diagnostic Laboratories and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver of the global FBS market is the rapid expansion of biopharmaceutical research and development. Increasing investment in drug discovery, monoclonal antibodies, vaccine development, cell and gene therapies, and advanced biologics requires robust cell culture systems, with FBS being a critical supplement to support cell proliferation and viability.

The market benefits from rising funding for biomedical research globally, growing applications in regenerative medicine, and intensified efforts to develop treatments for chronic diseases. For instance, In February 2022, South Korea’s CellMEAT raised USD 4.5 million to scale cultivated meat production. By December, it introduced FBS-free cell culture media, advancing biopharmaceutical R&D and reducing reliance on FBS. This innovation impacted the global FBS market by promoting serum alternatives, supporting both domestic and international cultured product development. This upward R&D trajectory fuels demand for high-performance, quality-certified FBS products across academic institutions, biotech firms, and pharmaceutical manufacturers seeking reliable culture media components.

Cell culture remains foundational to in vitro experiments, toxicology tests, cancer research, stem cell studies, and diagnostic kit production. The proliferation of CROs and CMOs supporting outsourced research amplifies FBS consumption, as does the need for standardized media components with reproducible performance. For instance, in September 2022, scientists developed an in vitro meat growth technique using FBS with magnetic fields, advancing cell-based research and diagnostics and increasing global FBS demand for regenerative medicine and experimental applications.

In vitro fertilization (IVF) applications and the rising prevalence of chronic conditions also boost demand. As laboratories expand globally, especially in emerging biotech hubs, consistent supply of FBS becomes essential to sustain scientific workflows and meet rigorous regulatory standards required for pharmaceutical and clinical research endeavors.

Market Restraints:

A significant restraint on the FBS market stems from ethical and regulatory concerns associated with animal-derived products. Because fetal bovine serum is harvested from bovine fetuses during slaughter, animal welfare advocates and regulatory authorities are increasingly scrutinizing sourcing practices, leading to heightened compliance requirements, traceability standards, and societal pressure for alternatives. These concerns have encouraged some research institutions and companies to reduce FBS usage or explore synthetic and serum free media. Regulatory variability across regions also complicates supply chains and raises costs for certification and quality control, posing barriers to market expansion and supporting the shift toward more defined, animal-component-free culture solutions.

The FBS market significantly supports the global biomedical ecosystem by enabling research and development in therapeutics, vaccines, and regenerative medicine. Growing investment in life sciences and biotech sectors leads to job creation, technological innovation, and enhanced healthcare outcomes. Demand for FBS correlates with expanded academic and industrial research, contributing to economic activity across supply chains, from livestock producers to cell culture suppliers. However, ethical concerns about animal welfare influence social discourse and regulatory frameworks, prompting debates on sustainability and alternatives. The market’s growth in emerging economies also reflects increasing scientific capacity and improved access to advanced cell culture tools, ultimately aiding global scientific competitiveness.

Segmental Analysis:

The Stem Cell Qualified FBS segment is expected to witness the highest growth among product types over the forecast period due to the expanding demand for specialized, high quality serum in regenerative medicine and advanced cell therapy research. Stem cell applications require highly consistent and traceable serum with minimal variability to support sensitive cell lines and meet stringent regulatory requirements, which drives preference for stem cell qualified grades. As clinical pipelines for autologous and allogeneic therapies mature, researchers increasingly adopt these premium products to ensure reproducibility and safety in culture systems. This specialized segment’s growth outpaces standard products, reflecting its critical role in cutting edge biomedical research and therapeutic development.

The Drug Discovery & Preclinical Studies application segment is projected to register the highest growth in the FBS market over the forecast period as pharmaceutical and biotechnology companies intensify efforts to develop novel therapeutics. FBS remains essential in supporting complex cell based assays, screening models, and preclinical evaluation systems, providing necessary growth factors and nutrients for mammalian cell viability. Rising investment in oncology, immunology, neurodegenerative, and personalized therapies further stimulates demand for high quality serum to ensure robust, reproducible results early in the drug development pipeline. As global R&D expenditure increases and drug pipelines expand, FBS use in drug discovery and preclinical research is expected to accelerate more rapidly than in other segments.

The Liquid FBS form segment is expected to witness the highest growth over the forecast period due to its widespread usability and convenience in laboratory operations. Liquid serum, ready to use without reconstitution, supports streamlined workflows, reduces preparation time, and minimizes variability risk—features highly valued by research institutions and industrial laboratories engaged in continuous cell culture activities. As demand increases for dependable culture media across biopharmaceutical production, vaccine development, and academic research, liquid FBS remains the preferred format for many applications. Its growth is further fostered by broader distribution channels and improved cold chain logistics, ensuring reliable supply and quality for end users globally.

The Academic & Research Institutes end user segment is anticipated to record the highest growth rate in the fetal bovine serum market over the forecast period. Expansion in university research programs, government funded biomedical initiatives, and collaborations between academic laboratories and industry sponsors has substantially increased demand for FBS in foundational cell biology, molecular research, and translational studies. These institutes often require diverse serum grades to support a wide range of experimental protocols, fueling increased procurement. Grow¬ing global emphasis on life sciences education and expanding research infrastructure in emerging economies are also key growth drivers, propelling academic demand more rapidly than traditional commercial research sectors.

The North American region is expected to witness the highest growth in the global FBS market over the forecast period, driven by its well established biotechnology, pharmaceutical, and academic research infrastructure.

The United States and Canada host a concentration of leading life sciences companies, advanced research institutions, and robust funding mechanisms that collectively stimulate high levels of cell culture research, biologics development, and preclinical testing requiring FBS. For instance, in November 2024, Lonza completed its first GMP batch at its next-generation mammalian manufacturing facility in Portsmouth, USA. This milestone boosted North America’s FBS market by increasing demand for high-quality cell culture media to support advanced biologics and cell and gene therapy production, strengthening the region’s biopharmaceutical manufacturing ecosystem.

Presence of stringent quality standards and early adoption of specialized serum products further bolster regional demand. While Asia Pacific may grow rapidly in percentage terms, North America will remain the largest regional market due to its mature ecosystem and high per capita investment in life sciences innovation.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global FBS market is moderately fragmented with major multinational life sciences and biotechnology companies dominating share. Leading players focus on product quality, regulatory compliance, expanded distribution networks, and R&D to meet diverse customer requirements. Strategic activities such as acquisitions, partnerships, and geographic expansion strengthen competitive positioning, while smaller, specialized suppliers differentiate through niche formulations and agile service. Competition centers on innovation in serum variants, traceability, ethical sourcing, and support services. Regional competitors in Asia Pacific and Europe also contribute to market diversity. Large incumbents often leverage integrated supply chains and brand reputation to maintain leadership against emerging rivals.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the expansion of biopharmaceutical research and vaccine production. Fetal Bovine Serum is a critical growth supplement for cell cultures used in drug discovery and biotechnology. Additionally, rising investments in life sciences, increasing prevalence of chronic diseases, and the burgeoning field of regenerative medicine significantly boost global demand.

Q2. What are the main restraining factors for this market?

The market faces constraints from ethical concerns and the high cost of serum collection. Stringent regulatory hurdles regarding animal welfare and contamination risks also limit supply. Furthermore, the industry is seeing a shift toward serum-free media and chemically defined alternatives, which offer better reproducibility and reduce dependency on animal-derived products.

Q3. Which segment is expected to witness high growth?

The Drug Discovery & Preclinical Studies segment is projected to witness the highest growth, driven by increasing global investment in pharmaceutical R&D. FBS supports critical cell-based assays, screening models, and preclinical evaluations. Rising demand for oncology, immunology, and personalized medicine accelerates serum usage in early-stage drug development, ensuring reproducible and reliable results.

Q4. Who are the top major players for this market?

Leading players include Thermo Fisher Scientific Inc., Merck KGaA (Sigma-Aldrich), GE Healthcare (Cytiva), and Danaher Corporation. Other significant contributors are Bovogen Biologicals, Atlas Biologicals, and HiMedia Laboratories. These companies maintain dominance through sophisticated supply chains, rigorous quality-control testing, and strategic geographic sourcing to ensure a consistent serum supply for laboratories.

Q5. Which country is the largest player?

The United States is the largest player in the FBS market. Its dominance is driven by a massive biopharmaceutical sector, world-class research universities, and extensive government funding for healthcare R&D. Furthermore, the U.S. maintains strict standards for serum collection, making North American-sourced FBS highly desirable due to its lower risk profile.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model